I picked up a small slice of EVO for my portfolio, so I’m opening a dedicated thread here. The company is at an interesting stage, so a few people might find this interesting.

This is a company that produces online casino (Live Casino) games, which has rapidly conquered Europe and is expanding into Asia/America.

ESG investors should not read beyond this point. This is not my favorite business either, but I recognize its high profitability and growth as a platform business with high moats and good scalability. The company receives approximately 10% royalties from all profits of casinos using their gaming tables on a monthly billing basis, without bearing the casino’s loss risk itself.

IR Pages:

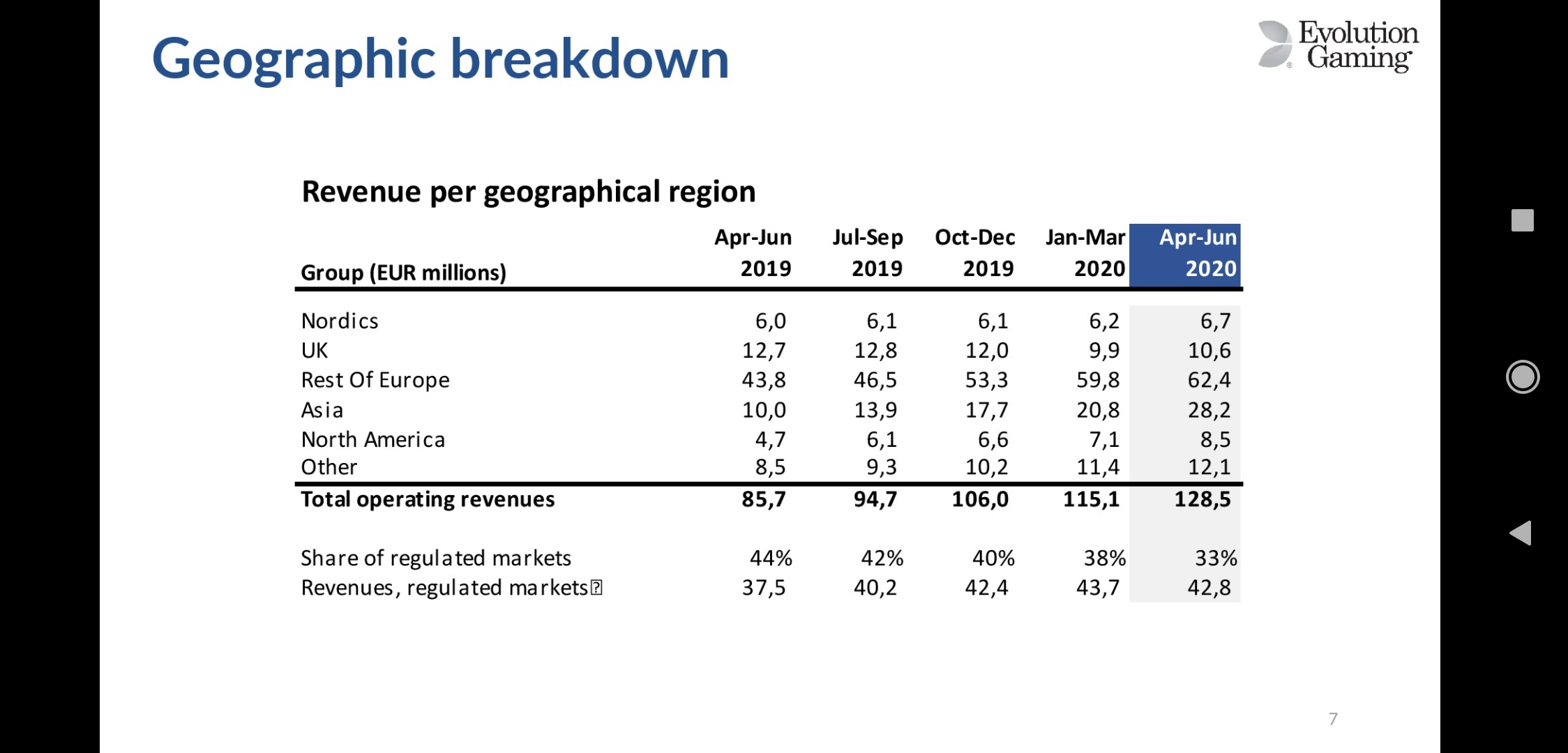

H1/2020 Report:

https://www.evolution.com/sites/default/files/1280416.pdf

Alta Fox’s research from June, which clearly outlines the main aspects of the case:

In addition, the company is being followed by RedEye. They are currently preparing a company update due to a rather significant M&A development (the acquisition of NetEnt) over the summer.

