It probably needs its own thread. A large domestic company with little discussion. A turnaround has been awaited for a long time. Is it time now?

-Relevant to this moment is especially sustainable development and recyclability in fiber products. Rapidly started the production of facial mask fiber material in Finland.

-Produces fiber raw material for masks sold by domestic K- and S-chains.

-Is it aiming for international mask markets in the production of both ordinary consumer masks and medical masks?

Production of face mask materials started in Tampere in April.

Below is a slightly modified quote taken from the company’s website.

Ahlstrom-Munksjö is a global leader in fiber-based materials, offering innovative and sustainable solutions to its customers worldwide. The offering consists of filter media, release liners, materials for food and beverage processing, laminating papers, abrasive and tape backings, electrotechnical papers, glass fiber materials, and fabrics for healthcare and diagnostic applications. In addition, a wide range of other specialty papers for industrial and consumer use. Annual net sales are approximately 3 billion euros and the company employs approximately 8,000 people. Ahlstrom-Munksjö’s shares are listed on Nasdaq Helsinki and Stockholm.

Half-year review January-June 2020: 28.7.2020

-Dividend 0.52€ in four installments, 0.13€ each. Next installments in October and January. The Board decides on each dividend payment separately. This year’s dividends have been paid in April and July as planned.

-Half-year review 28.7.

