I would consider it likely, based on the timing, that the change of CFO is related to the change of the company’s CEO and the expectations possibly associated with it within the company. -No changes have been announced in the strategy, so it can’t really be related to anything else. People are ambitious regarding internal appointments, and if their own expectations and the company’s needs don’t align, then changes occur. Normal.

1 Like

Industrial turnover indicators are now developing positively month after month. Although the entire industry is a broad entity, I have thought that this also describes the business cycle of Boreo’s companies (Pronius, J-matic, Filtteri, Machinery MT, Milcon, etc.) to some extent. Construction is then its own kettle of fish, but even there, things are hardly going down anymore.

9 Likes

Now also positive figures from the construction sector.

https://forum.inderes.com/t/porssien-suunta-osa-3/42502/5761?u=karhu_hylje

The business cycle situation is rapidly improving in Boreo’s operations. It’s a shame that the change in management now adds a bit of uncertainty.

Boreo, by the way, has now discontinued SEB’s coverage. The reason is probably that they previously took on Redeye’s coverage as new.

5 Likes

Here’s an example for many others too, if one believes in the company, let’s take a slightly more generous view:

13 Likes

Boreo’s updated comprehensive report is available to read here.

19 Likes

In December, the momentum only strengthened as industry grew by 4.1% compared to last year and construction by a whopping 11.8%. Management comments last time (Q3) stated that industrial demand had already improved, but demand on the construction side remained sluggish. Now, perhaps a clearer change for the better has been achieved in that field as well for Q4. The starting point for this year is indeed interesting, especially since the major investment phase in Delfin should also be starting to wrap up.

8 Likes

Boreo needs to centralize its administrative functions more into a group-wide model to achieve greater synergies and savings and to enable more profitable growth. Hopefully, the new Group CEO will implement this, unless the main owner exerts too much control.

Boreo’s current decentralized operating model is the complete opposite of a centralized model. Yes, some efficiency gains are certainly lost on the bottom line in a decentralized setup, but this model ensures the preservation of each acquired company’s own culture and thus reduces risk in acquisitions. In my opinion, the cultural aspect is important when attracting more companies under Boreo’s umbrella. A new company can continue with its own model as long as it meets the financial metrics set by the parent company. The parent company, for its part, wants to focus as much as possible on capital allocation rather than running these companies.

If Boreo were to suddenly change the model to a more centralized one, it would be a confusing move for me, and that last bit of being a serial acquirer would be lost.

2 Likes

Great points! The cultural aspect is definitely an essential part of every company’s identity.

To clarify my previous point, these administrative centralizations are not intended to direct business operations or, especially, company culture, but rather to support and enable them. At their best, these measures bring resource efficiency and support, allowing employees to focus more on their core tasks. Small and medium-sized enterprises (SMEs) rarely have deep expertise in all areas of business, such as ICT-related matters, the importance of which is constantly increasing in efficient operations. SMEs often spend a lot of time and resources on these things, and that is where savings and efficiency gains are frequently found. This is just one example.

Of course, it is good to remember that these actions also require capability and discretion to ensure the core philosophy remains intact.

2 Likes

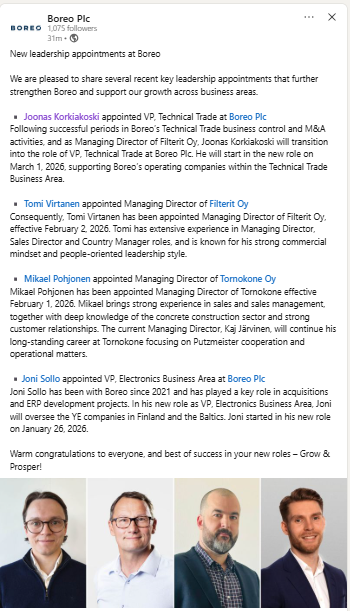

Leadership changes at Boreo. Although the group’s top brass are changing now, fortunately, there are more familiar names at the lower level, and the business area heads are staying the same. Former Inderes analyst Joonas Korkiakoski is advancing in his career at Boreo ![]()

18 Likes

The weekend before next Friday’s interim report, and my own subjective thoughts below.

- According to the latest reported quarter:

- revenue €146m (R12)

- €7.3m operational EBIT

- 23 companies

- In the rearview mirror, strong growth and a market rollercoaster

- 2019-2022, rapid growth phase

- 2023-2024, challenges (Ukraine, Finnish economy)

- 2025, back to growth

- After the market dip, four consecutive quarters of growth are already behind us

4. The business model has proven its functionality both in the general market (=Boreo’s peer companies in Sweden) and under Preato’s ownership (=Consivo)

- In next week’s financial statements, the following are of interest:

-continuation of organic growth

-growth opportunities for Milcon, Delfin, Signal Solutions, and Filterit

-performance and outlook of the RS businesses acquired in 2025

- On the strategic side, hopefully we will hear something in the financial statements or the review about the status/continuation of the previously announced 2026 portfolio review.

