There was a discussion about Ålandsbanken in the Aktia thread. Perhaps it’s worth opening a separate thread for the company if it sparks further discussion. Over 2600 investors follow the company on inderes.fi. The company is not covered by Inderes.

The Group (source)

Ålandsbanken is a commercial bank listed on the Helsinki Stock Exchange. The company operates in Åland, mainland Finland, and Sweden. The Group consists of the parent company Ålandsbanken Abp and its branch in Sweden, as well as two subsidiaries (Ålandsbanken Fund Management Company Ltd and Crosskey Banking Solutions Ab). In addition to banking and wealth management services, the company also offers IT services.

The company’s headquarters are located in Mariehamn

Two branches in Åland (Strandnäs in Mariehamn, Finström)

Five branches in mainland Finland (Helsinki, Pargas, Tampere, Turku, Vaasa)

Three branches in Sweden (Stockholm, Gothenburg, Malmö)

History (source)

1919 Ålands Aktiebank is founded

1942 Ålands Aktiebank is listed on the Helsinki Stock Exchange

1980 Ålands Aktiebank changes its name to Ålandsbanken

1982 Helsinki branch opens

1991-1994 Finnish banking crisis, from which ÅB emerges as the only Finnish bank without state bank support

1992 Turku branch opens

2009 Ålandsbanken expands into Sweden by acquiring Kaupthing’s Swedish operations

2009 Branches open in Stockholm, Gothenburg, and Malmö

“In Åland, Ålandsbanken is the bank for all Ålanders, and the bank has both the position and the desire to be involved in developing the future of Åland.”

Strategy in Sweden: “In Sweden, the bank focuses on entrepreneurs, affluent families, and private customers with financial leeway.”

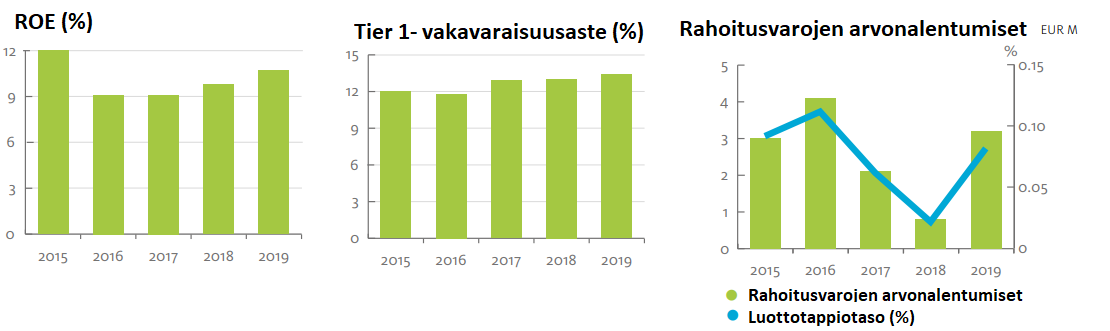

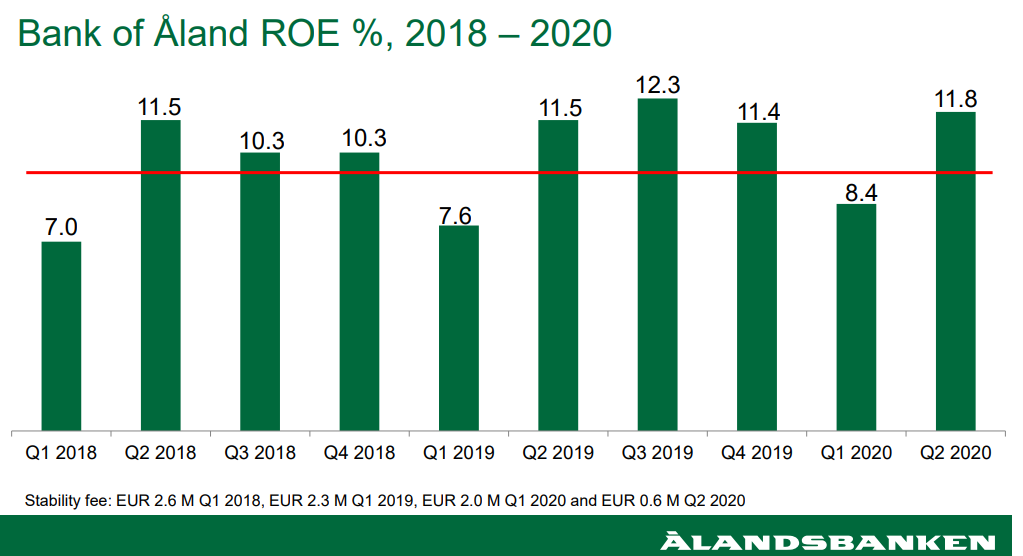

“In terms of operating profit, the second quarter (EUR 9.8 million) is the best we have ever achieved.”

