Julkaisimme tänään päivityksen Etteplanista. Ei mitään dramaattista eikä muutoksia ennusteisiin, vaikka epävarmuus markkinakehityksen suhteen on toki kasvanut. Toisaalta arvostustaso on nyt laskenut merkittävästi viime vuoden lopusta.

Aamukatsauskommentti sisältää tällä kertaa käytännössä koko tarinan:

Etteplan täräyttää ja tekee Semconin hallituksen suosittelemaan ostotarjouksen. Etteplanin markkina-arvo on n. 380Me, tarjous 260Me, eli olisi iso harppaus:

Ehkä varteenotettavampaa vielä lv-vertailu: Etteplan 350Me, Semcon n 160Me, eli ehkä n 45% epäorgaaninen kasvu oston myötä. Semconin lv ei ole juuri kasvanut, mutta muut luvut parantuneet viimeiset viisi vuotta suht nätisti:

Tarjouksessaan 23.8.2022 kerrotun mukaisesti Etteplan ei korota omaa tarjoustaan.

Etteplan kirjaa kaupan valmisteluun liittyvät kertaluonteiset kulut kuluvan vuoden kolmannelle vuosineljännekselle. Taloudellinen ohjeistus vuodelle 2022 säilyy kuitenkin muuttumattomana.

Lisäksi kaupan valmisteluun liittyvällä valuuttasuojausriskillä on merkittävä negatiivinen vaikutus rahoituseriin ja siten osakekohtaiseen tulokseen kolmannella vuosineljänneksellä. Valuuttasuojauksen lopullinen vaikutus kirjataan yhtiön neljännen vuosineljänneksen tulokseen.

Ohessa tuore raportti ja tässä toisaalta kaikille vapaa aamarikommentti:

En tiedä, olenko nyt liian nössö Etteplanin kanssa. Koko sektorin arvostushan on tällä hetkellä suhteellisen maltillinen, kun markkinat odottelevat taantumaa ja investointien laskemista. Joillakin sektoreilla se on lähes varmaa, mutta toisaalta on tässä lähivuosina myös paljon voittavia sektoreita ja teollisuusinvestoinnit yleisesti voi hyvinkin yllättää positiivisesti Euroopassa, kun mennään läpi tästä murroksesta.

Silti heikon näkyvyyden kanssa varmaan turvallisempaa pelata puolustuspeliä, ja yhtiökin oli vähentänyt rekrytointeja. Lyhyen aikavälin kasvunäkymä lienee vaisu, kun korkealta kysyntätasolta lähdettiin, ja kannattavuutta on silloin ainakin vaikea parantaa. Jäätiin sitten seuraamaan vielä sivusta, mutta mielenkiintoista nähdä miten markkina lähtee kehittymään. Luottamus on kuitenkin vahva siihen, että Etteplan navigoi heikossakin markkinassa onnistuneesti.

The discussion isn’t very active here, so allow me to give a small shout-out to Etteplan’s Juha Näkki. It really caught my ear when the CEO mentioned that the Cognitas acquisition in technical documentation had gone wrong AND further stated that the problem has been identified and they know how they are going to solve it and on what schedule. Exemplary straightforward behavior!

I hear these kinds of things quite rarely, and it feels like it’s always easy to hide behind some excuse (after all, no one wants to admit mistakes). Without knowing the company better, this at least boosts my confidence in the company, and Etteplan will surely be wiser in future acquisitions, so let’s add this company to the watchlist now.

Juha has produced an excellent new extensive report on Etteplan. Extensive reports are available for everyone to read.

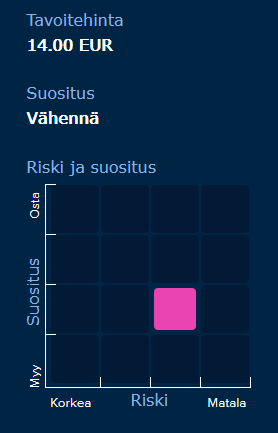

Technology service company Etteplan’s growth story continues thanks to its diverse expertise, even in a slight market headwind. The company’s track record of profitable growth is strong and earnings growth will continue, but in our assessment, the growth rate will decrease from historical levels as profitability improvements become increasingly difficult. The share valuation level is reasonable (2023e adj. EV/EBITA 12x), but we see no upside while uncertainty remains high.

This thread has been without a single post for almost three months. Here are Juha’s preview comments, as the company releases its Q2 report on Thursday.

"ETTEPLAN Q2 2023: Growth slowed in a difficult market situation

Key highlights April-June 2023

The Group’s revenue grew by 0.7 percent and was EUR 89.8 (4-6/2022: 89.3) million. At comparable exchange rates, revenue grew by 3.2 percent.

Operating profit (EBITA) decreased by 8.9 percent and was EUR 7.4 (8.1) million, or 8.3 (9.1) percent of revenue.

Operating profit (EBIT) decreased by 10.3 percent and was EUR 6.1 (6.8) million, or 6.8 (7.6) percent of revenue.

Cash flow from operating activities was EUR 8.9 (4.4) million.

Basic earnings per share were EUR 0.15 (0.22).

Etteplan narrows its guidance for revenue and operating profit (EBIT) within the previously published range and estimates: 2023 revenue to be EUR 360-380 (previously 360-390) million, and 2023 operating profit (EBIT) to be EUR 28-31 (previously 28-33) million."

I wonder if the high share price will hold up against these numbers; I’m a bit skeptical. And yet (DISCLAIMER), I do own it.

@Juha_Kinnunen interviewed CEO Juha Näkki regarding the Q2 results and the company’s outlook.

Topics:

00:00 Introduction

00:14 Q2 highlights

01:45 Engineering Solutions

02:52 Technical Communication Solutions

04:28 Software and Embedded Solutions

06:30 Outlook for the rest of the year

08:43 Competitive landscape

10:26 Guidance

Etteplan Oyj estimated in its interim report published on August 10, 2023, that the Group’s revenue for 2023 would be EUR 360-380 (2022: 350.2) million and operating profit (EBIT) for 2023 would be EUR 28-31 (2022: 28.6) million.

Etteplan is now updating and refining its previous estimate for the 2023 revenue and operating profit due to weaker-than-expected business development in the third quarter. According to the new estimate, revenue is estimated to be EUR 355-370 million and operating profit (EBIT) to be EUR 26-28.5 million.

Here are Juha’s pre-comments as Etteplan releases its Q3 report on Tuesday.

Etteplan will release its Q3 report on Tuesday at approximately 1:00 PM. Following the negative profit warning issued by the company in September, it is clear that it has been a challenging quarter. We expect the company’s revenue to have grown slightly, but the operating profit to have weakened from the level of the comparison period. In the report, areas of particular interest include the outlook, estimates regarding the duration of the weak market situation, and the company’s measures to rectify earnings performance.