I couldn’t find a dedicated thread for so-called “quality companies,” so I decided to open a brand new one for it. The purpose of the thread is to spark a diverse discussion about quality companies that meet strict criteria. Hopefully, the thread will also help other community members find interesting new investment targets! I hope that if you know of a firm that meets the criteria, you’ll submit it here!

What then is a quality company that this thread is meant to discuss? There are many definitions of a quality company, and no single truth exists. Therefore, as the founder of the thread, I take the liberty of defining a quality company for this thread. This is partly because I don’t want the thread to be flooded with hundreds of firms that another person might think are far from quality firms. I want the best firms from the global stock markets here, because unfortunately, they are hard to find on the Helsinki Stock Exchange! From this, you can already deduce that the criteria are strict. The criteria consist of both quantitative and qualitative factors. When you submit a firm to the thread, you must put in the effort to explain how the company meets the required criteria.

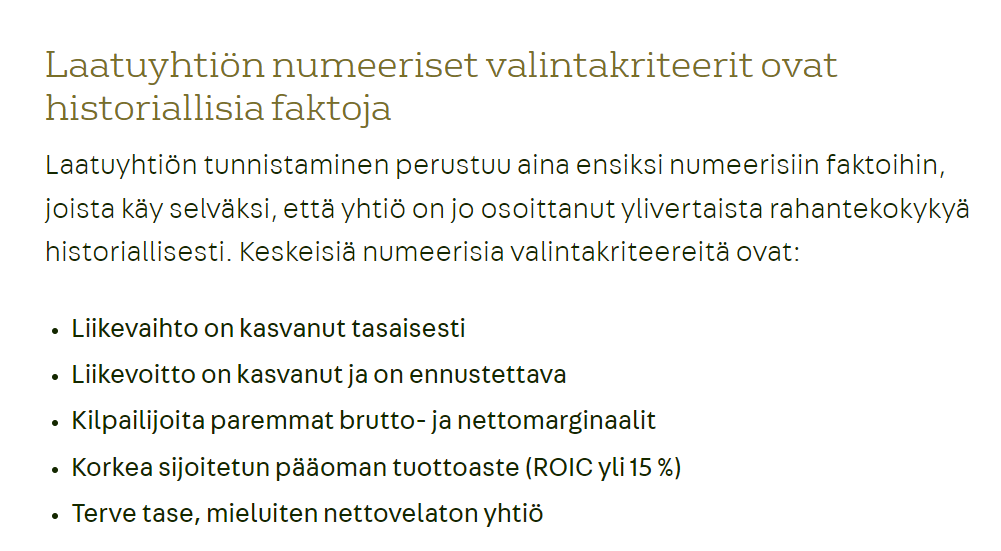

Quantitative criteria:

- ROIC > 15%

- Revenue growth > 5% p.a.

- Earnings growth > 7% p.a.

- Net profit margin > 12%

These figures should roughly have been realized over the last 5 years, but exceptions are allowed if the deviation can be credibly justified as somehow “one-off” or similar. Cash flow-based metrics (e.g., FCF must not be below 80% of net income) or capex/R&D share relative to revenue could have been added to the quantitative criteria, but I did not include them now.

Qualitative criteria:

- Credible arguments that the previous earnings growth trend and high return on invested capital will continue for at least years (5-10 years?) to come. Very likely growth must therefore be profitable (high ROIC). This leads to the point…

- Deep moats. Only genuinely deep moats in a high-quality business enable the requirement above. Why does this specific firm have deep moats, and why are competitors (likely) unable to step on its toes?

- The business must not be too cyclical. The stock price can fluctuate, but the earnings should be somewhat predictable. Of course, few firms/industries are completely immune to global events, so we aren’t completely blind here. For example, in a single year, earnings/revenue may hit a hiccup, but there must be a clear external reason for it, and it must recover quickly.

EXAMPLES:

On the Helsinki Stock Exchange, for example, Elisa is perceived as a quality firm, and by many metrics and arguments, it is. However, Elisa does not meet the criteria of this thread; revenue growth hasn’t really reached the target, and there isn’t much room to improve profitability. Furthermore, in my view, there aren’t really credible arguments for how the firm could tap into sufficiently high earnings growth. KONE also drops out of this thread because the growth in revenue and earnings is very stagnant. KONE’s net margins are also unnecessarily low.

Another typical quality firm on the Helsinki Stock Exchange is Revenio, which meets the above criteria, at least in a historical light. On the other hand, the growth streak will break this year, so it could well be asked whether Revenio still belongs in this category. In my opinion, it does, if we can credibly justify with the firm’s qualitative factors why this year is an exception and we will return to “normal” quickly. So, a single year doesn’t yet ruin the quality company label; the big picture counts. I will return to Revenio later because I think it meets the criteria, but high-quality arguments are required for this!

I will also return later with a couple of other messages to this thread, including the companies Novo Nordisk and West Pharmaceutical Services, both of which deserve their own posts.

Note! No one will be put down in this thread, even if you submit a company that doesn’t strictly meet the criteria. The purpose is purely to find new high-quality firms to explore. The criteria are strict so that only the highest quality ones are submitted and the workload doesn’t become too large, as there are plenty of firms in the stock markets. For example, a firm that doesn’t have a long enough track record yet, but there are very good reasons to believe it’s precisely the top firm of the future, is very interesting and welcome in this thread ![]() Rather, we’ll be flexible on the numbers if the qualitative side is top-tier. In some way, however, the numbers must already support the narrative, so unfortunately Hyzon drops out

Rather, we’ll be flexible on the numbers if the qualitative side is top-tier. In some way, however, the numbers must already support the narrative, so unfortunately Hyzon drops out ![]()

Once a firm has been suggested, in the spirit of the thread, it is very good to have a constructive discussion about it. So, the thread is not intended to be filled only with “announcement posts,” but quality discussion about these firms is also very welcome.

ADDITION 5.11.2023:

The importance of the growth component was already challenged a bit in the thread. A link that appeared in the thread (Importance of ROIC: “Reinvestment” vs “Legacy” Moats | Saber Capital Management) handled well why this is precisely important from an investor’s point of view. A high ROIC is not automatically a guarantee of happiness for an investor if the firm cannot reinvest the business cash flow again and again at this high ROIC back into growing the business. Highly recommended reading.