Guidance: “Due to low visibility and high volatility in the markets, Ålandsbanken has decided that the bank will refrain from providing an outlook for 2020 for the time being.”

Loans: “72 percent of the loan portfolio consists of lending to private individuals, of which housing loans account for 77 percent. For private individuals, the second largest loan type is securities loans, collateralized by market-listed securities. The corporate portfolio is very similar to the retail portfolio, as in many cases the owners of the companies are also Private Banking clients.”

“The increase in non-performing loans due to the pandemic is not yet visible, but we expect negative effects to become more apparent next winter.”

The reference to the upcoming winter probably refers to the effects of the coronavirus pandemic on tourism in Åland. Talouselämä published an article on July 17 about tourism in Åland and the impact of the coronavirus (link to the article, currently freely available). Here are a few highlights from that article:

Åland Tourism

The absence of Swedish tourists is a major blow to Åland’s tourism. Tourism plays an important role in Åland’s economy because:

Tourism accounts for 15% of Åland’s GDP, and one in five private sector employees earns their living from tourism.

Tourism is heavily concentrated in the summer, with over 75% of tourism sector revenue coming from June-August.

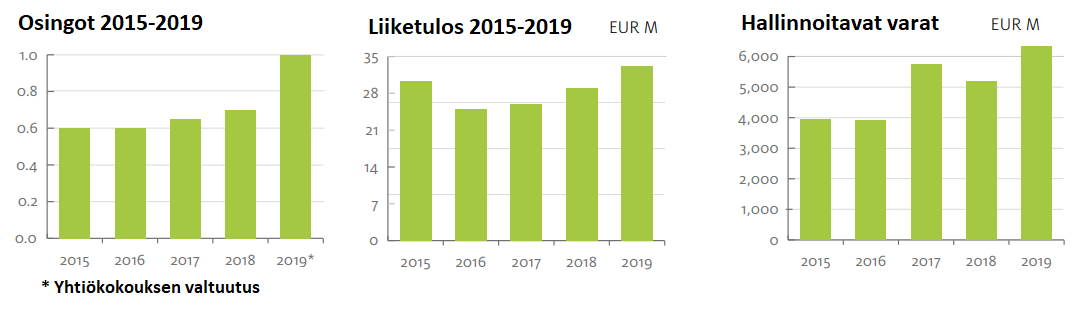

Negative impacts on tourism can affect the entire Åland economy. On page 21 of the half-year report, Ålandsbanken’s receivables from private individuals and companies are broken down.

However, for corporate receivables, the share of hotel and restaurant operations is small (EUR 35 million). How much tourism affects “other service activities” (EUR 103 million) is unclear. Also, the extent to which tourism businesses in the region have financial buffers for difficult times will naturally affect the situation.

On Sijoitustieto’s website, Aki Pyysing writes about Ålandsbanken and Nordea, which have published their interim reports. “Money rained down on Mariehamn from all doors and windows, meaning from all sectors.”

Eckerö’s subsidiary Birka Cruises has cruised between Mariehamn and Stockholm. Operations have been unprofitable for a long time, and the economic consequences of the coronavirus sealed the company’s fate. So, in that sense, it’s not solely caused by the coronavirus.

Updating the Ålandsbanken thread. A quiet period is now underway, and Ålandsbanken will publish its interim report for January-September on Thursday, October 22, 2020.

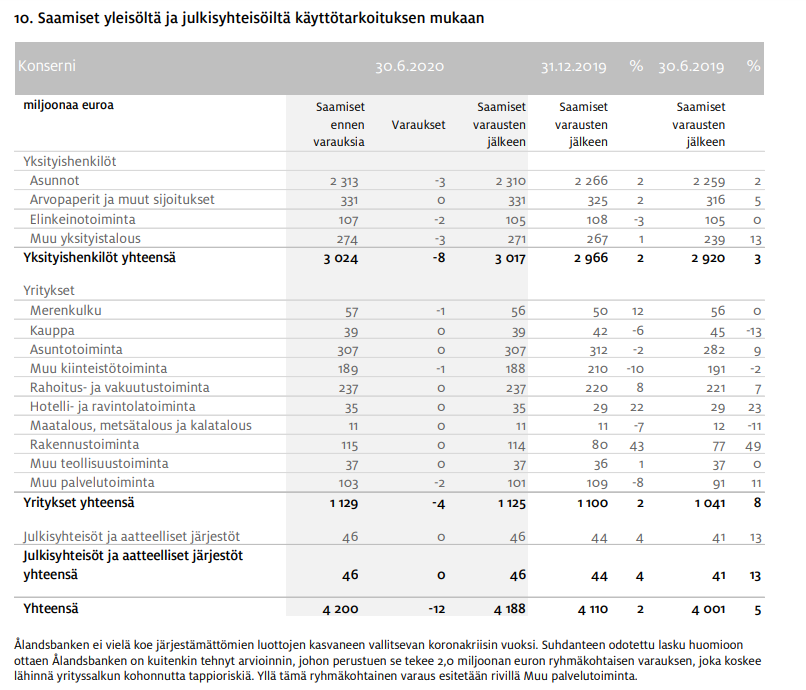

I’m highlighting the latest company presentation from Ålandsbanken’s website from July.

