What are your thoughts on Etteplan and its current valuation, considering future prospects? I’ve long seen Etteplan as somewhat unexciting and a provider of low-level engineering work, where margins have generally been quite low. I haven’t really followed Etteplan much before, and for some reason, I also imagined that revenue consisted mainly of documentation and traditional resource leasing.

However, now that I’ve learned a bit more about the company, my overall impression has improved significantly. I find the Managed Services particularly interesting, as it offers the potential for better margins. My view is that if they can refine that managed services business model to fit their Central European expansion, the company has truly interesting growth opportunities.

Here’s a link to Inderes’ latest extensive report:

I must admit that Etteplan has always been a bit unfamiliar to me, but now that I’ve learned more about it, it seems like a very interesting company when it comes to its expertise portfolio and market position.

Hei, how do you choose the unlisted companies for comparison in your reports? For example, in the case of Etteplan, Elomatic has been included in the comparison, while RD Velho with a smaller turnover has not made it to the list (small size being one reason?). I understand that RD Velho is, however, growing in its field and competes with Etteplan for the same customers, especially in Finland.

Regarding unlisted companies, we primarily include the largest ones, which usually have the most information available. Even for Elomatic, public information is very limited, which is why the discussion is very superficial.

The greatest added value comes from listed peers, as a lot of information is available about them, they provide public insights into market developments (in addition to their own guidance), and they also serve as benchmarks for valuation levels. Etteplan has quite good comparables in Sweden, on which we have focused the most.

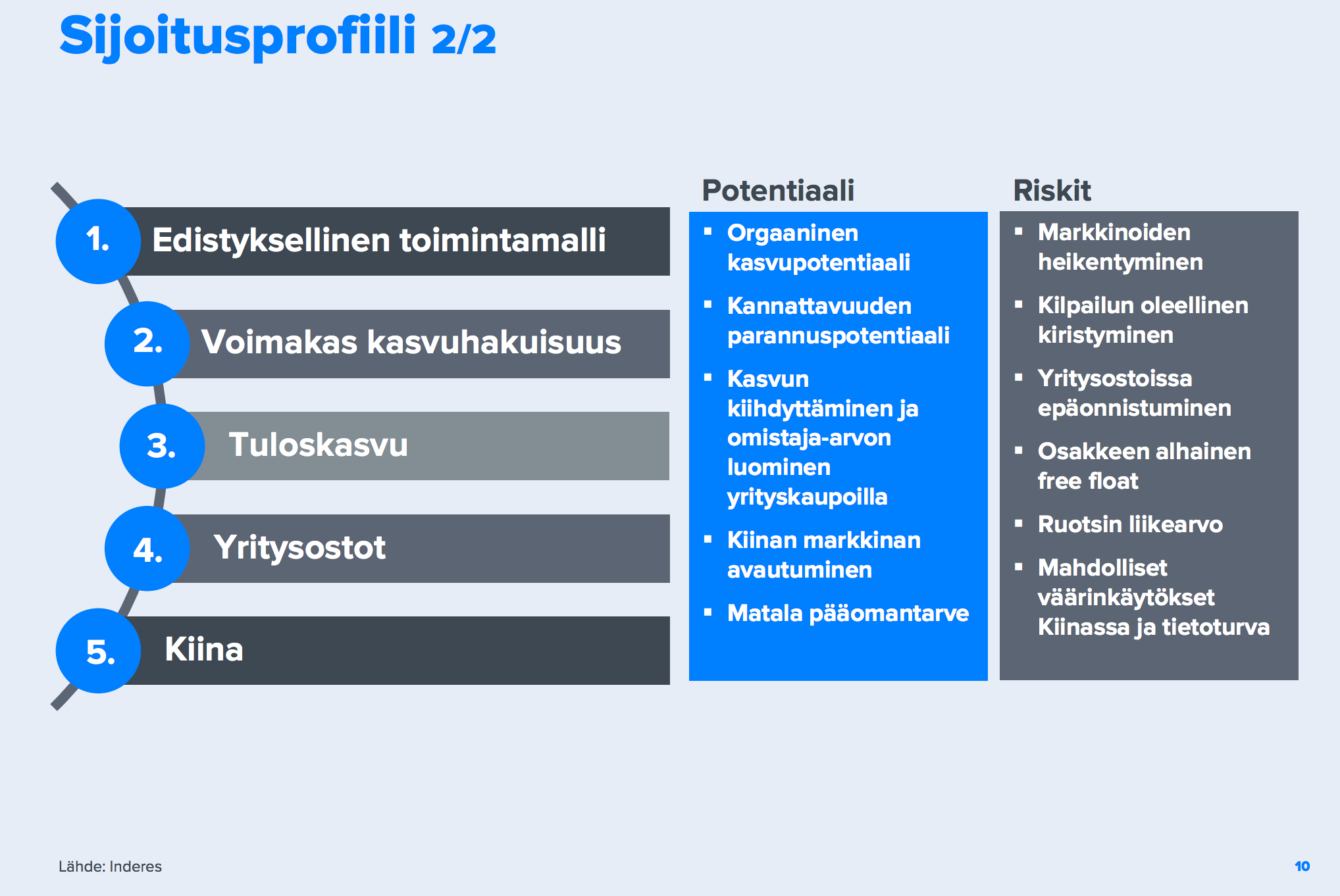

@Juha_Kinnunen How many of Etteplan’s shares are in free float? A few major shareholders seemed to own over 80% of the shares…? How do you think this affects price formation? Trading volume is likely to remain quite small, but ownership is certainly stable.

