Those in the ecosystem buy a new one when the old one breaks, regardless of the fact that the new model is hardly different from the previous one, because those earlier models aren’t available anywhere.

This is unlikely to change at all in the coming years?

4 Likes

The tweet says something like this: Apple is a strong investment for several different reasons. The company has a globally recognized brand, high customer loyalty, and a solid financial position. Its operating margin is 25.3 percent and its profitability is otherwise in good shape, which signals efficiency and profitability.

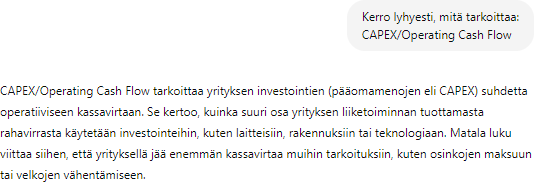

Over the past five years, Apple’s average revenue growth has been 5.4%, and earnings per share (EPS) has risen by 17.5% accordingly. The company is also investing heavily in the future; the CAPEX/Operating Cash Flow ratio is 9.9%, which according to the tweet, indicates a focus on long-term growth. Risk is limited by low leverage and a strong capital structure.

https://x.com/QCompounding/status/1834207843886477635

4 Likes

Ben Thompson’s good article on Apple

7 Likes

Here is a story about Rookie’s ancestor. ![]()

He originally owned 10 percent of Apple’s shares, but decided to sell them back to Steve Jobs and Steve Wozniak for a paltry 800 dollars. The reason for selling the shares at a rock-bottom price was that Wayne feared the company’s financial risk and wanted to avoid potential losses.

4 Likes

But what is the moral of the story? I see two holders and one trader there ![]()

7 Likes

iPhone 16 pre-order numbers have fallen 12.7 percent compared to last year’s iPhone 15 launch, based on delivery times and supply chain analysis.

7 Likes

It was such a minor update that I’m not surprised. Even the AI features are coming later, and to Europe even later.

Currently, the iPhone 15 Pro (which will also get the new AI features) is slightly cheaper at Verkkokauppa than the base 16 ![]() Those who can do without the AI gimmicks can already get the base 15 at a pretty good price.

Those who can do without the AI gimmicks can already get the base 15 at a pretty good price.

If purse strings are tightening, people don’t really want to make these upgrades.

1 Like

I read a similar story somewhere. The newest model brings less and less innovation year after year. Those who used to buy a new one every year are switching to a two-year upgrade cycle, and those who used to upgrade every two years are moving to three.

Device sales are declining, but apparently people aren’t switching from Apple’s ecosystem to Google’s in droves yet, as the service and software side is still going strong?

4 Likes

Switching has been made just the right amount of difficult ![]() The upgrade cycle will probably just get longer.

The upgrade cycle will probably just get longer.

Distinguishing between the Pro and base models is starting to become challenging when, for example, the screen refresh rate is kept lower than in the Pro. I wouldn’t be surprised if the display hardware was actually the same. You can already find those 120Hz screens in the sub-€500 price range. Better cameras, of course, etc.

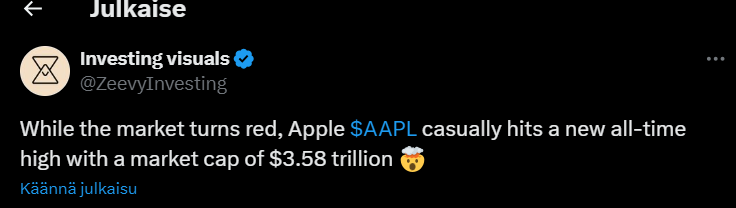

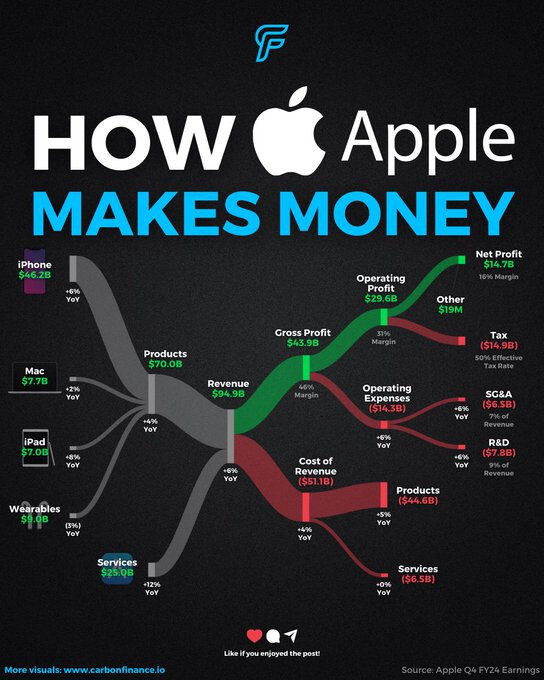

Here’s a quick look at Apple. ![]()

![]()

This company’s market cap is quite decent. ![]()