Quite a comprehensive slide series on Ålandsbanken (in English):

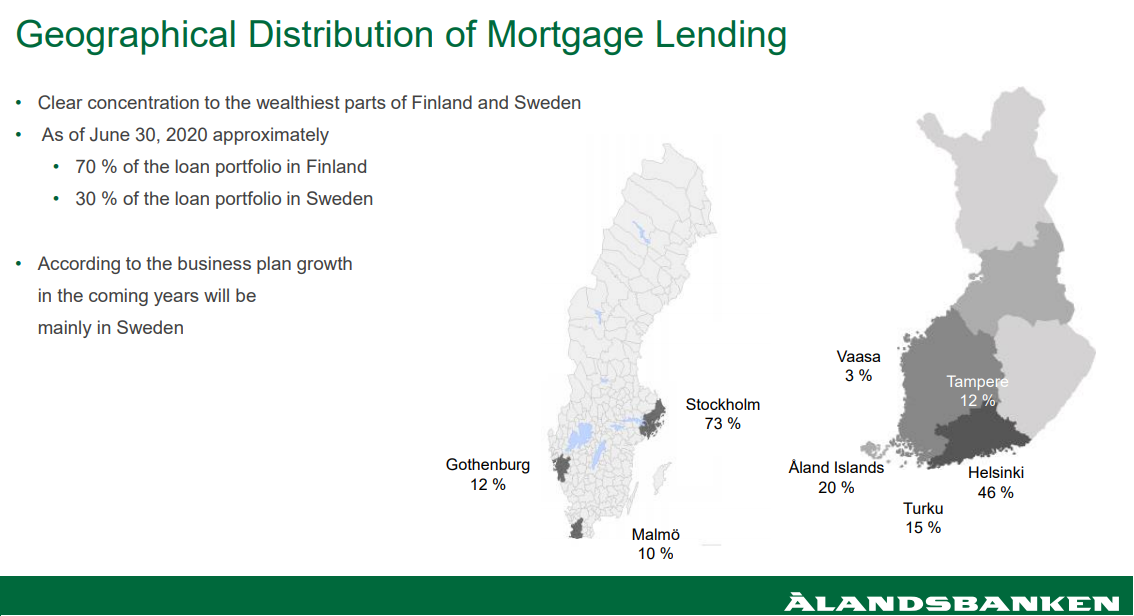

I’ve included a few images from that presentation in the thread. In Sweden, offices are in the three largest cities; Swedish market share < 1%.

January 10: The bank reported: The Ålandsbanken Global Equity Fund has been awarded the Nordic Swan Ecolabel.

In autumn 2019, Ålandsbanken’s sustainable bond fund, Ålandsbanken Green Bond ESG, received the Nordic Swan Ecolabel.

To receive the Nordic Swan Ecolabel, a fund must meet 25 mandatory criteria concerning exclusion, positive screening, transparency, and impact. By excluding investments in certain problematic industries and companies and instead choosing the most sustainable alternatives, companies can be influenced.

To obtain the Nordic Swan Ecolabel, a thorough sustainability analysis and an annual sustainability report on the fund’s activities are also required, for example.

Conclusion of the blog post: “it can be stated that there is a clear connection between sustainable development and return, and that ESG issues are an important part of investors’ selection process.”

New webinar recordings have appeared on Ålandsbanken’s Vimeo channel within the last couple of days.

Link to the channel:

Ålandsbanken Webinar September 14, 2020: general information on the Finnish housing market and ÅB’s housing fund (in Finnish): (Link to video: Ålandsbanken Suomi Live 14.09.2020)

Ålandsbanken’s September 2020 market strategy update (in Swedish):

(Link: Ålandsbanken Åland Strategidragning september 2020)

Content:

Our fund management team with Lars Söderfjell and Niklas Wellfelt gives you Ålandsbanken’s overall view on the economic cycle and financial development. Finally, you will also get to hear our analysts’ views on interesting stocks, such as Carlsberg, Sampo, and New Wave.

Niklas Wellfelt: A world economy on steroids? (on the recording at 4-18 min)

Lars Söderfjell: Fixed income: risk-free return or return-free risk?

Stocks: record-high multiples, but is it “expensive”?

According to preliminary information, strong performance continues: best ever quarter in terms of operating profit (+12%; Q1–Q3 +14%), ROE 12.3%. Guidance reinstated: operating profit better or significantly better than last year. I predict the stock price will react +8.4% today.