Ingman Group seemed to have larger stakes in Digia, Qt, and Etteplan. They probably haven’t been dissatisfied for a couple of years I started looking into everything they have, as they seem to be heavily invested in some of the companies in my portfolio.

Where could I see Kyösti Kakkinen’s stock market investments? He probably also has quality holdings, as he’s at the top in Revenio, at least. Well, that was easy to Google…

Etteplan’s free float is indeed small. Perhaps about 80% can be said to be directly “locked,” although in principle they are all always freely traded. I haven’t looked at the statistics recently, but I would guess that genuinely less than 10% of the shares are actively traded.

Due to this, liquidity is low, but on the other hand, I don’t see it as an obstacle for private investors. Larger investors are then forced to trade in blocks. I don’t think this directly affects price formation significantly, but of course, sometimes we can see large price movements with quite small volumes. In other words, even one slightly larger seller/buyer can cause a significant temporary price reaction, but then it normalizes over time.

Initially, low liquidity negatively affects valuation, but when considering how good a main owner Ingman has been for Etteplan, I don’t think this situation can be considered very bad.

I have strong confidence in Ingman Group’s expertise as an owner. They understand long-term business development and value creation for owners. Kakkonen’s portfolio, of course, also contains quality, but it has also included Afarak and other more speculative stuff.

I’m now an Etteplan owner for the 4th time, and this time with a small initial investment. Thanks for the good tips regarding the analyses A little further down, and I might consider a bigger slice. But a 4% dividend is already starting to tempt me. There doesn’t seem to be much debt and the track record is good!

The discussion about Etteplan seems to have frozen, but here are some fresh news comments:

For the company, the flexibility provided by these layoffs is now critical. In Finland, the situation in this regard is very good, and short-term market disruptions do not cause major problems. Of course, the situation changes if the problems become prolonged.

The target price had to be sharply cut based on significantly weakened outlooks, large (negative) forecast changes, and a decrease in acceptable valuation levels as the general risk level rose very rapidly. In our assessment, coronavirus will strongly impact Etteplan’s demand, and a negative profit warning or removal of guidance is ahead, as is the case for a large number of listed companies. I have long been concerned about Etteplan’s cyclicality, and now that risk seems to be materializing - though in a completely different way than I could have even guessed

In my estimation, Etteplan’s fair value is higher than the current share price, and the long-term investor’s expected return is at a reasonable level. However, in the short term, the drivers are mostly negative, and the long-term potential is not highly valued in the stock markets at the moment, as visibility into the recovery of the entire economy is very weak. The recommendation therefore remained on the negative side; we will see how the situation develops.

However, I recommend familiarizing yourself with the case if you haven’t already. This is a very good company, but in this exceptional situation, the company cannot create demand out of nothing.

Let’s dig this thread out of the mothballs. After a relatively good Q2, the target price updated to €9.5 and a “Add” recommendation, I joined the owners’ club today. I also see a small possibility of a positive earnings surprise for this year, as H1 wasn’t far behind last year. Based on the interview led by @Juha_Kinnunen, the most important thing would be to start new projects with large customers in Finland. Elsewhere, markets have started to recover, and China is doing well.

Good to bring this out of mothballs! Etteplan has quite unnecessarily been left out of these discussions.

Regarding Etteplan, I made a fresh mistake during this COVID period It would have been a great opportunity to buy a quality long-term case, but I myself had a reduce recommendation during that period (and of course, before that too). There were reasons for that, mainly the feared cyclicity of Etteplan and the strong impact of COVID on demand, but in hindsight, it’s easy to say that the concerns were greatly exaggerated. The forecasts were too negative, and through that, the valuation looked challenging, so we waited for better buying opportunities.

Well, the effects of the COVID-19 pandemic were ultimately clearly smaller than the worst fears, and on the other hand, Etteplan’s ability to defend profitability was particularly impressive and a positive surprise. The situation is not entirely over yet, of course, but confidence in the company’s ability to generate results even in a difficult market situation has clearly increased. I’m especially annoyed that I wrote in both reports during that COVID period that the company’s fair value was higher than the current share price (to varying degrees), but still chickened out with the recommendations If only someone had read those reports carefully and bought…

But one must learn from mistakes, and now a quote from a recent report: “Based on recent performance, we have changed our view of Etteplan’s risk profile to lower than before, which we believe also positively reflects on an acceptable valuation. We previously clearly underestimated Etteplan’s ability to generate results in a difficult market situation and thereby missed the buying opportunities offered by the COVID-19 pandemic. However, we believe that the stock’s risk/reward ratio is clearly positive even at the current price.”

The morning comment can be read here and the link to the full report is here (Premium). I recommend checking it out

No worries, my man! I read your reports carefully and bought some a couple of weeks ago.

My TA (technical analysis) outline and exchange with DayTraderXL can be found in the TradingView thread. He also promised to look into it, and perhaps even bought some.