Etteplan will release its results next Thursday, and here are Juha’s pre-result comments regarding them.

Etteplan reports its Q2 results on Thursday at around 1:00 PM. We expect high single-digit revenue growth from the company, which is primarily driven by completed acquisitions. However, we also expect slight organic growth from a weak comparison period. We forecast robust earnings growth driven by growth and improving profitability. The main focus in the report will be on the outlook, market development in various sectors, and the sustainability of the company’s own earnings performance. The emerging signs of a pick-up in market demand from early in the year have not yet been confirmed, and no clear improvement has been seen in industrial indicators. Estimates for the remainder of the year’s development are therefore important in an uncertain situation.

Mr. Juha interviewed CEO Juha about the company’s Q2 and outlook, among other things.

Topics:

00:00 Start

00:08 Q2 key highlights

01:27 Difficult market situation

02:22 Distribution of engineering design and R&D

03:35 How to improve the demand situation

05:19 Geographical differences in the business

06:32 Outlook for customer segments

07:34 Reasons for the weak result

08:55 Geographical differences in profitability

09:26 Minority investment in Bangladesh

11:17 Bangladesh’s impact on Etteplan’s customer projects

12:05 Future plans for cooperation

12:36 Bangladesh and India

13:35 Cooperation with Konoike

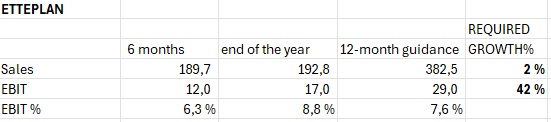

15:12 Current guidance

15:57 Drivers for maintaining the guidance

16:49 Outlook for the rest of the year

In his old age, Pitkä-Jussi has started working nights, and as a result, we received a fresh company report.

We are downgrading Etteplan’s recommendation to Reduce (prev. Accumulate) and the target price to EUR 13.0 (prev. EUR 15.0). The Q2 result was a clear disappointment for us, as broad-based weakness in demand significantly weighed on the results of all service areas. Guidance ranges were revised downwards, but reaching the lower end of the range for the result requires a clear and rapid recovery in demand. We consider this unlikely and doubt the sustainability of the earnings guidance. The conflicting valuation could be described as somewhat high in the short term (2024e EV/EBITA 12x) and quite attractive in the long term (2026e EV/EBITA 8x), but in the current situation, short-term risks weigh more heavily.

Quoted from the report:

There are still clear differences in demand outlooks by customer industry. The defense industry and, with slight reservations, the energy industry continue to stand out positively among the sectors. Sectors that weakened during the quarter were especially the metal, mining, forest, and chemical industries.

It’s always been that way on days with three (or more) earnings reports There isn’t really time to write during the day when there are also interviews and conference calls. But usually, they’ve been published “refreshed” in the morning.

Even Juha’s forecast was a notch above the upper end of the new guidance, meaning that although Inderes was expecting a profit warning, they didn’t expect it to be this drastic.

Juha has published a new company report following the profit warning.

We reiterate our target price of EUR 13.0 for Etteplan, but upgrade our recommendation to Accumulate (prev. Reduce). We were expecting yesterday’s negative profit warning from the company, but its magnitude put further negative pressure on our forecasts for the coming years. The market situation has not picked up, and no significant improvement is expected for the remainder of the year either. Still, we believe the market bottom is already at hand and see Etteplan as being well-positioned to benefit from the eventual turnaround. Looking even slightly further ahead, the stock’s valuation (2025e EV/EBITA 10x) is moderate in our view, and the risk/reward ratio turns positive again.

Kinnunen has shared his thoughts on Etteplan after the second profit warning.

After the company’s second negative profit warning, investor confidence is being tested, but we consider the company’s problems to be fixable and still see the long-term investment story as attractive. Etteplan’s valuation is not yet at rock-bottom levels (2025e EV/EBITA 10x), but the upside is sufficient for a buy recommendation. The best buying opportunities arise when good companies encounter temporary problems.

Etteplan reports its Q3 results on Thursday at 1:00 PM and here are Juha’s pre-comments regarding them.

The company has issued two negative profit warnings since its Q2 results, so it is likely clear that the Q3 result will not cause any shouts of joy. The market situation is known to be very difficult, especially in Finland, and the company has responded to the weakness with new efficiency measures. These incur costs, and in addition, the company has also made exceptional errors. The outlook for the rest of the year is weak, but our focus has already turned to next year and whether the company can be guided back onto the path of profitable growth. According to our assessment, the current problems and gloom will ultimately prove to be temporary, but we will review this assessment critically in connection with the Q3 report.

Mr. Kinnunen has crafted a new company report following Q3.

Q3 results were as weak as expected, and there were no surprises in the outlook as the gloom continues for now. Consequently, forecast changes remained minimal, and the situational picture remains unchanged. Etteplan’s valuation is not quite at rock-bottom levels (2025e EV/EBITA 10x), but the upside is still sufficient for a Buy recommendation. The best buying opportunities arise when good companies face temporary problems, and we estimate Etteplan’s challenges to be ultimately transitory.

