Gentoo’s Q4/24 earnings report yesterday. The train is chugging along:

Good:

- Healthy overall picture: 16th consecutive time revenue is at ATH and 18% organic YoY growth. Full-year organic growth 17%.

- They expect double-digit organic growth this year as well. More detailed guidance will come in the Q1 report.

- No major headwinds from Google updates, nor are problems expected in the near future.

- Overall good performance in 2024 vs. competitors.

- The Chairman of the Board mentioned buybacks as one option for cash flow allocation.

Bad:

- EBITDA dropped to 40% (full year 46%), and consequently, cash flow also suffered; clearly, “extra” marketing was invested at the expense of profitability to reach the lower end of the revenue guidance. According to the CEO, they will stick to the familiar 45-50% EBITDA going forward, which naturally also weakens revenue growth compared to this quarter.

- Rev share (most valuable revenue) accounted for only 51% of revenue, presumably for the same reason as above. According to the CEO, this will also return to the normal level of approx. 60% in the future.

- Top5 websites flat YoY, growth came from smaller sites. Casinotopsonline, in particular, is still having problems. In the report, they tried to spin this as growth coming from a broad front and not being entirely dependent on the largest sites. But this doesn’t inspire confidence, and it’s a bit hard to believe in strong sustainable growth when some of the spearhead products are struggling. On the other hand, there’s hidden upside here if and when they get, for example, casinotops up and running, which seems to be a priority project for the CEO.

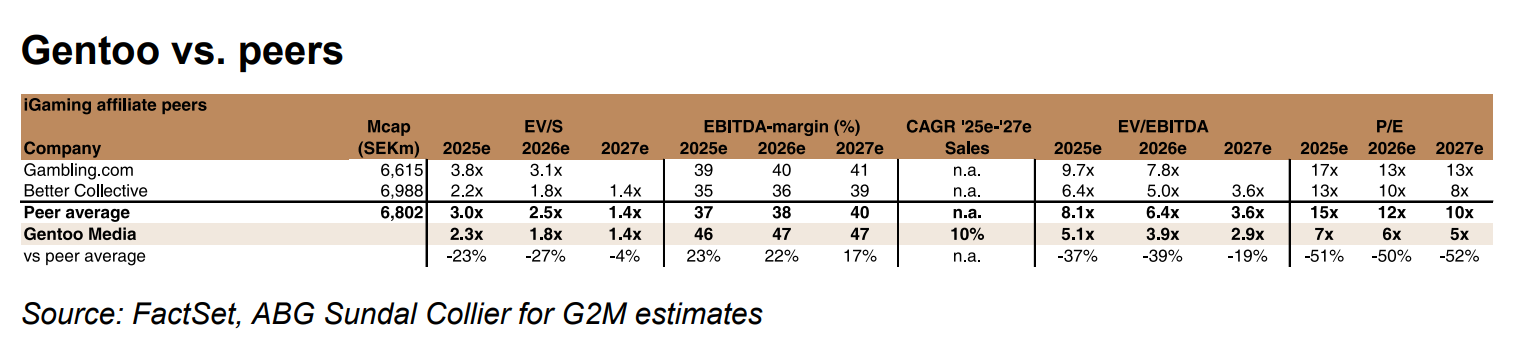

Among analysis firms, ABG and Carnegie (edit: now also Redeye) have already published their updated forecasts, with 2025 averages of 14% revenue growth at 45% EBITDA. EV/EBITDA for these is around 5, and if they can convert approximately 2/3 of this into cash flow as per their comments, the FCF yield is clearly double-digit. The market doesn’t really believe in the company’s future, and peers trade at significantly higher multiples:

Major owner Juroszek has plenty of confidence, having bought another 700k shares and now owning over 18% of the company.