Petri has diligently completed Boreo’s company report this Sunday evening.

The share’s risk level is clearly elevated in the short term, backed by high indebtedness and a subdued earnings outlook due to a weak operating environment. On the flip side, there is a demand outlook that will eventually pick up, leading to a higher earnings level, relative to which the share is priced quite moderately. We believe the company will weather this period of elevated risk, which is why we rely on the long-term high return potential in our view. Thus, we raise our recommendation to ‘add’ (previously ‘reduce’), but reflecting forecast changes and an increased required rate of return, we lower our target price to 11.5 euros (previously 15.0 euros).

Quoted from the report:

We have raised the required rate of return in our cash flow model due to risks related to the financial position. Despite the elevated required rate of return, our cash flow model yields 11.6 euros/share, indicating that the share is also moderately priced according to our cash flow model. Our medium and long-term forecasts anticipate revenue growth roughly in line with economic growth, and profitability forecasts expect an improvement compared to recent historical performance (previous 12-month operating EBIT-% 5.2% vs. 2028-2033e 6.0%).

It is also important to pay attention to the debt repayment of these highly leveraged companies; the fact that there is a lot of debt and also interest expenses means those debts also need to be amortized.

In Boreo’s case, this year, approximately 7.9 million euros in amortizations and lease liabilities are due, in addition to which there will be approximately 4 million euros in interest expenses.

It is probably clear that the company cannot manage these with cash flow alone, but some kind of loan arrangement is likely coming.

After the upcoming interim report/financial statements, we will be a little wiser again.

If I’m researching correctly, this is exactly the property that YE Int. owns/owned. Perhaps there is more information about this in the financial statements.

Here are Pete’s pre-earnings comments as Boreo publishes its Q4 results on Thursday.

We estimate that weak demand has weighed on revenue, leading to a clear decline, and reflecting this, earnings also clearly declined from the comparison period in Q4. Due to its tight financial position, we do not expect the company to pay a dividend for the 2024 financial year. In line with its guidance policy, the company has not typically provided guidance, and we do not expect it to do so now either.

Revenue 24 million, operating profit (adj) approx 1 million

It’s interesting to see how much cash there is and if there are any debt arrangements, e.g., regarding the payment of that Hybrid.

In my opinion, the company should provide some guidance for the upcoming quarter and regarding its financial position.

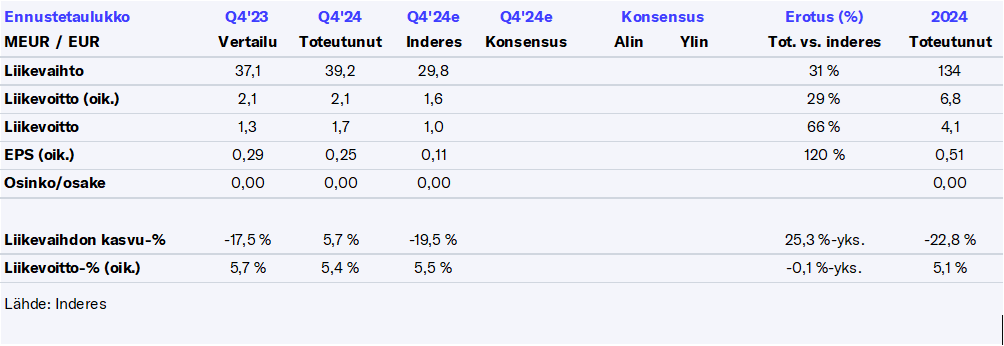

Q4/2024 will be remembered by Boreo’s investors as a turning point for the better, a very important turnaround:

October-December 2024

Revenue grew by 6% to EUR 39.2 million (2023: 37.1).

Operating profit of EUR 2.1 million was at the comparison period’s level (2023: 2.1) and was 5.3% of revenue (2023: 5.6%).

Operating profit increased to EUR 1.7 million (2023: 1.2).

Profit for the review period improved to EUR 0.9 million (2023: EUR 0.3 million).

Net cash flow from operations increased significantly to EUR 7.1 million (2023: EUR 2.1 million), positively impacted by successful working capital reduction.

Operating earnings per share were EUR 0.25 (2023: 0.25).

