Did @Olli_Vilppo have those ERP costs included in the operating profit? If so, then the profitability fell slightly short of what was expected.

Yes, those EUR 0.2 million were indeed adjustments, as they were included in the forecast for operational EBIT, which is why EBIT fell slightly short of expectations. But overall, it was an expected report based on the results and outlook.

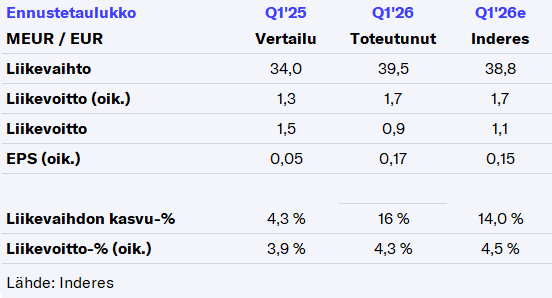

The webcast starts at 11:00 Boreo, Webcast, Q1'26 - Inderes and we’ll listen to see if any new information comes out.

3 Likes

Olli interviewed Tuomas Kahri:

No drama here today, and perhaps that’s for the best. We should see more of the promised growth in H2. The increased activity on the M&A front is positive, also signaling confidence in the current businesses’ cash-generating ability and consequently the balance sheet position.

13 Likes

Boreo (Q1 Interview): Business off to a good start under new CEO.

Redeye interviews Boreo’s new CEO, Tuomas Kahri. We discuss Tuomas’ extensive background and the company’s strong Q1 2026 report.

Report here! There were indeed no surprises, so we continued with almost the same forecasts and the same view.

10 Likes

Critical comments on Inderes’ analysis report are as follows:

- Today’s analysis from Inderes completely overlooks the €19 million in liquidity + cash highlighted in Boreo’s Q1 report, which provides the opportunity mentioned in the release to continue selected add-on acquisitions, as stated yesterday in the earnings release as well as in both the Inderes and Redeye interviews.

- The statement at the end of the report that “the ability to make acquisitions is currently limited” is pessimistic and backward-looking; it fails to account for the strong liquidity position described by the company in yesterday’s earnings release and the Inderes and Redeye interviews.

These are very unfortunate shortcomings, and for these reasons, Inderes’ narrative is incomplete and backward-looking. Investor returns, however, depend on future performance. Personally, I have more faith in the narrative of Boreo’s Head of M&A; below are copies of the relevant Q&A transcript sections:

Q: How do you view the financial stability, especially with hybrid debt not classified as debt in your reporting? A: Rafael Kosmonov, Head of M&A and Financing: We have a good cash flow and expect to decrease leverage this year. Our liquidity position is strong, and we have full support from financial partners.

Q: You talk about both accelerating M&A activities and strengthening the balance sheet. Can you describe that dynamic? A: Rafael Kosmonov, Head of M&A and Financing: We are paying down debt and exploring financing alternatives. We aim to make small add-on acquisitions now and larger ones as our balance sheet strengthens. We are building a pipeline of potential targets to be selective.

1 Like

The ability to make acquisitions will certainly recover once the earnings improvement comes through, but they are not currently being front-run in the valuation. That is why it’s stated so clearly on the front page as well: the current valuation is based on existing operations.

There are still unused debt facilities, of course, but we don’t believe any major acquisitions will be seen now, given the net debt of €29.5M and hybrids of €30M. The focus is on deleveraging, which according to our calculations is now decreasing by about €4M/year if nothing is bought—which is quite a decent rate.

In 2027, a €20M hybrid, among other things, needs to be refinanced, so it’s better to approach that point with a strong balance sheet.

But indeed, once again, the sentiment following Q1 remained positive.

11 Likes

Apparently, a board member felt the same way. Reaching into the pocket and a bunch of shares from the market![]() :

:

7 Likes

- Mattias Björk is a very cool guy on Boreo’s board, and he brings a lot of serial acquirer and stock market expertise to the board (=e.g., Volati, Bokusgruppen). I also like that he is active with Boreo share acquisitions. I agree with the Redeye analysts that it is good for board members to have significant share ownership.

- Boreo’s Q1 performance is really interesting when looking at the growth figures of Swedish peers from the same period and the data on the Finnish economy published by Statistics Finland during May Day week.

Momentum Group Q1/2026 (29.4.2026):

• Revenue was in line with previous year. Sales for comparable units decreased by 6%.

Indutrade Q1/2026 (24.4.2026):

• Order intake increased by 2%. For comparable units, the increase was 1%.

• Net sales were unchanged . For comparable units, there was no change.

Boreo Q1/2026 (29.4.2026):

Net sales increased by 16%. Organic growth was 9%.

In addition, Statistics Finland published data on the Finnish national economy in the first quarter during May Day week, with the following highlights:

-

Finland’s gross domestic product is estimated to have grown by 0.9% in the first quarter of 2026.

-

Trade turnover increased by 4.9% in March 2026, and Services turnover increased by 5.4% in March 2026.

Good figures for both Boreo and the Finnish economy, and significant in that I don’t immediately recall when Boreo’s quarterly growth figures have been better than its Swedish peers. -At the same time, the Finnish economy, which has lagged since the start of the war in Ukraine, seems to have gained real momentum in early 2026, and the trade and service figures for March are solid. In fact, we are usually only accustomed to seeing 5% growth figures like that in the US economy.

Edit 4.5.2026:

Arvopaperi notes Boreo as a turnaround company in today’s article “Three potential turnaround cases from the Helsinki Stock Exchange: You can still get on board at a reasonable price”:

“We picked companies from the Helsinki Stock Exchange that show emerging signs of a profitability turnaround, but the turnaround is not yet reflected in the valuation. F-Secure, Fondia, and Boreo caught the net. “

6 Likes

More skin in the game. The fresh CEO increased his shareholding:

With this move, he rose to become the sixth-largest shareholder.

11 Likes

Block trade in Boreo:

![]()

I consider it likely that the seller is this party, i.e., the former owner of Pronius:

![]()

He already reduced his position somewhat earlier this year.

Could the buyer perhaps even be found among the management?

1 Like