00:00 Introduction

00:14 Q3 highlights

01:50 Profit warnings

03:46 Germany

04:38 One-off items

05:10 Salary payments in Sweden

06:46 Acquisitions in Central Europe

09:09 Market situation

11:18 Next year

12:42 Strategy

13:22 AI

Let’s post a little something in this dead thread.

Etteplan doesn’t seem to be sparking much passion in anyone.

Indeed, the thinking seems to stem from the idea that Etteplan is a good company and the problems are temporary:

“The best buying opportunities usually arise when high-quality companies encounter temporary problems, and in our opinion, Etteplan’s current situation meets these criteria. The risk, of course, is that there have been more permanent weakenings in Etteplan’s business or competitiveness that we haven’t noticed.”

The company has issued two profit warnings this year and now missed estimates again, but the trust remains

I Googled Etteplan as an investment:

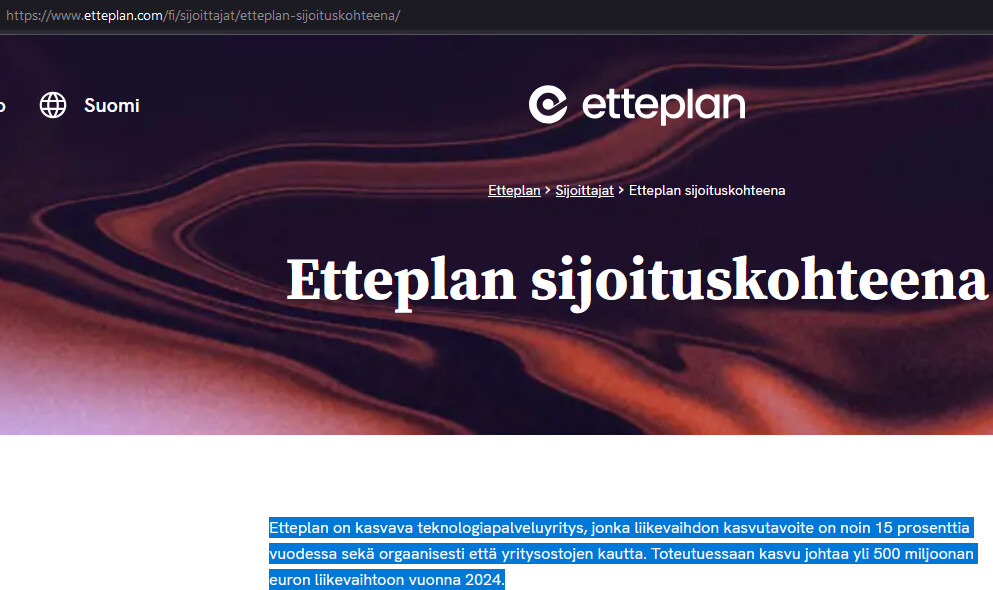

Yeah, with growth materializing, 500 million in revenue, wonder if that’s happening…

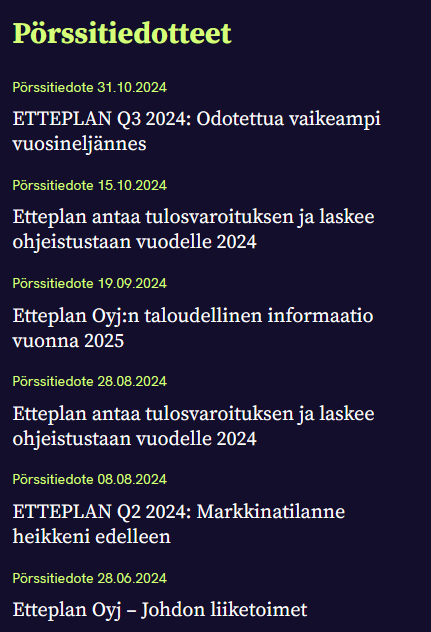

Stock exchange releases from Etteplan’s website in order:

insider sale

interim report - doing poorly

profit warning

next year’s calendar

profit warning

interim report - doing poorly

Analysts from both Inderes and Evli are confident.

Let’s wish the company all the best, but things are looking interesting.

Personally, I don’t believe Etteplan will fare very well in the future either. The company is unable to compete for top talent because they would actually have to pay them a decent salary. This is reflected in the exodus of high-level experts in a tightening talent market. I actually work at this firm myself, and I wouldn’t invest in the company.

Thanks and congratulations. It’s refreshingly honest to come and say that the company is far too expensive with employees like yourself.

This might be a stupid question since I don’t know the industry dynamics very well, but in Etteplan’s case, is it possible to bring in those mentioned high-performers to replace the “average Joes” once the market picks up? Or is it just the nature of the industry that good people don’t move to where the money is when needed? I seem to recall the CEO mentioning, at least indirectly in some interview in the midst of the slump, that they are saving their ammunition for better times. Or is this aforementioned powder wet in Etteplan’s case?

Working in the industry, I can say from experience that these so-called top performers certainly know their worth. If the salary isn’t competitive or the demands of the role don’t meet their expectations, they will switch jobs quickly!

