So, do you still have faith in Enersense and the achievement of their growth targets, or have you already “given up”?

7 Likes

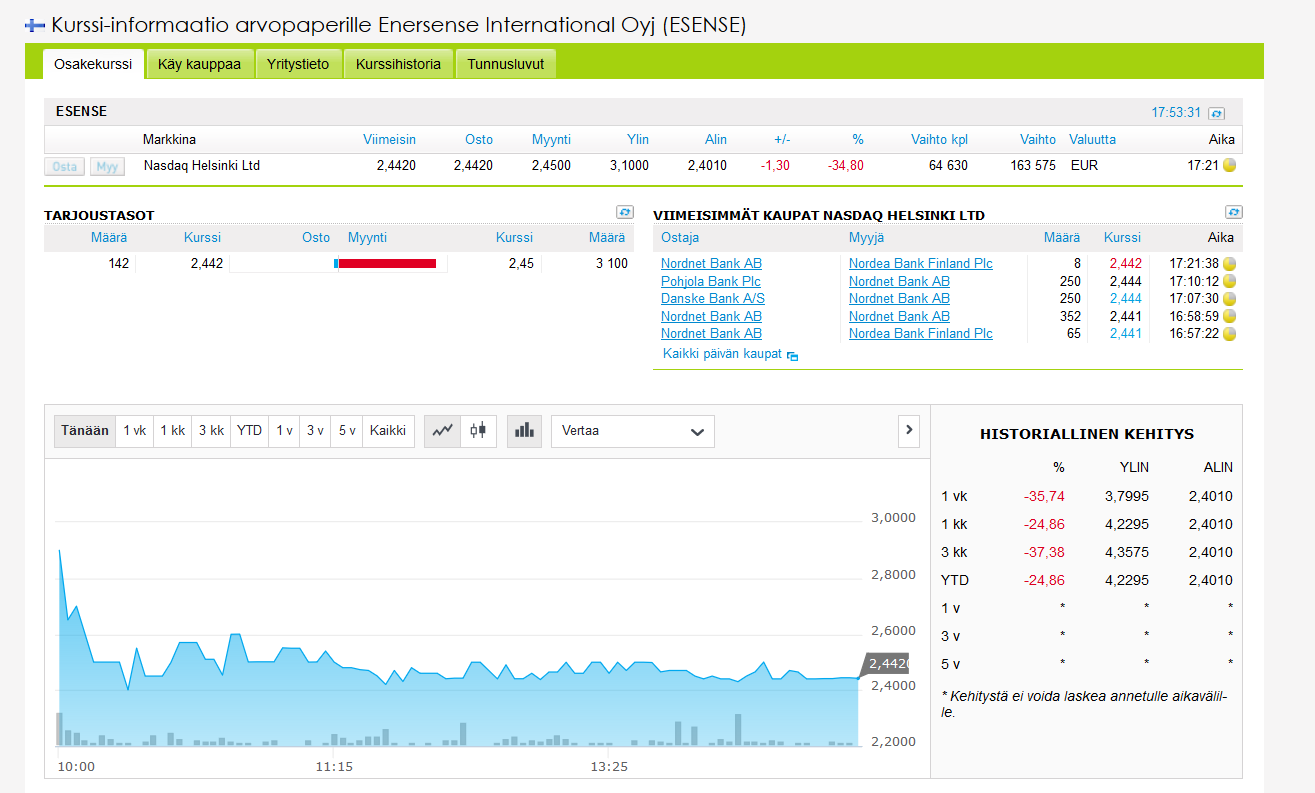

There’s still growth here, in good shape. Making a profit will just come later, meaning it requires patience. I’ve been thinking about buying now that there was a drop after the results.

2 Likes

However, the growth fell considerably short of forecasts. Why would this company generate profit in the future when its largest source of income will soon be lost? Growth was the foundation for the future, and it failed. This is still shockingly expensive. Growth in no way compensates for projects nearing completion.

2 Likes

As I understand it, the company just needs to get its latest acquisition target in order, as it did with previous acquisitions. (Proof that the company has the ability to turn acquired companies around.) After that, everything would be okay. You probably mean Olkiluoto with that largest source of income. Enersense said they could compensate for it well with other ramped-up projects, and Olkiluoto will probably never completely end, so resources will always be needed there. I haven’t looked into it more closely, I need to read more, or if someone can explain how the end of Olkiluoto will be compensated for in the future, please let me know. Thanks for challenging me a bit, it helps me decide whether to buy according to the recommendation or leave it behind. And I agree with you about the analyst’s ownership. Does Inderes’ analyst own Enersense? @Petri_Gostowski

1 Like

Around the time we started tracking this, there was talk that Enersense had the opportunity to secure contracts for three different nuclear power projects, and if I recall correctly, Sauli mentioned in a presentation that it was likely one of these would materialize. So, the future largely hinged on the belief that at least one of these would yield a significant project, and growth would otherwise be good. Personally, I wouldn’t bet too much on any of those materializing significantly enough to even come close to replacing Olkiluoto. The workforce at Olkiluoto will drop to a fraction. Even if it doesn’t completely end, the revenue will decrease to a fraction.