https://x.com/ZeevyInvesting/status/1846203128091213913

8 Likes

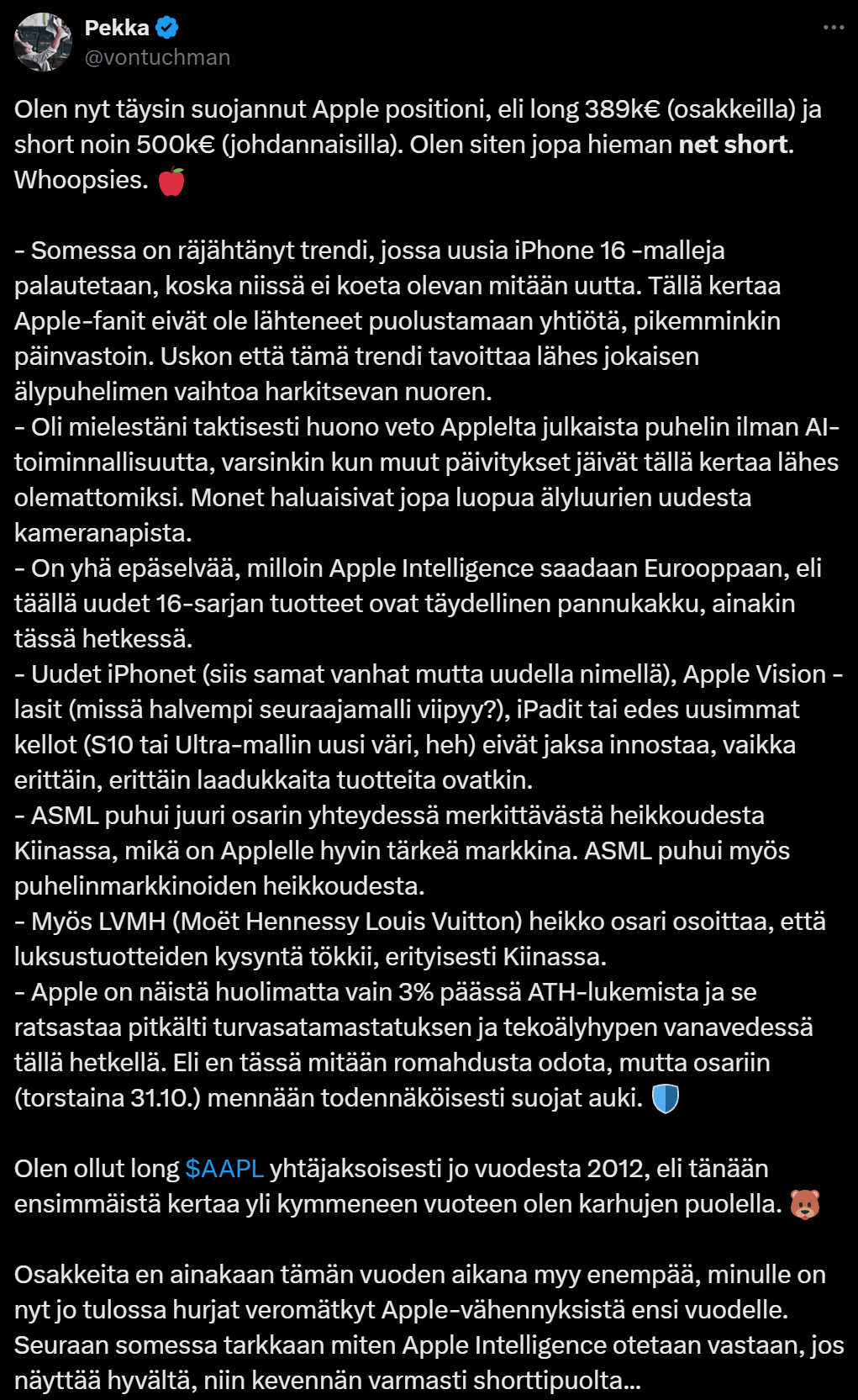

Pekka is bearish.

