Huomenna 14. syyskuuta USA:n pörssiin listautuva Arm on mikropiirejä suunnitteleva ja valmistava yhtiö. Arm syntyi v. 1990 Acorn Computersin, Apple Computerin ja VLSI Technologyn yhteisyrityksenä. Pääkonttori on Cambridgessa, UK:ssa. Yhtiö oli listattuna Lontoon ja USA:n pörsseissä 1990-luvun lopulta vuoteen 2016, jolloin SoftBank osti sen itselleen 31 miljardilla dollarilla. Nvidia ja SoftBank sopivat vuonna 2020 Nvidian ostavan Arm:n 40 miljardilla. Kauppa kariutui kilpailuviranomaisiin.

IPO:ssa osakkeen hinta asettuu 47-51 dollarin haarukkaan ja markkina-arvoksi tulee IPO:ssa ennen kaupankäynnin aloittamista n. 52 miljardia.

Arm tekee mikropiirejä, joita käytetään lähes kaikissa mobiililaitteissa, samoin kattavasti IOT:ssa, ja myöskin monissa muissa tietokoneissa ja palvelimissa. Mikropiirien yksi keskeinen ominaisuus on alhainen virran kulutus. Arm on siis monopoliasemassa mobiililaitteissa. Kilpailijoina on lähinnä muiden siruvalmistajien ”avoimet” mikropiiriratkaisut, joilla on ainakin tunnusteltu vastavoimaa Armille.

Rohkenen sanoa, että kaikkien tärkeimpien teknologiatalojen ratkaisuista löytyy Arm:n mikropiirejä.

Armiin sijoittavan on hyvä tunnistaa Kiinariippuvuus. Arm Chinalla on osuus yhtiöstä. Sen takia on olemassa riski patenttien ja IPR:ien valumisesta yhtiön ulkopuolelle tavalla, joka ei ole länsimaisen lainsäädännön hallittavissa. Lisäksi lähes 25% yhtiön markkinasta tulee Kiinasta, ja yhtiön talousaineistoista voi tutkia, että maksamattomien laskujen osuudessa Kiina ylikorostuu. Maariski on siis ilmeinen. Mutta kolikon toinen puoli on se, että Apple, Nvidia, Samsung jne. tarvitsevat Arm:n ratkaisuja ainakin toistaiseksi. Arm on nyt monopoliasemassa.

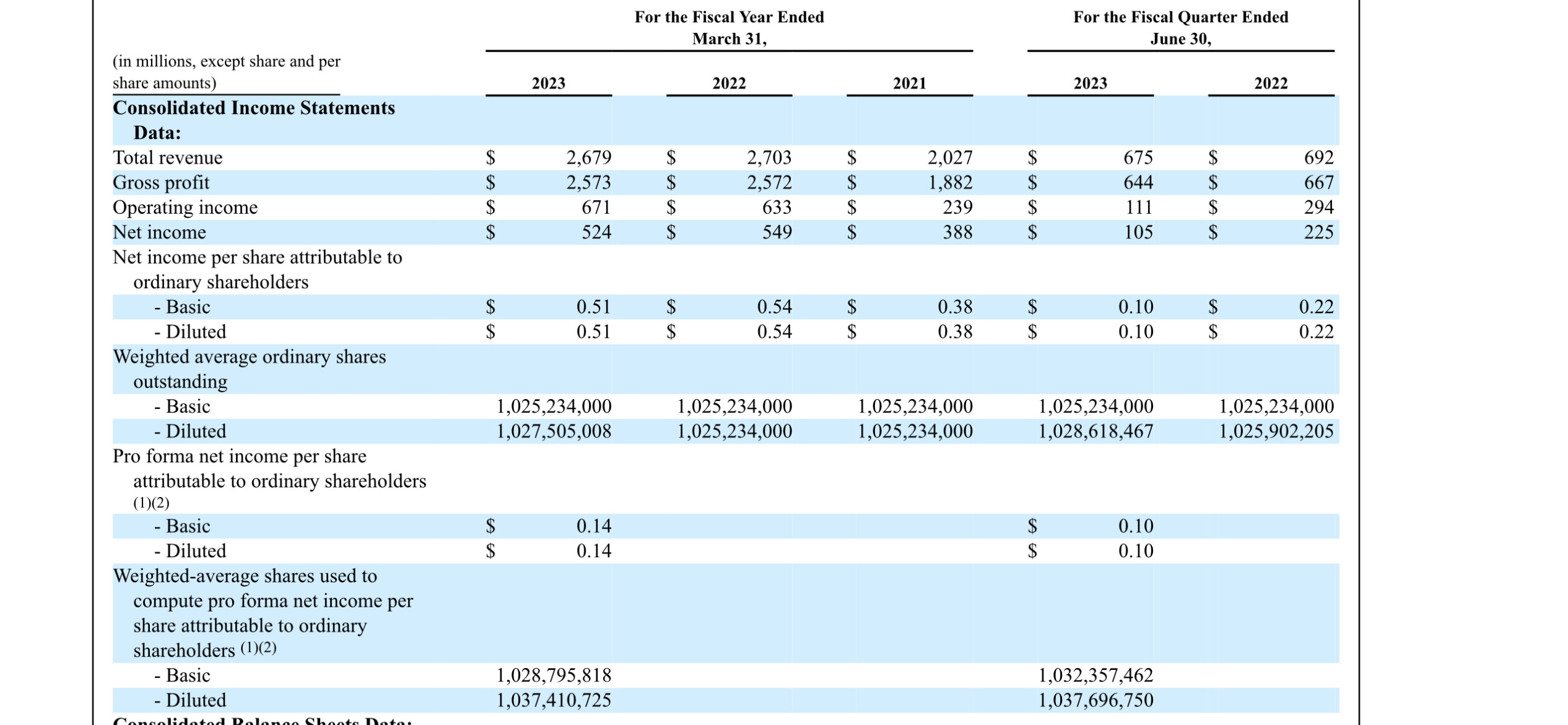

Arvostus 52 miljardia ennen kaupankäynnin avausta on paljon alle 3 miljardia liikevaihtoa tekevälle yhtiölle. Mutta Arm on vasta nyt astumassa pilvipalveluiden ratkaisuihin. Siellä se uusi iso kasvu on edessä. Ja toisaalta tuskin mobiili- ja IOT-palveluiden kasvu tulee taittumaan. Monopoli mobiiliratkaisuissa ei ole huono asetelma. Markkinahan mielellään hilaa tällaisen velattoman, kaiken ytimessä ja vieläpä monopoliasemassa oleva yhtiön hinnan pilviin. Mutta pilvilinnan puhkaisee kiinalainen omistus, joka voi halutessaan romuttaa yhtiön liiketoimintaedellytyksiä tavalla, johon emme ole länsimaissa vielä tottuneet.