OP’s Q1 preview, published today, estimates that Alma’s acquisitions have created shareholder value this spring. Recommendation and target price are on the rise.

“Alma Media’s clearly value-creating transactions do not, in our estimation, fully reflect the value of the share at present. We raise our target price to 11 euros (10), and our recommendation rises to BUY (Add). H1 is still difficult for the company, but the normalization of the operating environment in H2 will shift earnings development into a new gear. The share’s valuation is demanding with current year forecasts, but with 2022-2023 earnings development, we see clear upside potential in the valuation.”

Hey, Alma Media isn’t generating much discussion despite good earnings. I bought it as a new addition to my portfolio today because I wanted to see the Q1 results before buying. There seems to be clear upward pressure in the forecasts for this year.

Agreed. If the COVID-19 situation improves, Alma Media’s earnings growth could be a positive surprise. There are already better signs in the air and plenty of pent-up demand.

That was a positive first quarter. The recovery in the recruitment business was expected, as shown in HPL’s reports. The share of digital continues to grow, which is good. Here, too, it’s surprising how little Alma sparks discussion among investors during such a hot period, especially when most people encounter the company’s services or products in their daily lives. There’s certainly still hidden power in the synergies between different platforms.

Today, Alma for the first time in my portfolio. It’s an interesting company and involved in many positive-looking and surely profitable ventures!

But I’m truly surprised how little discussion there is here. Well, maybe it requires a good rise in stock price, then the interest will spark… I personally have expectations for a good long-term investment.

A very strong report, because ALL businesses are moving in the right direction. Digital business is the core in the long run, but a broad front will quickly digest, for example, acquisitions.

Looks like there’s some dispersion in the recommendations. Nordea today has it at €13 and a buy. The importance of digitalization is seen as positive and growing in the long term.

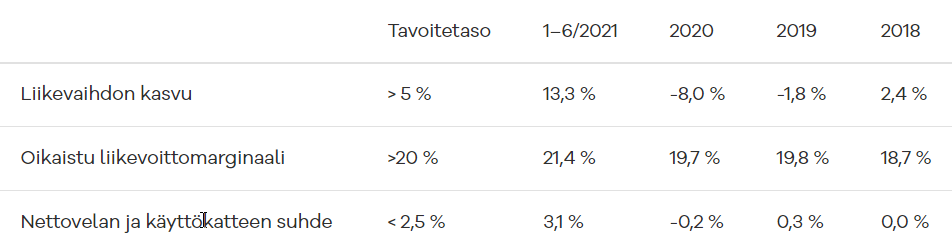

Alma Media has published new long-term targets. Regarding growth, it is stated that the target specifically refers to 2022 and beyond, including inorganic growth. 2021 growth will clearly exceed the target, as we are rebounding from the corona slump.

A rather bold comment from Alma’s CEO about phasing out print media:

Alma Media’s business will in the future be based one hundred percent on digital media, says the company’s CEO Kai Telanne.

“We will get there over time. It won’t happen in a year or two. My guess is that print media will still be produced for a good five to ten years.”

The direction is clear to everyone, of course, but 5-10 years is quite a short timeframe for a company that still owns a huge collection of different print media outlets.

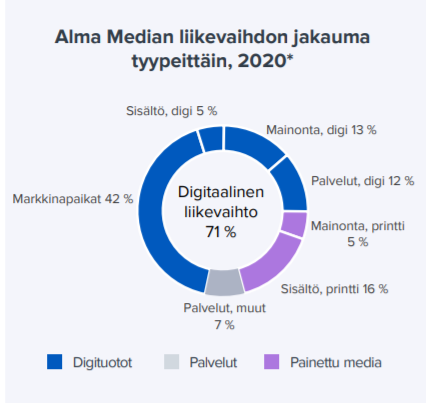

A huge pile is, of course, a subjective concept, but it’s good to note that for Alma, about 20% of 2020 pro forma figures (i.e., including Nettix) came from print (see screenshot from the latest comprehensive report below). It has also been estimated that revenues from print will decrease by several percent annually, so it will shrink quite a bit over the next 5-10 years, especially as other revenues will then generally grow. When you add to this that it is probably not reasonable to do print on a very small scale, e.g., due to printing costs, I would see Talanne’s estimate as quite realistic.