Here are the figures in table format - the forecast error per hectare is far too large and downright embarrassing, but fortunately the direction of the forecast errors changed from the previous ones to be more favorable for all parties.

Sometimes you comment on Boreo through slightly too rose-tinted glasses, @Justus_Lipsius, but now you are right. The trend is turning, and with such a leveraged structure, when it turns, the earnings development should flow rapidly to the bottom line. Let’s hope that after the already commented weak Q1, we can achieve profitable growth. The financial situation also looks significantly better with these numbers. Strong cash flow in the last quarter!

The good thing about this is primarily the revenue growth; electronics, in particular, seems to be the driver now.

But on the other hand, debt payments were postponed until 2027; one would have thought there would have been enough resources even for the 2.5 million euro amortization payment.

In addition, the 5.7 million in working capital, specifically the reduction and sale of inventories in this case, increased cash and net cash flow because that avenue has been exhausted.

Equity attributable to the main owners, on the other hand, grew by 2 million euros, already exceeding 43 million.

The company now seems strongly focused on strengthening its financial position by selling inventories and otherwise streamlining operations before 2027, when significant amortizations and loan restructurings become due.

There’s no reason for applause yet, but if Q1 doesn’t go too badly, it might survive, though there are still no grounds for a share price increase.

How reassuring to hear that if Q1 doesn’t go too badly, our Boreo might not go bankrupt after all. However, based on your message history, you seem to approach the company very objectively, giving both criticism and praise equally, so at least I unswervingly trust your view that the stock price reaction seen now is an unjustified rise based on the results. Hopefully, we objective observers will eventually get some real reasons for the stock price to rise.

I haven’t believed in the threat of bankruptcy, because the main owner has too much at stake; perhaps a share issue, but even that seems difficult precisely because of the concentrated ownership.

The reason I initially started following the company a bit was this great term ‘Serial Acquirer’; I thought it was a great concept: companies are bought cheaply, and their earnings then pay off the purchase price.

Well, now it has been noticed that it doesn’t really work; debt has just steadily increased.

My guess is that no new acquisitions will be seen this year at least, or they will be in the category of less than a million or so.

It strongly appears that the company is focusing on debt repayment in 2027; it’s another matter whether it succeeds or if due dates will have to be shifted again.

It is true that Boreo is now prioritizing its balance sheet position and financing situation, but the intention is not to run the company debt-free in the future. Rather, we are talking about refinancing on the best possible terms (i.e., precisely postponing the due date, like other companies). This requires improving profitability and probably some reduction in the debt level.

Leverage is perfectly fine if one’s shoulders are broad enough, but apparently even the board is not sure about future earnings performance, as even the 2.5 million repayments were postponed. At least the old hybrid debt of 4 million was paid off, though it also increased the debt owed to the main owner.

Interest must always be paid on debt.

I am skeptical about Boreo’s chances of getting refinancing on so-called good terms, cf. for example, the renewal of that Hybrid and the rise in interest rates.

In the next earnings report, I will pay attention, among other things, to the working capital situation, to see if there’s still enough inventory on the shelves or if that path has been exhausted.

Petri has written a company report on Boreo, which offered a pleasant surprise.

Boreo’s Q4 figures clearly exceeded our forecasts, as high revenue accumulation flowed into the result with profitability roughly in line with expectations. In our estimation, the Q4 figures partly reflected timing-related factors, although order books have generally increased compared to before. We have made positive forecast changes for the coming years, and in addition, a strong Q4 cash flow reinforced our expectations that the company will navigate through a tight financial situation unscathed. Reflecting these, we raise our target price to 12.5 euros (previously 11.50 euros), but in a 12-month horizon, aligning with a neutral valuation view, we lower our recommendation to reduce (previously add). Boreo’s CEO’s Q4 interview can be viewed from this link.