11 Likes

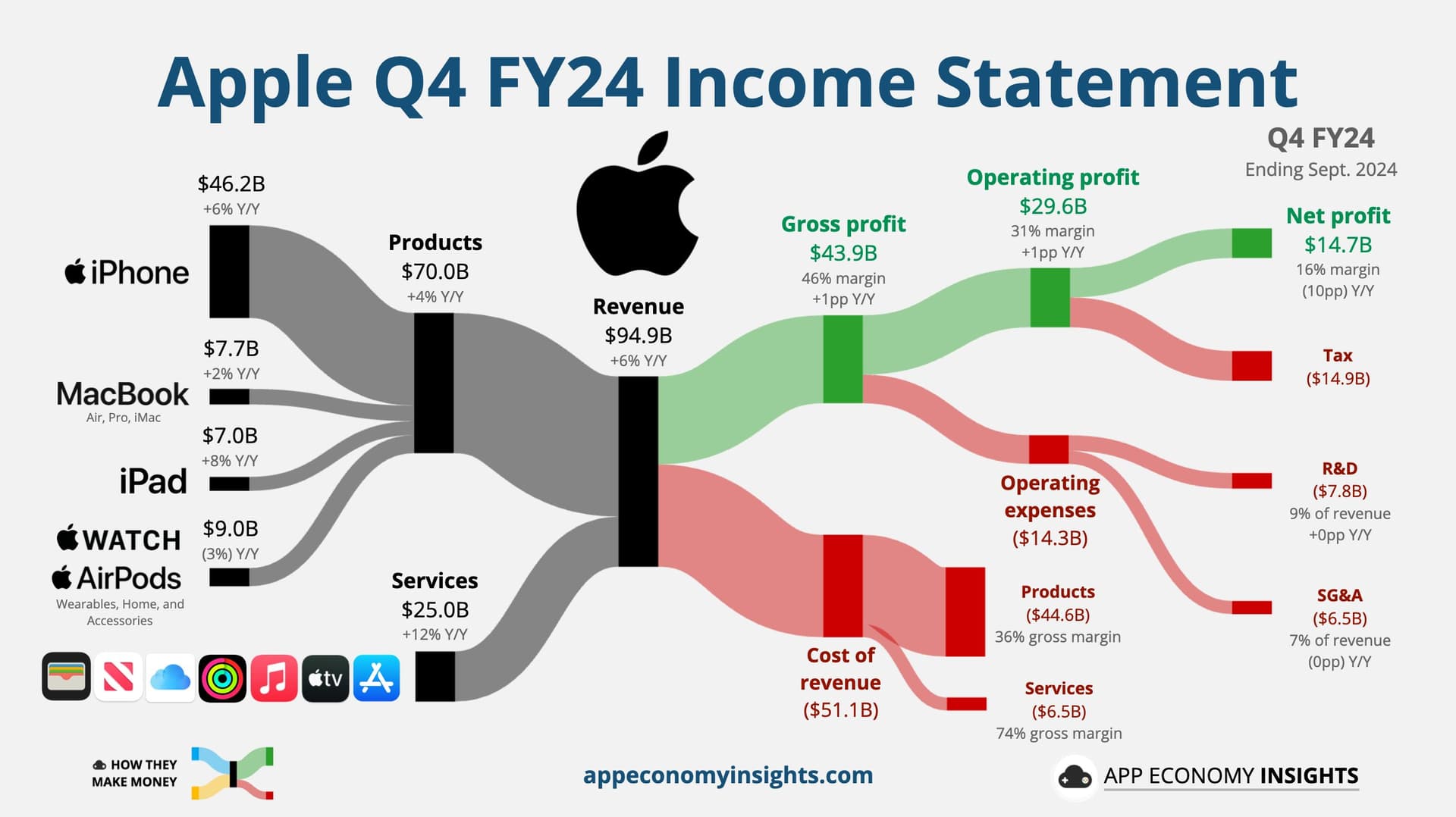

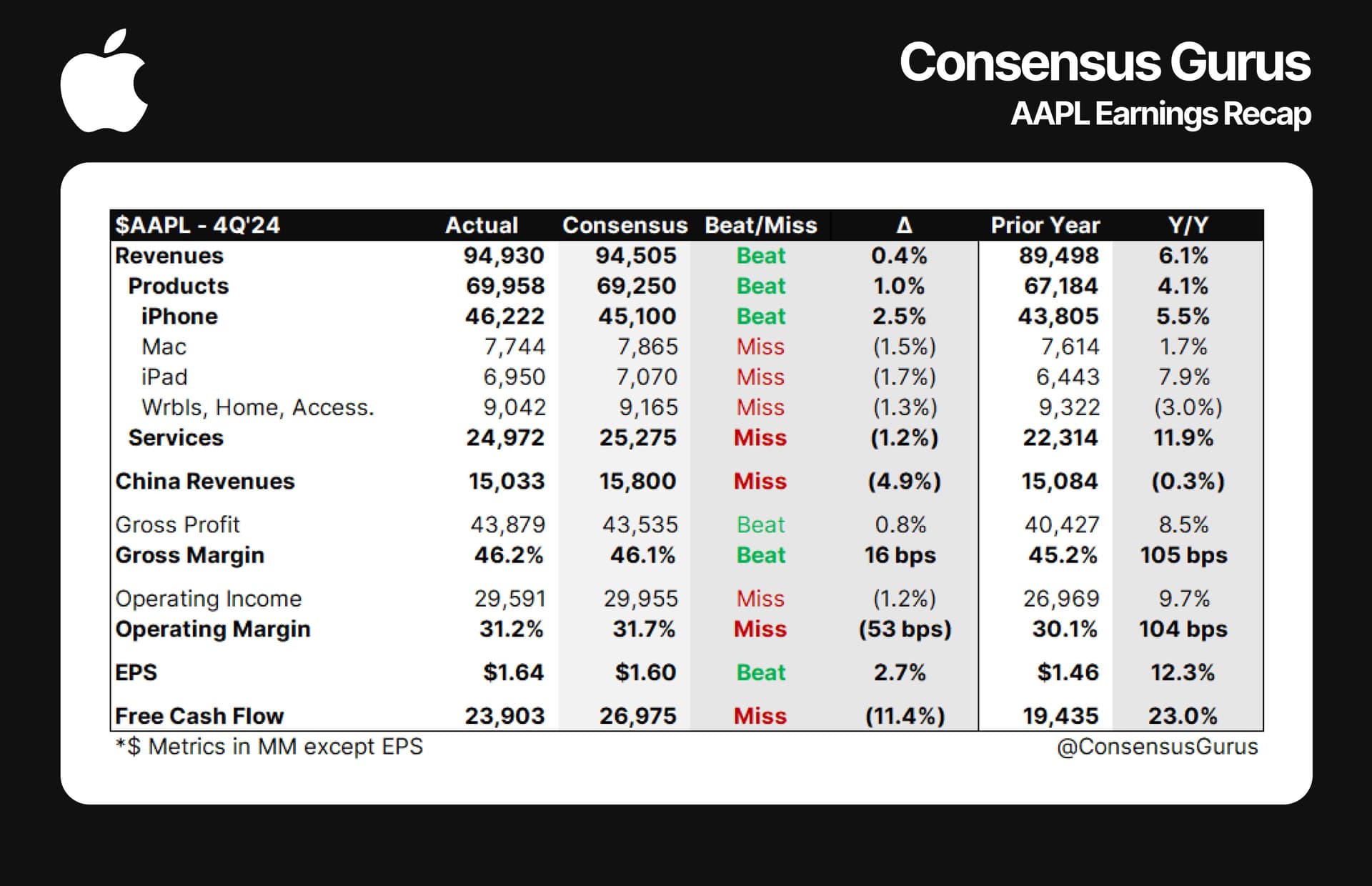

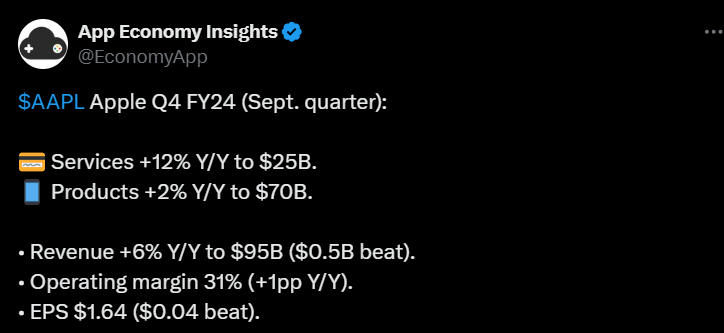

Apple’s fourth-quarter results exceeded expectations, although net income fell due to a European tax ruling. Revenue grew 6 percent to $94.93 billion.

The iPhone 16 sold well, and iPhone revenue grew 6 percent compared to the previous year. iPad sales also rose 8 percent, and growth for Mac products was 2 percent.

Apple also launched the Apple Intelligence AI system for iPhone and Mac devices, which boosted user upgrades. The Services business grew 12 percent, and the company expects moderate growth for the December quarter as well.