1 Like

You’re very much on the right track with your comment. However, I’d like to add that the revenue brought in by Olkiluoto is intended to be offset by other nuclear power projects. Of these, Flamanville seems to me to be the most likely at the moment, to which the company has already transferred a small number of personnel. You were also right that even after the construction phase, the company will have personnel remaining at Olkiluoto for maintenance and servicing, so its revenue contribution will not drop to zero.

Personally, I own Enersense, having bought it in the summer before the H1 report.

5 Likes

Reportedly, Enersense is courting Raos Project concerning the upcoming nuclear power plant in Pyhäjoki. It remains to be seen whether this Finnish subsidiary with Russian roots will take any kind of deal…

2 Likes

Enersense Expands to France and Germany https://www.inderes.fi/fi/tiedotteet/enersense-perustaa-tytaryhtiot-ranskaan-ja-saksaan

"CEO Jussi Holopainen comments:

“We have been actively exploring the French and German markets. The project outlook in these markets is such that we decided to establish our own subsidiaries in these countries. Up until now, we have operated in these regions from Finland.”"

1 Like

What do you think about Enersense’s acquisition of Värväämö? My feeling is that the Värväämö deal is an acquisition of a cyclical (construction industry staffing) business at the peak of the cycle..

2 Likes

Upside is starting to be 65% to the index target price… Hmmm?

![]()

3 Likes

0.4 EV/sales is not terribly expensive, it’s true. But I still want to keep an eye on it to see if, with a cyclical turnaround, I could get EV/sales down to something like 0.25 or less, given it’s such a small and overlooked company. This has the potential to be genuinely cheap.

1 Like

Hey! I listened to your podcast 34 (Personnel Services Companies and Market). It was really enjoyable to listen to, thanks to Petri and Juha.

From the discussion, I got the impression that the personnel services industry is a difficult business with small margins, fierce competition, and where companies don’t have a significant competitive advantage (no moat!). In practice, it’s hard to differentiate yourself in any meaningful way (except perhaps with technology, maybe, one day..). On top of that, the industry is quite cyclical, as flexibility is what attracts companies.

This then raises the question, why is Inderes so bullish on Enersense? The industry doesn’t seem attractive at all, at least that’s the feeling I got after the podcast. Enersense also practically has only a few customers on which its revenue depends, and it might be very difficult to find a replacement for the Olkiluoto project. AND if a recession is now coming, couldn’t things get quite grim for the company? ![]()

Greetings from Belgium, come for a beer sometime!

2 Likes

Damn, I was just there a month ago for a bit of ![]() on a Qt-Berlin trip.

on a Qt-Berlin trip.

As for Enersense itself, analyst @Petri_Gostowski would best answer that.

1 Like

After reading the profit warning, there shouldn’t be any long-term problems.

According to the warning, the problems are limited to the end of the year and the situation should normalize in 2019.

The other question is whether the message of the warning can be trusted. It is probably justified to be cautious.

If the message later proves to be true, the current price would be a clear buying opportunity.

If the warning’s message has been smoothed over, and thus does not align with future developments, no one knows its true price.

However, I bought an exploratory batch for under 2.5 euros.

If the numbers recover over the year according to the warning’s message, the purchase was good; if they don’t, I am ready to take the hit I set up for myself.

It is clear that the management’s ability to take corrective actions will be measured in 2019.

2 Likes

Enersense has now been hit hard. Clearly, the market reacted quite quickly to @Petri_Gostowski’s forecast change. “Sell” now apparently literally meant “dump all shares and run far away!”

4 Likes

Akilta, as usual, an entertaining and good column today, on the topic of Enersense’s IPO:

A lot of good points and healthy self-criticism.

Regarding Enersense itself, considering the points raised in Aki’s column, following such a company is not necessarily the best PR for Inderes either.

I’d like to see the CEO in the next Roast, but I doubt they’ll dare to show up.

Luckily, I didn’t subscribe to this one, not that I was even seriously considering it.

7 Likes

This might be the last thing I participate in with the thought that it’s probably an okay company when Inderes takes on an IPO and gives a buy recommendation.

It probably belongs in the failures thread, but what on earth have I done, putting money into staffing and furniture??? When there’s all sorts of scalable and digital wonders available :).

The only consolation is the small size of the position, and the possibility of loss continuously decreases as the pot also shrinks…

6 Likes

Enersense just keeps disappointing, time and again…

Today, Enersense released three positive press releases!

It certainly feels like there are some tasty treats for a proper January rally!

2 Likes

Yep, in with a small position. I understand that when I spun the taxes and added a bit more to the portfolio, it was as cheap as a Sausage… I thought that any positive news might lift it out of the tax-loss selling rut.

1 Like