Quoted from the report:

Cash flow now rolled in the right direction

Business cash flow for 2024 reached EUR 12 million, and thus free cash flow (incl. lease payments and the impact of the hybrid), considering organic investments, settled at EUR 5.4 million. The free cash flow was supported by the company’s successful efforts to release working capital. Against this background, the company’s net debt was EUR 30 million (excluding EUR 24 million in hybrids) and corresponded to 2.8x the EBITDA of the previous 12 months. In the short term, the company estimates that its working capital will tie up a few million euros, and in addition, the repayment of the old hybrid, along with other debt repayments, is scheduled for the beginning of the year. However, the company’s liquidity situation allows for this, and thus, regarding its financial position, Q4 was somewhat reassuring.

Revenue Decline: Overall sales declined by 17% in 2024, primarily due to challenges in construction-related businesses and industrial exposure.

Operational EBIT: Achieved EUR6.8 million, representing 5.1% of sales.

Gross Margin Improvement: Increased from 28% to 30% in 2024.

Operational Cash Flow: Over EUR20 million generated in the last two years, with EUR7 million in Q4 2024.

Leverage Ratio: Ended 2024 at 2.8x net debt to operational EBIT.

Electronics Business Performance: Sales growth of 31% in Q4 2024, with an EBIT margin of 8.5%.

Technical Trade Performance: Sales declined by 11% in Q4 2024, with a 4.5% EBIT margin.

Liquidity: EUR24.5 million at year-end 2024, including EUR9.7 million in cash.

Order Book: Higher levels going into 2025 compared to the previous year.

Positive Points

Managed to secure and defend profitability through pricing actions and reducing fixed costs, achieving an operational EBIT of EUR6.8 million, which is 5.1% in relation to sales.

The company generated a strong operative cash flow of over EUR20 million in the last two years, with EUR7 million in the last quarter of 2024.

The electronics business area showed improved profitability, with a strong performance from SSN and Milken, contributing to a 31% sales growth in Q4 compared to the previous year.

Boreo Oyj successfully managed working capital, bringing it down to EUR25 million by the end of 2024, which supported strong operational cash flows.

The company extended its credit facilities by one year and postponed loan repayments, maintaining a liquidity of EUR24.5 million at the end of 2024.

Negative Points

Boreo Oyj experienced a 17% decline in sales throughout 2024, primarily due to challenges in construction-related businesses and industrial exposure.

The company’s financial standing is not where it wants to be, with leverage elevated at 2.8 times net debt to operational EBIT.

Technical trade business area faced a challenging operating environment, with an 11% sales decline in Q4 compared to the previous year.

The Putzmeister business in Finland continued to suffer from a tough market, with uncertain demand outlook going forward.

Despite improvements, the return on capital employed remains low at 8%, and leverage is higher than desired, indicating financial challenges.

Q & A Highlights

Q: Can you give some indication of the net impact from the cost cut actions and additional spending when thinking of 2025 compared to the end of 2024? A: Kari Nerg, CEO: We have made some recruitments and investments, particularly in Delphin Technologies and the machinery’s auxiliary power business. Going into 2025, we expect an increase in fixed costs due to inflation and provisions for improved performance. However, if market conditions do not support us as expected, we have the flexibility to adjust costs downward.

Q: Do you foresee the significantly better development of SSN continuing this year? What does their order book look like? A: Kari Nerg, CEO: The outlook for SSN is positive, especially in Poland and Finland, though more challenging in the US and Sweden. We expect SSN to operate at levels similar to 2022 and 2021, with gradual performance improvement throughout the year.

Q: What kind of working capital buildup do you expect in the near future? A: Kari Nerg, CEO: We anticipate a couple of million EUR in trade working capital swings, depending on sales activity and timing of larger deliveries. We aim to maintain a tight management of working capital, with some expected buildup at the start of the year.

Q: Can you provide an update on the timing of Putzmeister deliveries in Sweden? A: Kari Nerg, CEO: We expect the first deliveries to occur during Q1, with significant batches scheduled for Q2 and Q3. However, supply chain challenges, particularly with chassis, may affect the timing.

Q: How did the changes in debt repayment schedules affect your debt conditions? A: Jesse Petaja, CFO: The changes did not affect our current debt terms, and there are no material effects on costs. Any related costs are one-time impacts.

A nice price was obtained for that property, as it was indeed valued at €400k on the balance sheet. More room to maneuver on the balance sheet with the deal. Kari is smiling a bit more again. Of course, this also resulted in a corresponding increase in lease liabilities.