https://x.com/EconomyApp/status/1852089561138290744

https://x.com/ConsensusGurus/status/1852087214919778489

11 Likes

Apple and Q3 results; one more for good measure ![]()

https://x.com/ZeevyInvesting/status/1852366171506422067

https://x.com/ZeevyInvesting/status/1852366174417285342

EDIT:

https://x.com/EconomyApp/status/1852089561138290744

7 Likes

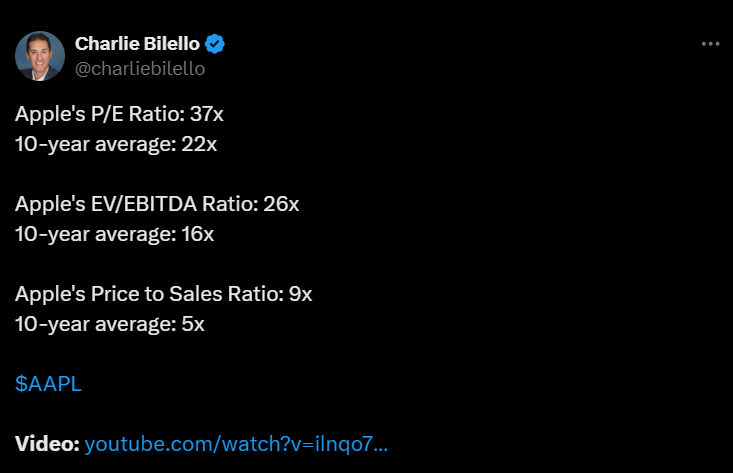

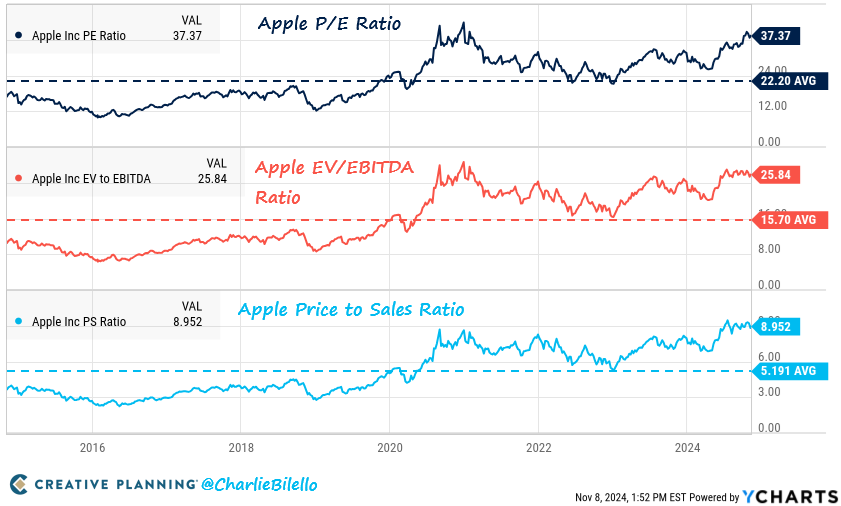

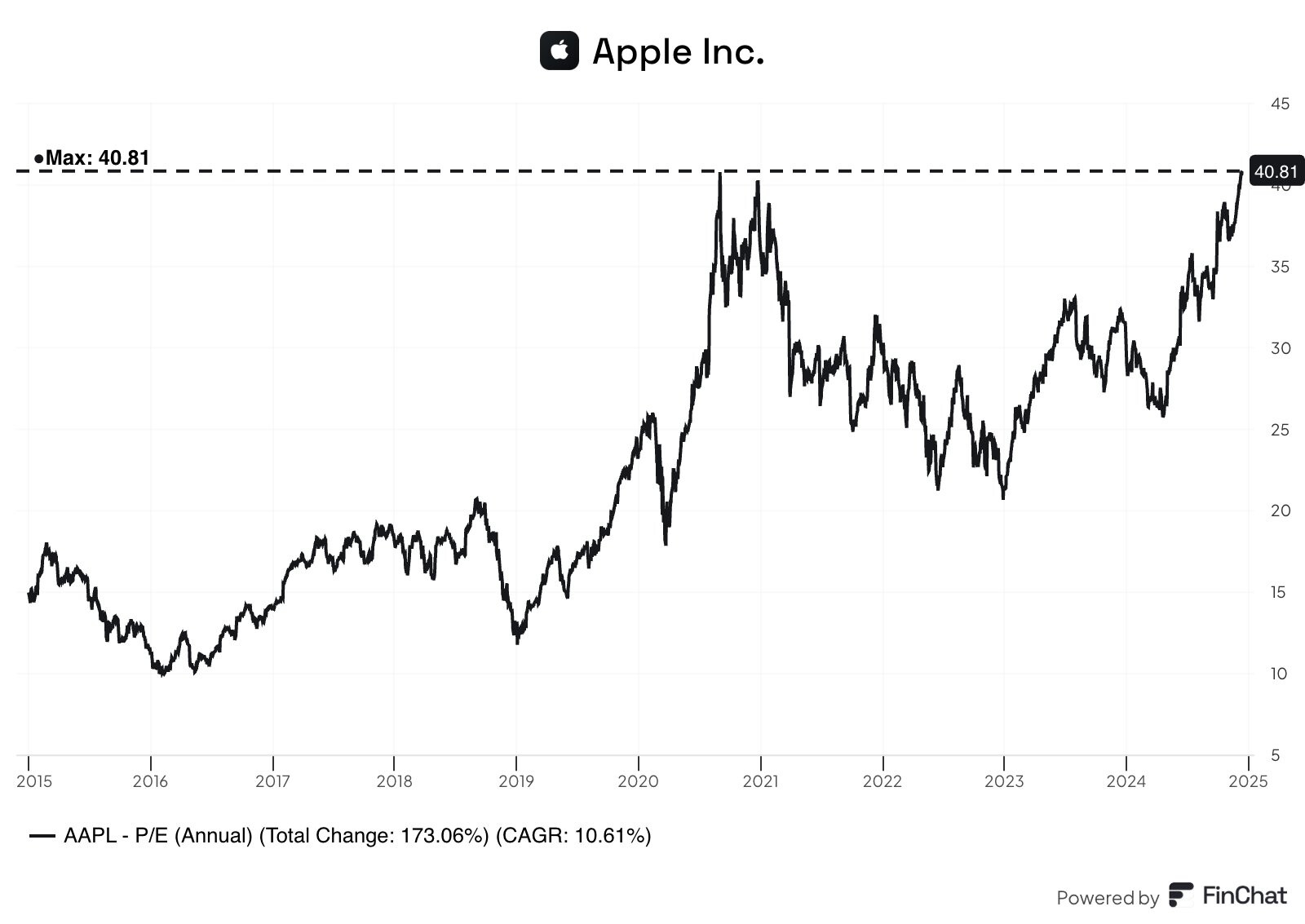

Below are some interesting charts about Apple, perhaps not that surprising if you’ve been following the company at all. ![]()

