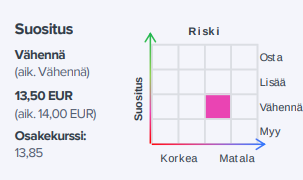

Etteplan’s Q3 results fell short of our forecasts even after the negative profit warning, and surprisingly, reaching the guidance requires a strong end to the year. The market situation is challenging and next year’s outlook remains blurry, which put slight pressure on our earnings forecasts. The stock’s valuation is reasonable (2024e adj. P/E 14x), but in the short term, we do not consider it attractive as the cycle may potentially weaken further.

Etteplan issued a profit warning and here is the release almost in its entirety below:

Etteplan Oyj, Stock Exchange Release/Inside Information January 18, 2024 at 8:00 a.m.

Etteplan issues a profit warning

According to preliminary results, Etteplan’s 2023 revenue is approximately EUR 359 million and operating profit (EBIT) is approximately EUR 25.4 million

In its interim report published on October 31, 2023, Etteplan Oyj estimated the Group’s 2023 revenue to be EUR 355-370 (2022: 350.2) million and 2023 operating profit (EBIT) to be EUR 26-28.5 (2022: 28.6) million.

Etteplan’s 2023 revenue is in line with the guidance and, according to preliminary results, is approximately EUR 359 million. The 2023 operating profit (EBIT) falls short of the guidance due to weaker-than-expected business development in the final quarter of the year and, according to preliminary results, is approximately EUR 25.4 million.

Etteplan’s lower-than-expected earnings level was affected by a weakening demand situation, high levels of sick leave at the end of the year, and a higher-than-expected number of holidays taken during the Christmas period. Additionally, the result was weakened by corrections in cost entries.

Etteplan will publish its Financial Statement Release for January-December 2023 on Thursday, February 8, 2024.

Here is a fresh company report on Etteplan from Juha.

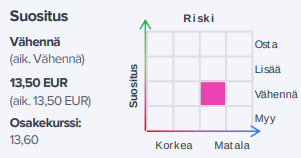

Etteplan’s previous negative profit warning was expected and did not cause material changes to our forecasts. The market situation has remained challenging and customer activity seems to have weakened slightly further, but in our view, the outlook has not changed dramatically. We believe the stock is fairly priced (2024e EV/EBITA 12x), but considering the cyclical risks, we do not find the risk/reward ratio attractive.

Quoted from the report:

Our own expectations for the current year were already set at a moderate level, so for 2024, we have so far only made downward revisions of a few percent. At the same time, it should be noted that we still assume the market will recover toward the end of 2024, the uncertainty of which has increased along with interest rate cut expectations, among other things. The cyclical risk remains significant, even though Etteplan is good at defending its profitability. Visibility into 2024 will improve after the financial statements.

Juha’s pre-commentary as Etteplan releases its Q4 results on Thursday.

Etteplan will publish its financial statement bulletin for 2023 on Thursday, February 8, 2024, at approximately 1:00 PM. Despite the negative profit warning and significant headwinds, the Q4 result will be reasonably good. Following preliminary information, the Q4 result is mostly known, and attention in the report will focus on the 2024 outlook and guidance, as well as the development of various segments. In 2024, the company is expected to be able to improve its earnings, even though the market situation remains challenging, at least in the early part of the year.

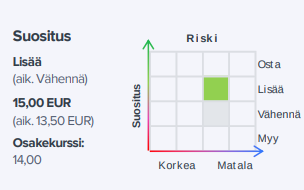

Etteplan’s guidance for 2024 was more positive than expected, and there was strong confidence in the market recovery, although there is still great uncertainty regarding the timing. This year, however, Etteplan will return to earnings growth, providing a critical driver for the stock moving forward. The stock’s valuation is relatively neutral (2024e EV/EBITA 11x), but the long-term outlook and previous strong track record of value creation make us turn positive.

@Juha_Kinnunen Etteplan’s financial targets; “We are targeting approximately 15 percent annual revenue growth, which, if achieved, will lead to a revenue of over 500 million euros in 2024.” In the analysis, however, revenue is under 400m and even in a couple of years well below that 500 million mark. In your opinion, is the company’s guidance realistic in the current market? Is it possible to reach the targeted levels through potential acquisitions and the expected growth in the order book? The CEO didn’t exactly promise much for Q1 in the interview.