Boreo has implemented its strategy quite exemplarily over the long term; below are the strategic targets compared to the 5-year average 2020-2024:

-EBIT growth/year: target 15%, realized 26%

-ROCE: target 15%, realized 10%

-net debt: target 2-3x, realized 2.5x net debt/EBITDA

And since that is the case, it would be worth considering measuring these parameters over a longer period than annually.

4 Likes

I share similar expectations with Justus above, especially regarding the portfolio review. It has already been two years since the updated strategy was released. Nothing concrete has happened in that regard other than the Machinery demerger (autumn 2024). As a shareholder, I am waiting for some moves to be made so that we can head toward the next steps.

Here are Olli’s preview comments as Boreo reports its Q4 results on Friday, Feb 13. ![]()

We expect the company’s revenue to have grown significantly from the comparison period, supported by acquisitions and improved organic demand. We also forecast the operating result to have strengthened alongside volume growth, although integration costs and development investments are hindering the full realization of operating leverage. Boreo does not typically provide short-term numerical guidance, so in the report, our attention will be focused particularly on the development of order books and comments on the market situation for 2026. No dividend is expected for investors as leverage remains high.

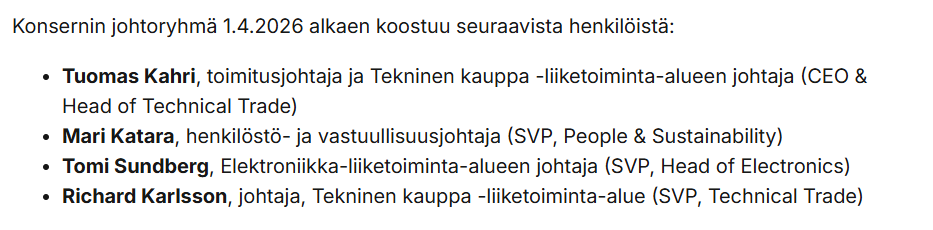

Why is Kahri also responsible for technical trade if the business area still has its own director, Richard Karlsson? Or is Karlsson now only a director in some sub-area of technical trade?

“In addition to the duties of CEO, Kahri is responsible for the Technical Trade business area.”

2 Likes

Yesterday, an update was also released regarding the continuation of the company’s CFO role. For the time being, the role will be split into two parts: M&A / Financing and financial reporting. Rafael Osmanov, who apparently leads a private equity firm called Helix Partners, has been appointed as M&A Director. Rafael has over 15 years of experience in M&A etc. Sami Hanerva was found from within Boreo for the reporting side.

From an investor’s perspective, this looks a bit messy at the moment, but I think the new CEO wants to have a say in the selection of the new CFO in the future. This is perhaps why the change was announced as a temporary solution.

5 Likes

Information about Boreo’s Delfin has been relatively scarce, so I did a little analysis using AI for my own amusement. The AI dug up some quite interesting points, especially regarding market position, the technical competitive landscape, and competitiveness. Below is a summary:

Delfin Technologies has high growth potential as a key player in the specialized skin measurement instruments market. The company is positioned at the intersection of several rapidly expanding sectors:

Competitiveness:

-

Core Competitiveness: Delfin is recognized as a significant market share holder alongside industry leaders like Cortex Technology and Courage + Khazaka.

-

Scientific Validation: Their devices are used in peer-reviewed research, making them essential for claims substantiation in the cosmetics R&D sector.

-

Global Reach: With a presence in over 40–60 countries and a strong focus on North America, Europe, and Asia, Delfin is well-integrated into the most lucrative regional markets.

Delfin’s product portfolio aligns with the fastest-growing niches in dermatology and aesthetics.

Market Share:

Delfin Technologies is a significant player in the specialized skin measurement instruments market, which is characterized by a high concentration of established European and North American companies.

- Market Share: As of 2025, Delfin Technologies holds an estimated 11.5% of the global skin measurement instruments market.

Technical Specification Comparisons

Delfin’s competitive advantage lies in its closed-chamber technology and portability, whereas competitors often prioritize high-precision open-chamber systems or integrated laboratory workstations.

1. TEWL (Transepidermal Water Loss) Measurement

Comparing the Delfin VapoMeter against the Courage + Khazaka Tewameter:

-

Measurement Principle: Delfin uses a closed-chamber method, which is less sensitive to ambient air currents and allows for measurements in any orientation (e.g., vertical or upside down). The Tewameter uses an open-chamber gradient method, which is the historical “gold standard” but requires a strictly controlled environment.

-

Sensitivity: Research indicates the Tewameter can detect smaller incremental differences in low water-loss levels, while the VapoMeter is faster and more consistent across varied environments.

2. Skin Hydration

Comparing the Delfin MoistureMeterSC against the Courage + Khazaka Corneometer:

-

Sensitivity: The MoistureMeterSC often shows a three times larger relative range of readings than the Corneometer, making it more sensitive to subtle differences in glycerin effects or individual variations.