https://x.com/charliebilello/status/1855643148078248256

6 Likes

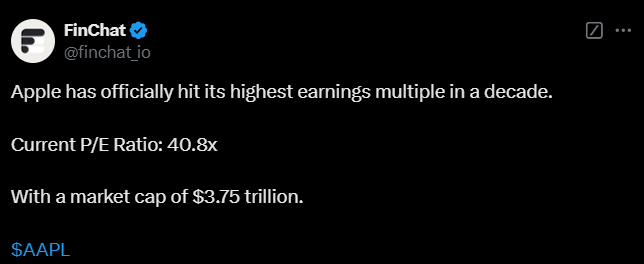

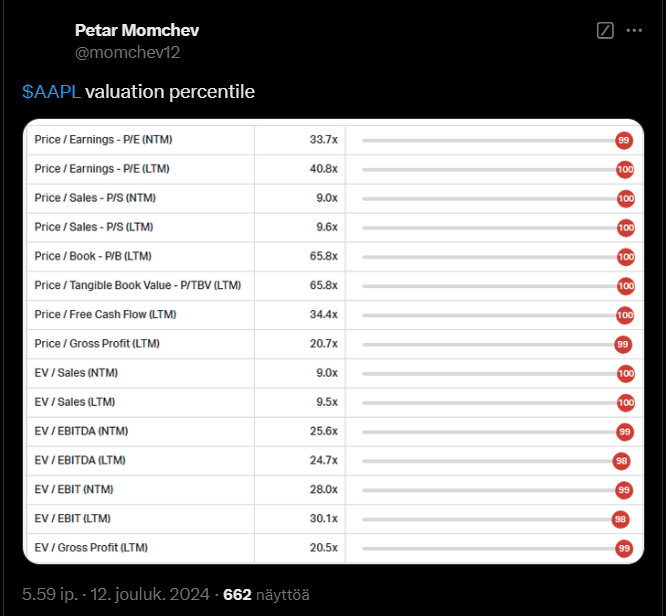

Here are a few tweets related to Apple’s valuations. ![]()