EPS could very well be €1.90 this year. Management is also confident about a strong year-end, as they provided guidance, thus removing uncertainty in that regard. So it feels cheap at a €20 price. A P/E of 12 would value the share at €22.80. Next year, a double dividend (last year’s and this year’s) could also be coming, i.e., €1 + €1, if the ECB approves.

I started researching Ålandsbanken late last summer. This was prompted by positive experiences with their wealth management services from a few Swedish entrepreneur colleagues. I was surprised at how little emphasis has been placed on the significance of wealth management in writings about Ålandsbanken, and I found a single line in last year’s annual report stating that Swedish wealth management (Asset Management Sweden segment) brought in over €21 million in net operating profit last year. That’s more than 60% of the entire bank’s profit! At the current market cap of €300 million, this would already be the value of just the Swedish wealth management business…

One thing puzzles me. How essential is this “traditional banking” to wealth management companies? Are there actual synergies between banking and wealth management, if some conclave decides to build this speculated “wealth management powerhouse” in Finland? In other words, is banking even needed at all…

I’ve been thinking the same thing myself. Not just about Ålandsbanken, but generally. If asset-intensive lending in the banking sector isn’t profitable, why not just make a move that protects shareholder value and stop lending and distribute the PB <1 business as dividends .

Could I get the page number of the annual report, as I didn’t notice that Ålandsbanken explained anywhere what the misleading way of presenting the results entails. However, I have read the document both in Swedish and in English. Of course, it’s possible that my thoughts wandered in both languages. Thanks.

Good question, and in my opinion, ÅB’s potential is quite well hidden in the IR materials. In the English annual report, the Swedish private banking segment is presented on page 26.

In the middle of that page, there’s a paragraph:

“Net operating profit from Private Banking Sweden in 2019 amounted to EUR 21.1 M, which was equivalent to 64 per cent of the Bank’s total net operating profit. Return on allocated equity was 17.4 per cent.”

I’ll join this speculation myself: I’ve been speculating that in the consolidation of asset management, there might also be a playbook where ÅB and Aktia would merge. ÅB has quietly built a foothold in Sweden with a Private Banking focus and would be a “match made in heaven” with Aktia. What would be missing from this equation, in my opinion, is backward integration in the asset management value chain, for example, a CapMan-type operator that acts as a value creator. This would be a true Nordic Powerhouse in asset management. The only thing still missing from this equation would be a marketplace for unlisted shares and other securities. But nothing would prevent building such a thing if its position strengthened.

I, for one, have recently bought all these stocks in the asset management value chain because arrangements will come sooner or later, and value will be realized through some card. Now, asset values have also risen sharply, so the Q3 & Q4 results for these players will again be a positive surprise for many. In terms of valuation, these boutiques are currently lumped into the same trash bin as banks, even though ÅB and Aktia’s customer base has significant financial leeway that the corona crisis doesn’t bite in the same way. Also, stimulus money will eventually sail here one way or another.

I’d say by the end of next year, ÅB will be a 30-euro stock and Aktia 15 euros. At least.

In Sweden, the interest rate is considerably higher than in Finland, and mortgage lending is apparently very profitable. What a mistake. Conquering Norway would be even more profitable.

Ålandsbanken is not just any bank, but a century-old embodiment of the Åland provincial spirit. Although basic banking operations only account for 10% of its profit, they will not be discontinued, even if they were to consume 10% of the profit. A soul cannot be measured by money.

Juurikki owns Ålandsbanken, but by no means believes the price could be €30 in a year. More like €18-23. ÅB is already overpriced in its peer group, i.e., finance/banks. Compare, for example, P/B ratio to Nordea. P/E perhaps a little better. ROE over 10, so okay. Future prospects are already priced in, at least partly.

Banks also have the downside that they don’t have to disclose their balance sheets publicly in detail. ÅB likely has a lot of interest-bearing securities, but what else? We do know that the amount of unlisted investments does not exceed the annual profit. And the EU-mandated loan loss provisions are not at all the worst. Still, never trust a bank, says Juurikki, who participated in KOP’s national fund-raising drive when he was smaller and even dumber than he is now.

Yes. In addition, those banking customer relationships are one way to acquire assets under management (AUM) for wealth management. If the pride of Åland puts an end to banking, tens or hundreds of millions in AUM could be lost as local patrons withdraw their funds.

Ålandsbanken’s operating profit in Q1-Q3/2020 saw strong growth of +14%. Commission income grew by as much as 15% in the early part of the year. One can only imagine, with market values having risen and commission income growing with them; for example, the Ålandsbanken Maailma equity fund had over a billion in assets at the end of September, after which markets have risen strongly – and commission income with them. I don’t know if I’m the only one who thinks the market isn’t pricing this asset management-focused case correctly.