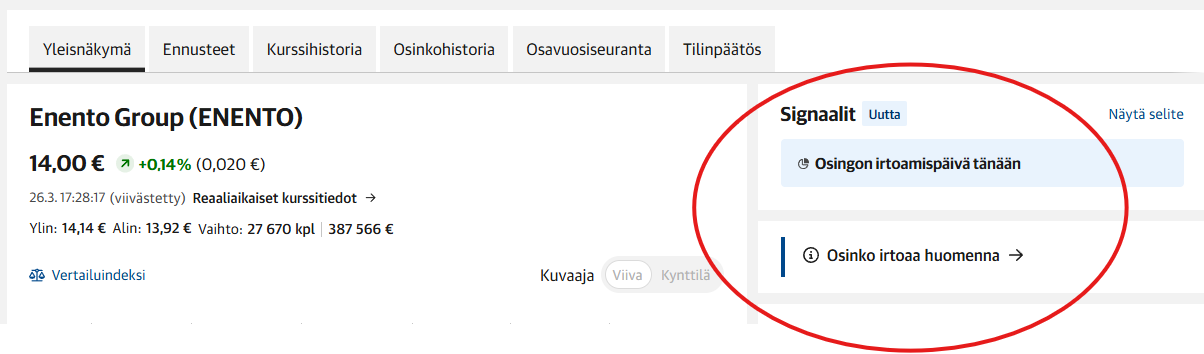

It’ll be interesting to see if there’s still an ex-dividend drop tomorrow, as Inderes’ dividend calendar, for example, marks tomorrow, March 26th, as the ex-dividend date, even though the dividend doesn’t go ex until March 27th. I was wondering earlier why Kauppalehti said “Dividend goes ex in 2 days,” but it was actually correct there.

The record date (täsmäytyspäivä) has been set up a bit annoyingly, causing unnecessary confusion. I’ll make additions tomorrow if it dips for no reason.

Soon we will see who is the buyer of the block. I would guess the Bromans or Mika Heikkilä’s magic touch. We’ll see soon. From the above call and otherwise, Paavola’s delivery is somehow convincing, and he immediately got things moving. And it’s nice that he’s putting more chips into the company he leads!

Likewise, a good presentation at today’s general meeting. It covered, among other things, thoughts on AI. Let’s hope the presentation will be available on the company’s website for everyone to see.

Will the dividend detach today or tomorrow? According to Inderes’ stock calendar, it should detach today, but Nordnet says tomorrow. At least the stock hasn’t reacted as if it would detach today:

Where can you see who bought the block? The amount was so small that it will get lost in the noise on the ownership list. The dividend will be ex-tomorrow, as discussed above.

On the other hand, given that the cumulative volume of the stock has increased by 800,000 shares since the last listing, a block of 10,000 shares will, of course, get lost in the noise.

It seems that the Sp fund has been selling regardless of price. In many other company threads, Säästöpankki’s (Savings Bank) small-cap funds have been revealed as net sellers, while Proprius has increased its holdings: Osakkeenomistajat ja liputusilmoitukset - Enento

Interesting changes in the owner list. Especially Teppo Paavola’s ownership is already quite significant, not just a formal ownership of a few shares. There are also a few other interesting additions, such as Savolainen and Two Sigma’s buy-ins. It would be interesting to know what they now see significantly improving in Enento?

However, the macro outlook is subdued, there is still a slight fear of regulatory changes in Sweden, and the organization still does not seem to have growth ambitions, focusing only on beautifying EBITDA and paying dividends.

I am still of the opinion that Enento is a great company with potential for so much, their data management expertise is at an incredible level already in their basic products, and they could build new sales channels abroad for all product areas (excluding credit information) at any time, but there still doesn’t seem to be any interest. The guidance at the beginning of the year was a huge disappointment due to the new CEO, which has started to erode faith in a real growth strategy, meaning Jäger’s line continues (everything out as dividends and taking care of old customers).

Here are Roni’s preview comments as Enento reports its Q1 results on Tuesday, April 28.

We expect Enento’s revenue to have grown moderately, albeit primarily driven by currencies. We also expect the result to have improved slightly from the comparison period. The presentation of the new operating model and how the result is divided between country-specific segments will be one of the interesting takeaways of the report, as the company has not yet published comparison figures for its new reporting. Additionally, we naturally focus on the development of the demand outlook, regarding which the war in Iran has once again raised risks.

“The negotiations concern all Enento employees in Finland and Sweden. According to a preliminary estimate, the planned measures could result in a reduction of up to approximately 60 full-time equivalents (FTE).”

Quite significant negotiations, given that Enento has a total of just under 400 employees. I believe that AI and other technological developments partly enable such major efficiency measures in this company.

No major surprises in the big picture. When looking at the historical profitability of Asiakastieto, it is no surprise that the Finnish business’s profitability is clearly the strongest among the segments. But Sweden’s profitability isn’t bad either, considering the country’s revenue development in recent years. Of course, there is no precise information on what the profitability levels were a few years ago. Norway/Denmark’s profitability is also already at a good level, despite being a smaller business.

Are the significantly higher “materials & services” in Finland due to the state’s high data delivery costs? Of course, there are many other data providers as well: banks, debt collection agencies, etc., but what explains Finland’s high cost structure?

To my understanding, that is exactly it—the costs of procuring public data are relatively higher in Finland. We saw quite significant price increases in these in Finland after the inflation peak, which the company naturally passed on to its prices.

Here are Roni’s “official” comments regarding Enento’s change negotiations.

Enento Group announced on Wednesday that it is initiating change negotiations in Finland and Sweden. According to a preliminary estimate, the planned measures could lead to a reduction of a maximum of approximately 60 full-time employees. The change negotiations were not a major surprise, given the updated organizational model by the new CEO Teppo Paavola and the continued weak demand environment, but their scale is surprisingly large. We will likely hear more details about the background of the change negotiations in connection with the company’s Q1 results next Tuesday, at which time our forecasts will also be under review. Enento also published comparative figures for 2025 yesterday for its new segment reporting, which emphasized the role of the Finnish business (the former Asiakastieto) in the company’s results.

Are there any Enento followers here? What do you think about the change negotiations (YT-neuvottelut) announced before the Q1 results? Are you getting Terveystalo vibes from this? Are the results going to be much worse than expected?