3 Likes

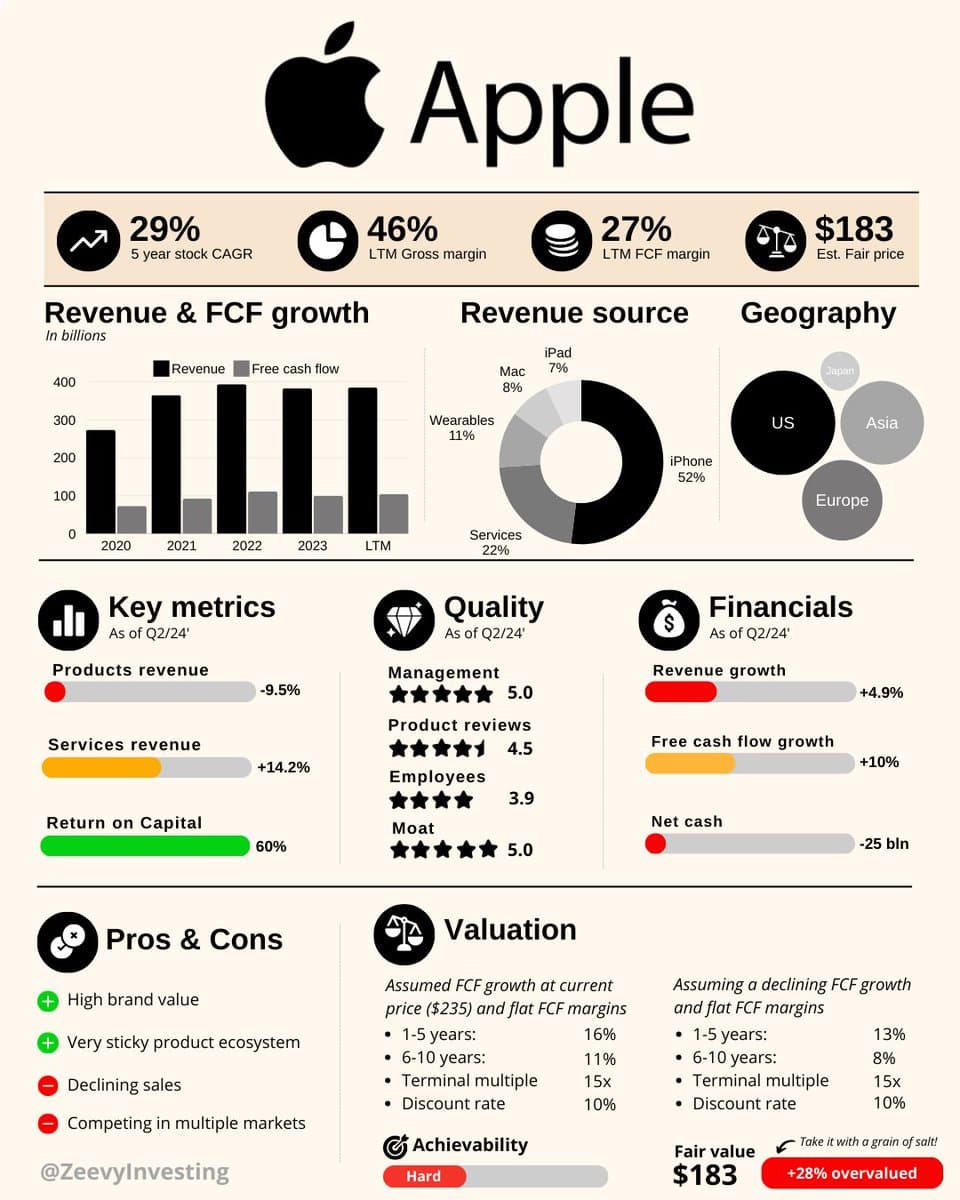

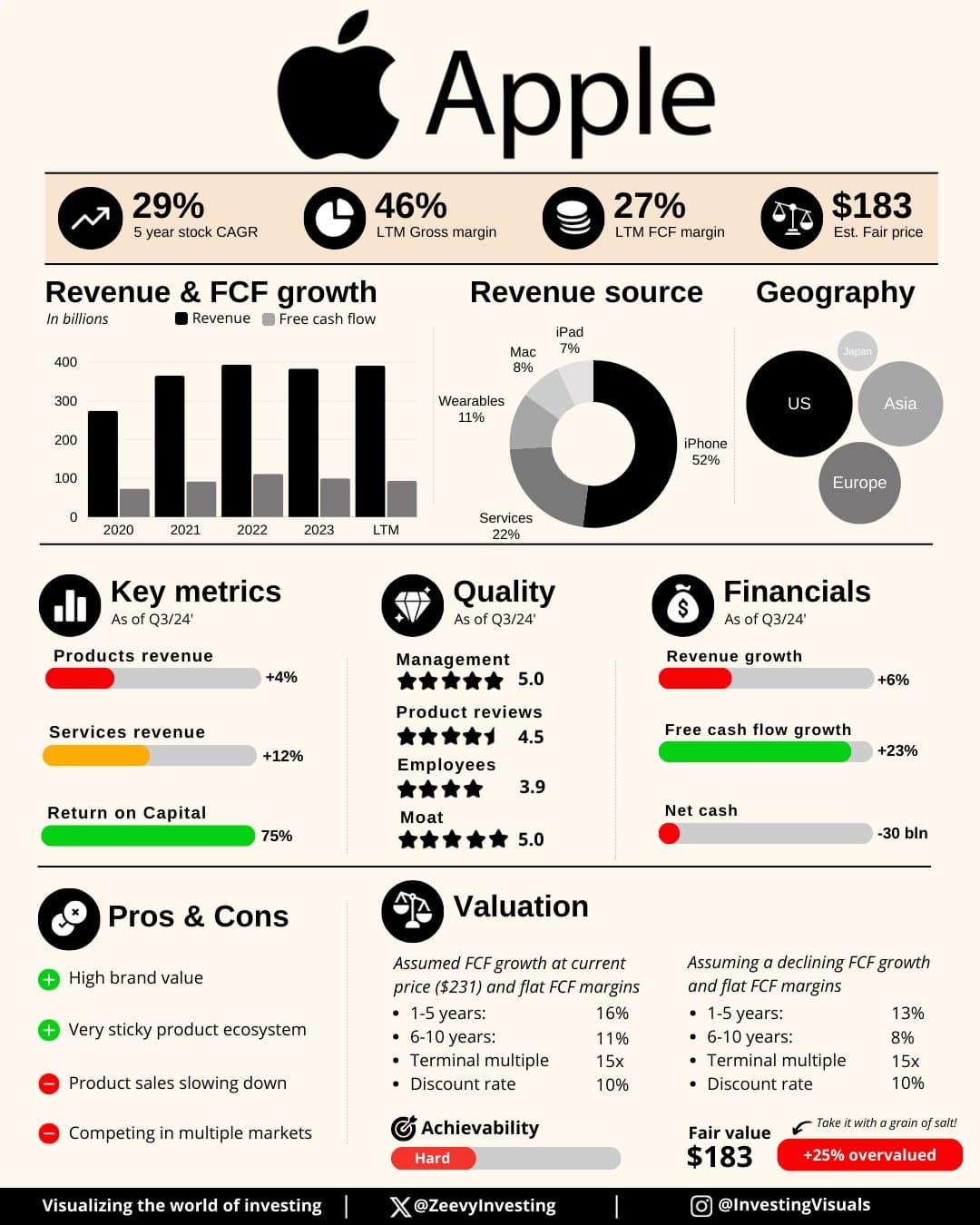

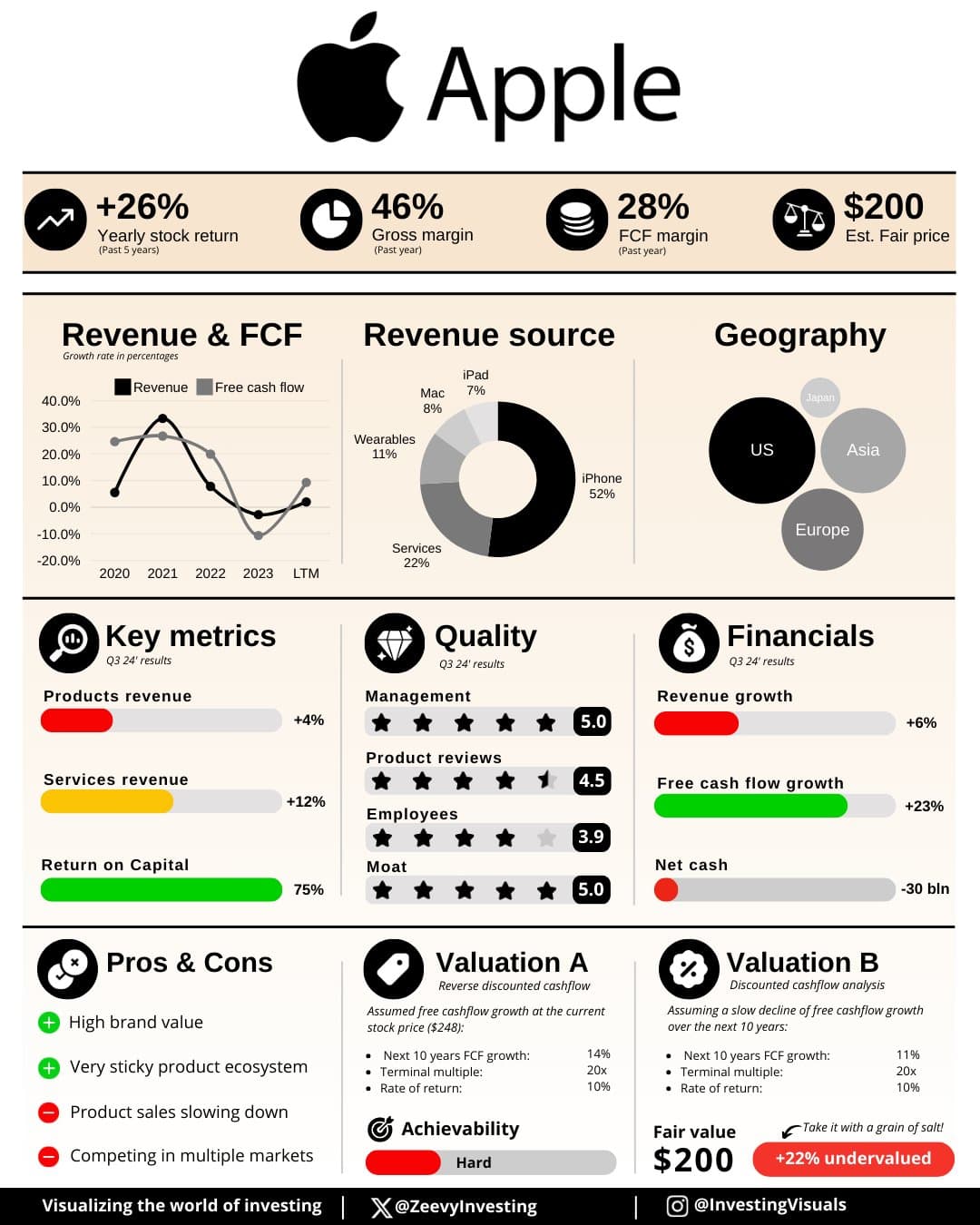

Here’s a concise, but pretty good overview of Apple. ![]()

