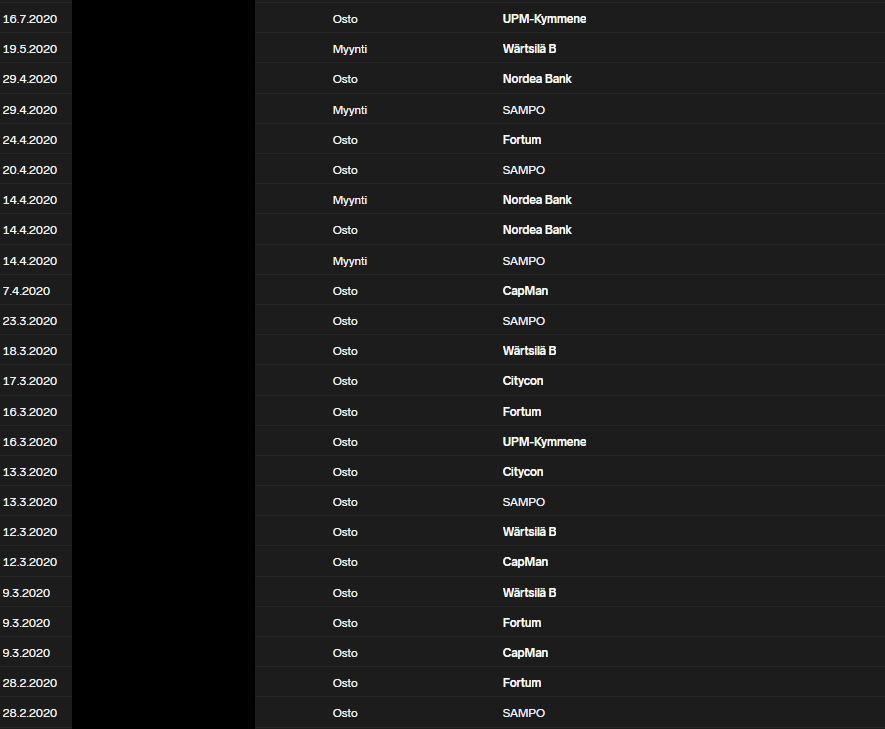

Out of curiosity, I checked what the corona spring of 2020 looked like in terms of trades. From memory, I’d say that the Equity Savings Account (OST) was launched at the turn of 2020, so there are also, for example, Nordea’s transfers from a Securities Account (AOT) to an OST. If I recall correctly, Nordnet also had some opening offer that allowed for relatively cheap purchases, so at least compared to today, quite small sums per purchase order were made. However, my investment assets were also about a fifth of what they are now back then.

I was lucky in that I had prepared for the introduction of the Equity Savings Account by not buying anything, and I had even sold shares from my AOT in 2019 when they seemed expensive, so I was largely in cash.

It was bought with a taste of vomit in my mouth, and if I remember correctly, my own buying steps were at intervals of about 5-10%, meaning in March, you could practically buy everything once or twice a week. Looking back, I could have bought more and bigger, but the mood was quite grim, and during lockdown, there wasn’t much to distract my thoughts. Going for a run helped clear my head a bit, but otherwise, it was quite lonely, even for an introvert. Fortunately, I know many investors, and there were forums even then, so there were plenty of fellow sufferers to laugh and lament with about the situation. Without that, it might have been somewhat tougher to watch my wealth melt away alone. Of course, I was a student investor at the time, so investment literature had been hammered into my head recently, and all of it taught that crises are precisely the moments when one should buy. There, the inexperienced “hoyhoy” reminded himself that one must buy when there’s blood in the streets and pressed the buttons, even though some of the blood felt like his own. In the end, I even slept quite well at night. Five years later, however, I must say that my own discomfort has probably been somewhat forgotten, as looking at the price charts makes it easy to say that of course it was worth buying. At that time, however, the atmosphere was a bit different, as newspapers were calculating the endurance of intensive care unit capacity and drawing casualty curves that grew exponentially.

During the downturn, I acted correctly in relation to my own financial situation. I bought quite stable companies, of which, for example, Sampo seemed to primarily benefit from the pandemic. The mistakes came when I started reducing my weighting too early, even though the stocks were still absolutely quite cheap. Even there, a couple of Sampo reductions are visible in April. Of course, I was ultimately a net buyer long after that, but I should have bought even more boldly into the rising market. Fortunately, in the autumn of 2022, I was able to buy quite cheaply again, which allowed me to somewhat patch up my diminished stock weighting. Additionally, I messed up with my interest rate view, although that inflation after such helicopter money probably didn’t surprise me, and I certainly didn’t understand how strongly interest rates affect, for example, Citycon.