-

Interference: Delfin’s capacitive principle is largely insensitive to salt and electrolytes in topical formulations, whereas the Corneometer may be more affected by salt concentration.

-

Depth: Delfin offers unique depth-specific probes (0.5 mm to 5.0 mm) through their MoistureMeterD line, allowing for measurements beyond the stratum corneum into the dermis and subcutis—a feature competitors rarely match in a handheld format.

3. Portability and Software

-

Form Factor: Delfin devices are typically fully wireless and handheld. Competitors like Cortex (DermaLab) often use a central PC-based “main unit” that probes plug into, though they have recently introduced more portable options.

-

Integration: Delfin’s DMC Software allows for modularity, where data from multiple different types of probes (hydration, TEWL, color) are synchronized into a single research database.

Global Skin Measurement Instruments Market Share (2026)

Cortex technology 26,10%

Canfield scientific 18,08%

Courage + Khazaka 16,40%

Delfin technologies 11,50%

Biox systems 7,90%

Others 19,30

2 Likes

Oleee!!! Finally a proper beat on estimates and strong performance. Just celebrating the result for now, more detailed comments later. Great job Kari and the rest!

With a report like this, it’s a pleasure to pass the baton @Rosskopf. Good luck going forward!

15 Likes

Yes, a truly breathtaking turnaround report.

Boreo Plc, FINANCIAL STATEMENT RELEASE 1 Jan – 31 Dec 2025

13 Feb 2026 at 9:00 AM

A strong finish to the year

October–December 2025

-

Net sales increased by 18% to EUR 46.3 million (2024: 39.2). Organic growth was 12%.

-

Operational EBIT increased by 33% to EUR 2.8 million (2024: 2.1) and was 6.0% of net sales (2024: 5.3%).

-

Operating profit (EBIT) increased to EUR 2.1 million (2024: 1.7).

-

Net cash flow from operating activities was EUR 5.6 million (2024: 7.1).

-

Earnings per share (EPS) increased and was EUR 0.35 (2024: 0.13).

January–December 2025

-

Net sales increased by 14% to EUR 153.3 million (2024: 134.0). Organic growth was 11%.

-

Operational EBIT increased by 17% to EUR 8.0 million (2024: 6.8) and was 5.2% of net sales (2024: 5.1%).

-

Operating profit (EBIT) rose to EUR 6.7 million (2024: 4.1).

-

Net cash flow from operating activities was EUR 7.5 million (2024: 12.0).

-

Earnings per share (EPS) rose significantly and was EUR 0.72 (2024: -0.30).

Order books continued to strengthen

The order books of our companies strengthened from the previous quarter and are clearly higher than the level at the beginning of 2025. Although the economic cycle, especially in Finland and the Baltic countries, is expected to remain modest in 2026, the prerequisites for earnings improvement are good.

Due to the order book’s higher-than-normal weighting toward the end of 2026, as well as system projects weighted toward the beginning of the year, we expect the company’s performance to improve toward the end of the year.

PS: Inderes was completely off with their forecasting, again. It is quite unfortunate if the analysis just follows the general sentiment in Finland, and the company-specific turnaround is missed even though there were already 4 quarters of growth before this and all economic forecasts from banks and forecasting institutes had already turned.

3 Likes

Well, we weren’t completely off the mark ![]()

Strong growth was predicted, as was growth in operating profit, and the target price was quite a bit higher than the share price! The company’s technical trade exceeded sales expectations, which then translated into the result with good leverage! This is certainly worth analyzing now.

| Forecast table | Q4’24 | Q4’25 | Q4’25e | Q4’25e | Consensus | Difference (%) | |||

|---|---|---|---|---|---|---|---|---|---|

| MEUR / EUR | Comparison | Actual | Inderes | Consensus | Lowest | Highest | Act. vs. Inderes | ||

| Revenue | 39.2 | 46.3 | 43.2 | 7 % | |||||

| Operating profit (adj.) | 2.1 | 2.8 | 2.3 | 23 % | |||||

| Operating profit | 1.7 | 2.1 | 1.6 | 33 % | |||||

| EPS (adj.) | 0.25 | 0.35 | 0.26 | 36 % | |||||

| Dividend/share | 0.00 | 0.00 | 0.00 | ||||||

| Revenue growth % | 5.7 % | 18.1 % | 10.1 % | 8 %-points | |||||

| Operating profit % (adj.) | 5.3 % | 6.0 % | 5.3 % | 0.8 %-points | |||||

| Source: Inderes |

18 Likes

What a pleasant surprise. The changes in key personnel caused some uncertainty for me, but fortunately, it was for nothing. It’s also good that no dividend is being paid; now it’s time to strengthen the balance sheet and execute the strategy. The core concept of this company is solid. The most pleasant surprise of the earnings season so far.

8 Likes