![]()

6 Likes

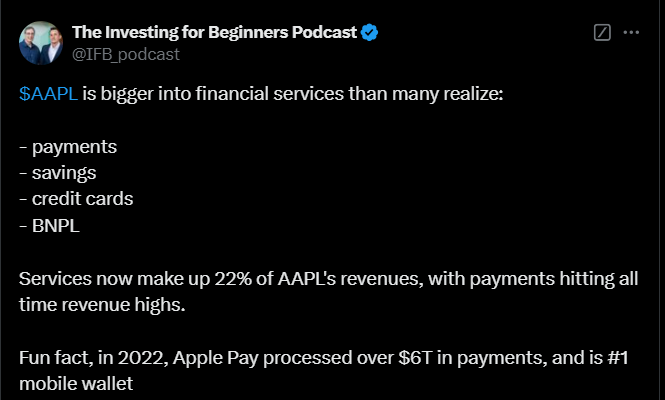

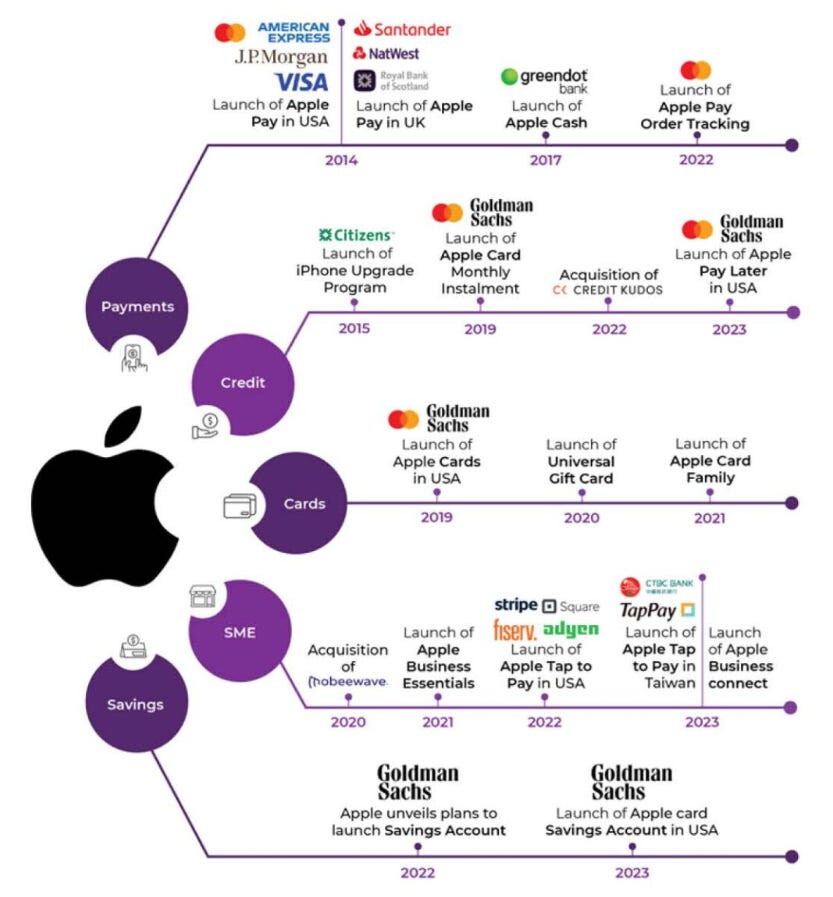

While the content of this tweet is surely familiar to many, I learned something new from it.

Apple is, of course, quite heavily involved in financial services: payments, credit cards, and installment payment services. Services account for up to 22 percent of the company’s revenue, and payments reached a record income level here.

In 2022, Apple Pay processed over 6 trillion dollars in payments and is the world’s leading mobile wallet.

10 Likes

I have quite diligently contributed my fair share to this pile. It is indeed a very useful way to handle payments on a computer, phone, watch, etc.

Years and years ago, a friend and I somewhat worriedly observed Apple’s results being so dependent on iPhone sales, but fortunately, the situation has turned in a healthier direction, and nowadays, services, for example, provide good support when considering the overall picture.

13 Likes

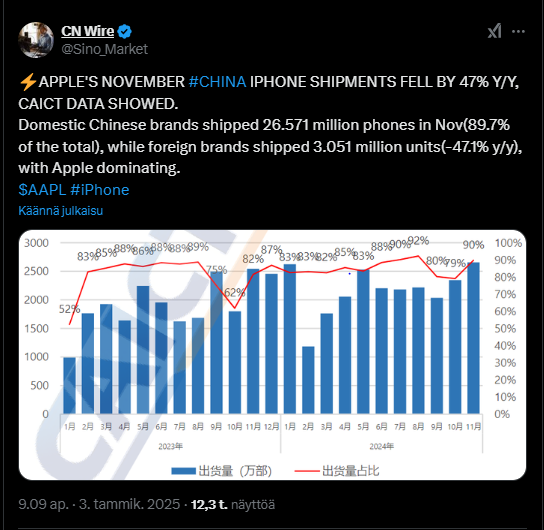

In November, Apple’s iPhone shipments in China decreased by 47 percent year-over-year.

Chinese brands dominated the market with an 89.7 percent share (26.6 million units), while foreign brands sold 3.05 million devices.