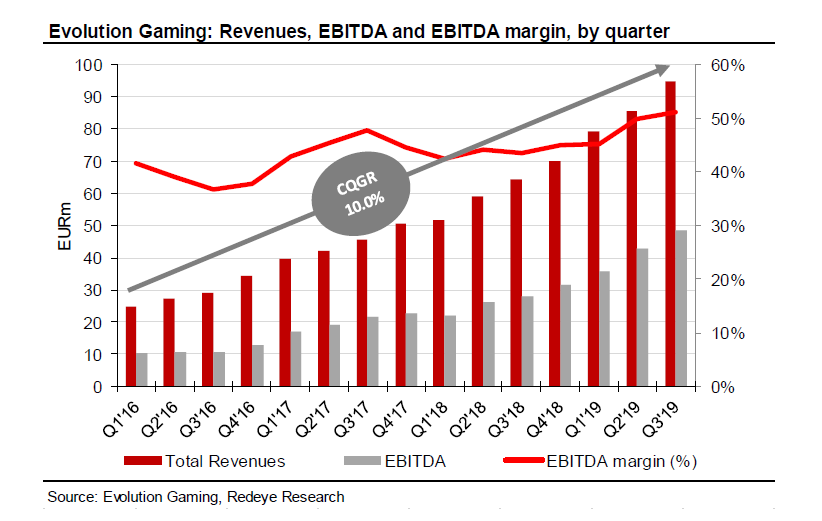

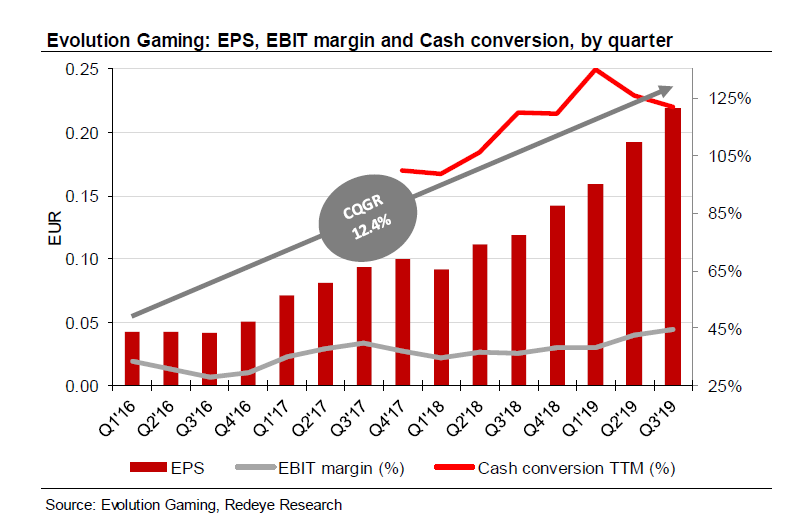

A couple of graphs from Redeye’s somewhat outdated report, illustrating the business’s profitability:

- EBIT margin approaching 50% levels (2019)

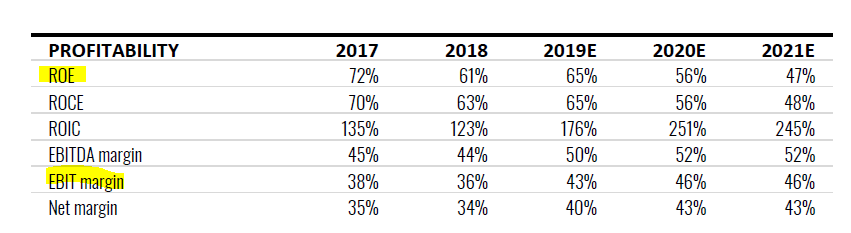

Typical profitability figures from history.

Analysts’ consensus is currently around 720 SEK. Most recently, on 2.10., BofA updated its recommendation to BUY / 715 SEK:

EVOLUTION: DOUBLE WINNER FROM CHANNEL AND PRODUCT SHIFT - BOA

STOCKHOLM (Nyhetsbyrån Direkt) Evolution Gaming has a unique position to capture growth in the online market, and the current share price does not reflect the strong growth prospects.

This is according to Bank of America in an analysis, and as Nyhetsbyrån Direkt previously reported on Friday, the bank initiates coverage with a buy recommendation and a target price of 715 kronor.

“Evolution benefits from a dual growth theme, firstly from a channel shift from land-based, and secondly from existing online markets’ growing demand for live casino,” the bank writes.

The company’s geographical and customer diversification provides additional protection against regulatory risks, and high entry barriers give Evolution a relatively secure position as market leader, the bank believes.

Live casino has high entry barriers, and with large economies of scale, it is unlikely that operators will start creating their own live casino products, it states.

The strong position as a sub-supplier should be further strengthened by the acquisition of Net Ent, which gives the company greater breadth.

“It will also provide a better position to capture growth in the USA; not all states are suitable for the economics behind live casino, but in those states, iGaming shares can be taken by offering ‘non-live’ slot products,” Bank of America writes.

The company will report its Q3 results on October 22, 2020.

https://www.evolutiongaming.com/financial-calendar

Here’s a tracker for player numbers, e.g., for September:

https://insider6.com/sv/evolution-statistik-september/

Updater, here’s a long thread of September player statistics: https://twitter.com/Marcamannen/status/1311414384749617153