This leads to your question: As the market picks up, competition for top talent will be extremely intense, and luring an employee back is always harder once they have already left. As @Loiskuttaja noted, Etteplan may find it difficult to attract these top performers to replace the “average Joes”—especially if they are currently losing them to competitors or clients.

I can’t comment on what kind of resources Etteplan has set aside for this market recovery phase to compete for employees.

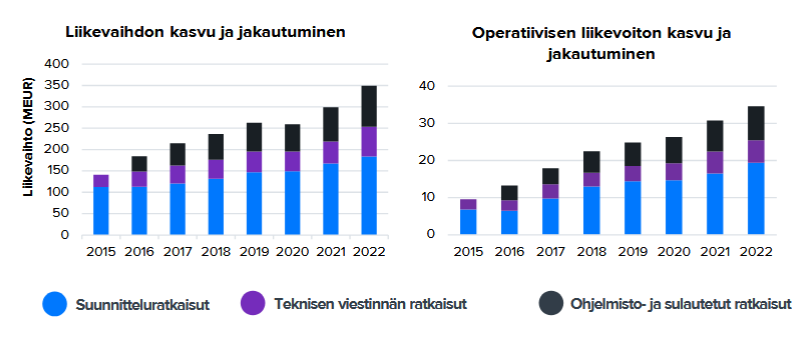

Etteplan certainly had quite good growth for several years before interest rates rose at the end of 2022.

In 2023, several IT companies anticipated a faster decline in interest rates and provided guidance accordingly.

Often, profit warnings have had to be issued, and guidance has been lowered.

On the other hand, IT companies have been competing for customer projects, which has pushed prices down; therefore, it might not be the best market for raising salaries.

Of course, someone might know Etteplan’s salary structure well.

If staff salaries are not transparent and people do not talk about them freely, it is difficult to know the actual salaries.

For example, as a lead architect, I have paid salaries based on productivity, and in the IT sector, productivity varies greatly between experts (especially the more advanced the required expertise).

Now that the IT services market has shifted in a direction where larger companies especially have their own coders, it may slightly change the role of traditional software firms (Siili, Vincit..).

Since Etteplan offers both mechanical and software design (e.g., embedded systems), customers do not easily undertake such projects with their own resources, which can be an advantage for Etteplan.

Of course, Etteplan has technical documentation as an addition.

Time will tell which companies return to growth as customers begin investing in IT projects again.

I have a small position in Etteplan, and I don’t feel particularly emotional about it, as I naturally don’t about any of my stocks.

The atmosphere seems to be exactly what I would expect after the past year. I have followed Etteplan for over a decade now, which I believe gives some perspective on the company’s situation. Additionally, there are many other companies in the sector and in B2B services in general that are also complaining about the market situation, especially in Finland. Of course, that doesn’t mean I’m right with my recommendation, but I think it gives me a pretty good overall picture.

Thanks for the comment! Has the talent market really tightened at the same time as demand has decreased? Are so many people retiring in Finland too (a clear problem in Germany)? Of course, there is always a shortage of certain skills, but I haven’t thought of this as a broader trend right at this moment.

In my experience, there have always been experts who have found better pay or more appreciation in other companies. I personally know some people in the sector who have also been at Etteplan and left. This is very natural, and they didn’t seem bitter. It hasn’t been an obstacle to the company’s success before, and I find it hard to believe it would be in the future either. In my opinion, it’s just the market’s pricing mechanism and part of the industry dynamics. In any case, I appreciate all comments from experts in the sector, especially when they disagree and bring new information to me

This would have been realized if the Semcon acquisition had gone through in 2022. It didn’t, as they withdrew from the price competition. I reckon it was probably good that they didn’t enter a down market with high leverage. After that, it was practically known that the goal wouldn’t be reached. However, it remains the goal as long as the strategy is updated, which is coming in December. I think it’s better not to just bury it but to be honest about how it went.

Yep, no one is cheering for this year. It has been miserable. I don’t know about Evli, but we have been on a “buy” recommendation for almost 3 weeks. No need to panic about that yet.

Recruitment is one of Etteplan’s key tasks, so one would hope so. Etteplan is traditionally quite strict with idle time and people are on furloughs, so it’s no surprise that people leave. One might get the impression from the comments that they are all top experts and then only “handymen” are hired to replace them, but I don’t really believe this is the whole picture. There is demand for top experts even in a bad market, and it’s also easy to pay them if and when customers are willing to pay for them. There are certainly exceptions, and there has always been a transition both to customers and competitors. I would think of this as a similar dynamic to the basic rule of sales: if you have never lost a customer because of price, you can’t know what the “right” price level is. I certainly need to dig into this matter more!

I have to say that economists make those interest rate forecasts — we don’t take responsibility for them But yes, they went completely wrong there too.

We haven’t done comparisons in a while, but generally, I think Etteplan has been an average payer in the industry. So these comparisons can be made from reported figures (number of personnel and personnel costs). It always mixes things up a bit since companies operate in different countries with different levels, and the reporting isn’t always top-notch.

Here are some basic thoughts for the discussion! All from memory, so I’m escaping responsibility