2 Likes

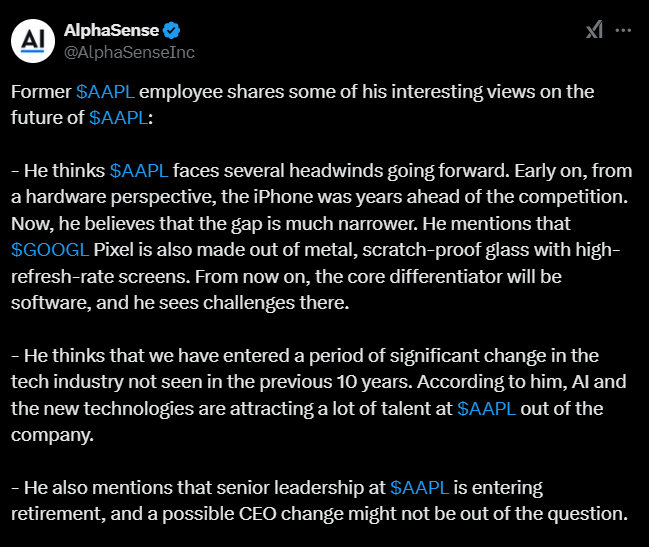

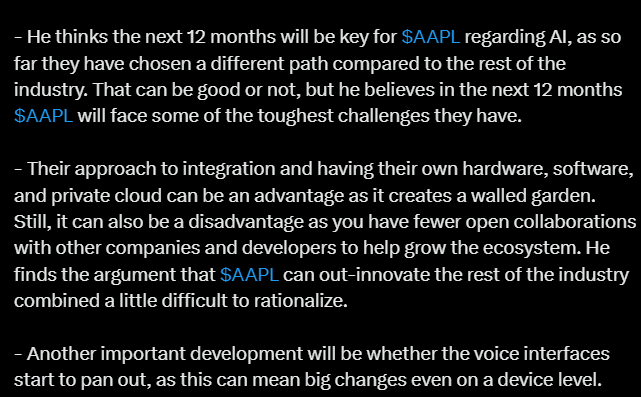

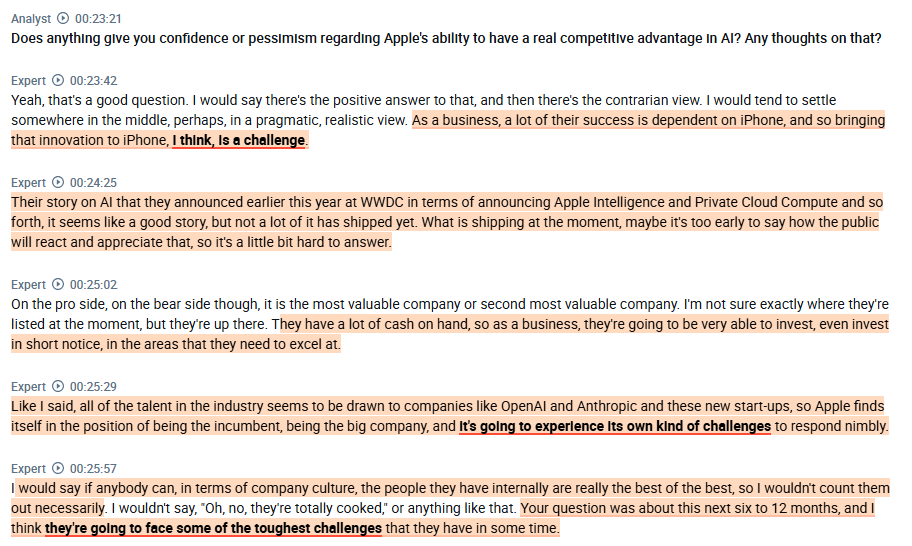

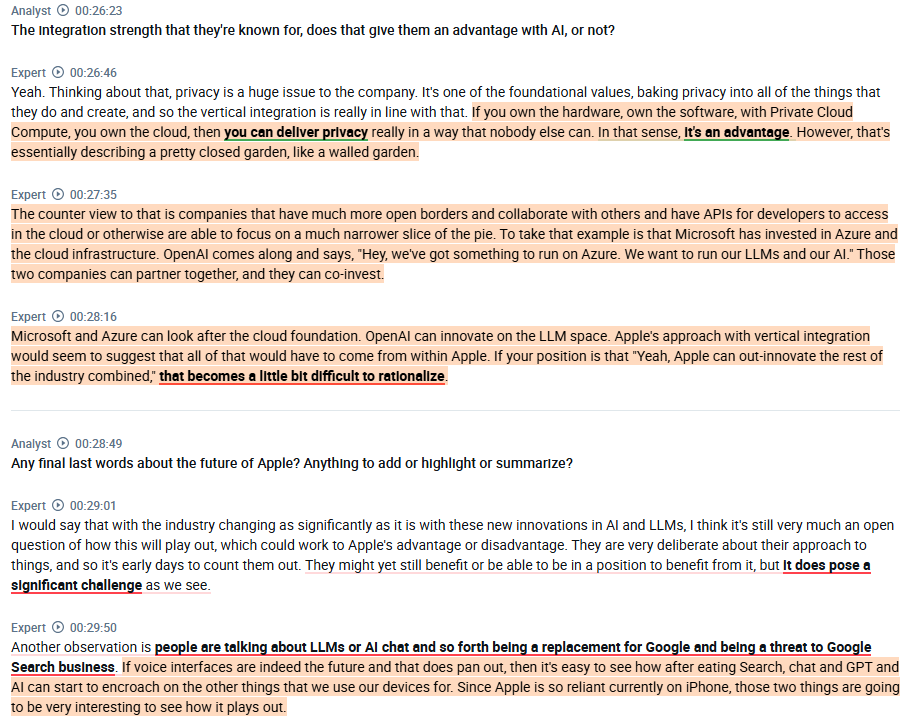

A former Apple employee estimates that the company faces significant challenges in the future. The iPhone’s previous technological lead has narrowed, and competitors like Google Pixel offer hardware of the same caliber.

Software emerges as a key differentiator, where he sees challenges. He believes that the allure of artificial intelligence and new technologies will draw talent away from the company, and additionally, management retirements and a potential CEO change could affect the company. Apple’s closed ecosystem is an advantage but limits collaboration opportunities.

The next 12 months are reportedly critical, especially regarding AI and voice assistants.

https://x.com/AlphaSenseInc/status/1877718986659430858

More comments from the ex-employee here

4 Likes