Now financial targets and guidance are being confused, which are very different things. That EUR 500 million revenue is no longer realistic without a major acquisition, which at this stage is already very unlikely. In late 2022, Etteplan had a significant acquisition of Semcon in its sights, but this fell through due to a higher bid for the company. That would have brought them to that size category, but it’s better that they didn’t start overpaying.

Financial targets are precisely targets, and they are always set for a longer period. Usually, they are quite challenging, meaning everything has to go perfectly to reach them. But it’s actually sensible for targets to be high. In contrast, there must be sound reasoning and realism behind the guidance, and these estimates must be updated if they are no longer justified. If this isn’t done, the FIN-FSA (Fiva) should essentially be knocking on the door.

Etteplan’s guidance for 2024 is as follows:

2024 revenue to be 375-415 (2023: 360.0) MEUR, and

2024 operating profit (EBIT) to be 28-34 (2023: 25.5) MEUR.

Yeah, I probably asked unclearly. I saw the guidance, but I was wondering about the financial target for 2023–24 not being changed. So, a potential acquisition and its success could still provide the means to reach it. Perhaps that’s what the strengthening of the cash position refers to. And of course, guidance evolves according to the situation; there’s certainly room to reach the target. Thanks for clarifying!

Financial targets are rarely changed in the middle of a strategy period, which is understandable in itself as the strategy and targets are fundamentally linked. Both are then updated at once when the period ends and a new one begins. At that point, companies with good communication also report how they performed relative to previous targets and explain any deviations. That is honest conduct.

On the other hand, many companies also have “strategic” or “medium-term” targets that don’t really ever move and there doesn’t seem to be a clear path to them. They then reflect more where the company sees its own potential. Without actions or a development path toward the targets, they can however be dismissed as a curiosity. Sometimes you also see targets simply being forgotten when they are found to be unrealistic and the company no longer bothers to explain. This is not recommended practice.

Thank you, and I apologize if I misunderstood your question a bit. Many people just seem to put a bit too much weight on financial targets, which is why I wanted to establish that distinction just in case.

Here are Juha’s preview comments as Etteplan reports its results on Wednesday.

Etteplan reports its Q1 results on Wednesday at around 1:00 PM. We expect the company’s key figures to have remained roughly at the level of the comparison period, which would be a reasonable performance as the market situation likely provides a slight headwind. The main focus in the report will be on the outlook, market development in different sectors, and the sustainability of the company’s own earnings performance. We suspect that the market will not provide any tailwind in the coming quarters either, but we estimate that Etteplan will still perform well thanks to internal efficiency.

CEO Juha Näkki was interviewed by analyst Juha Kinnunen.

Topics:

00:00 Introduction

00:12 Key highlights of the early year

01:14 Market outlook

02:40 Market areas

03:07 Better situation in Sweden

03:54 Central Europe

04:42 China

06:10 Is India the next China?

06:52 Decent performance in profitability

07:57 Service areas

08:43 Cash flow

08:59 AI

Juha has published a fresh company report following Q1.

Etteplan’s start to the year offered no significant drama: the Q1 result was roughly in line with our expectations, and there were no material changes to the outlook. There is uncertainty surrounding the market recovery expected in the latter half of the year, but we consider it likely that the market bottom is currently at hand. Once the turnaround occurs, Etteplan’s earnings growth will accelerate, making the stock’s valuation level quite attractive (2024e EV/EBITA 11x).

Here’s a comment regarding the AFFRA acquisition. Quite an interesting small company!

Just for your information, key figures for all Swedish companies can be found on the allabolag.se website without fees or registration. It’s a useful site for this basic information, much like Finder and similar services in Finland.

Etteplan acquires a stake in Bangladesh’s largest IT consulting company.

Technology service company Etteplan, which serves the world’s leading industrial companies, is increasing its global delivery capability and acquiring a 19.99% minority stake in BJIT, a global IT consulting company headquartered in Dhaka, Bangladesh. The transaction expands Etteplan’s geographical delivery network and brings significant new, cost-effective specialized expertise to its use.

@Roni_Peuranheimo provided his comments on Etteplan’s recent acquisition.

Etteplan is acquiring a 19.99% minority stake in BJIT, the largest IT consulting company in Bangladesh. The news was announced via a press release, and we do not believe the investment was particularly large in the context of Etteplan’s scale. However, it is an interesting new geographical expansion, where we see certain optionality in addition to the supporting effect it brings to the delivery network.

Software company Etteplan and engineering company Elematic have agreed that Elematic’s technical documentation department operating in Akaa will be transferred to Etteplan through a transfer of business.