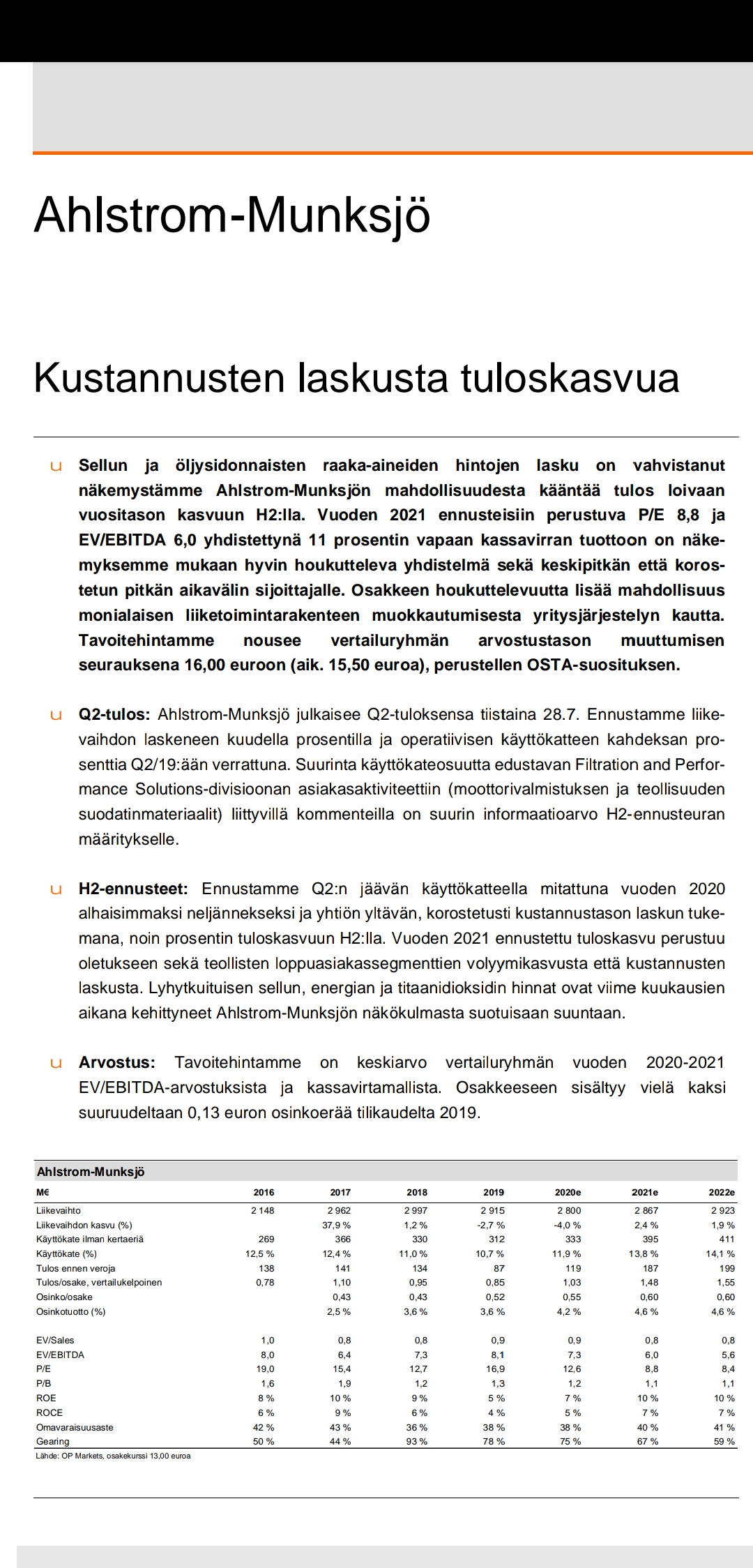

OP raised the target price for Ahlstrom-Munksjö shares to EUR 16.00 from EUR 15.50. The recommendation is a buy. The share ended with a 3.4 percent increase at EUR 13.50.

Good that we got a thread for Ahlstrom-Munksjö as well!

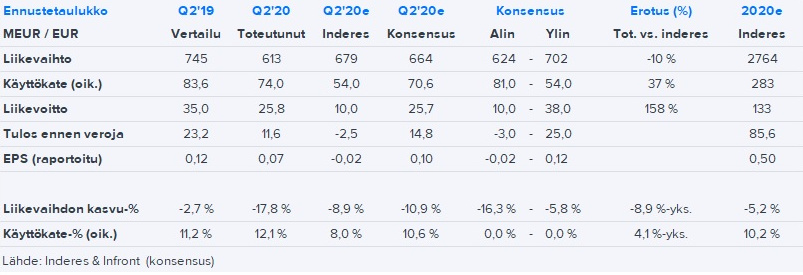

Q2 indeed comes out tomorrow, our preview was in this morning’s morning report. The guidance has not been changed, so the result will be lower than the comparison period, but the question mark is how much. Businesses driven by industry and construction have probably been in trouble in Q2, while the situation in the consumer sector is more stable and the market in the small healthcare segment is naturally very good. However, the outlook and guidance for Q3 are more important, but like the consensus, we do not expect earnings growth to start in Q3 yet. The cost environment is now favorable for Ahlstrom-Munksjö, and at least next year there is room to improve results if demand is reasonable and there are no widespread price pressures.

The long-term perspective on the company has been covered in Ahlstrom-Munksjö’s extensive report, which is from last autumn but still contains valid information. A new extensive report is planned for H2.

Q2 numbers are out. Adjusted EBITDA was strong in Q2, beating market expectations and especially our own forecasts, thanks to a decrease in expenses (including variable and fixed costs, and likely some one-off savings). Revenue, however, fell more than forecasts, primarily due to lower-than-expected volumes in end-uses driven by industry, transportation, and construction (Q2 group volumes -10%). However, further down the income statement, EBITDA was eroded in a somewhat typical fashion for the company, due to factors such as minor one-off expenses, higher-than-expected depreciation, and elevated financing costs. As a result, EPS ultimately fell short of consensus expectations. Despite the circumstances, the good EBITDA in Q2 did not translate into cash flow, due to the aforementioned reasons and the tying up of working capital.

For Q3, Ahlstrom-Munksjö guided for a weaker adjusted EBITDA compared to the reference period, which we believe was expected. Earnings will continue to be impacted by declining volumes, although the company has reported some signs of demand recovery. In addition, maintenance at the Aspa pulp mill will increase costs in Q3 (if I recall correctly, it was in Q4 last year).

The market reaction to the report was negative, at least for the first half hour (A-M share now -7%), which likely reflects the structure of the Q3 earnings lines, cash flow, still very cautious outlook comments, and the increased valuation in recent weeks. The investor call starts at 1 p.m. and can be followed here.

THL will provide more information on face mask recommendations on Thursday. Today’s Helsingin Sanomat (Hesari) features an article mentioning Ahlstrom-Munksjö.

"K-GROUP has been involved in Ahlstrom-Munksjö’s and Filterpak’s domestic mask production project. As the ordering party for the masks, K-Group is also responsible for their logistics and distribution. The Nesu-brand face masks sold in K-stores are manufactured at Filterpak’s factory using Ahlstrom-Munksjö’s materials.

“We are pleased that domestic operators have joined mask production. It will certainly ease the situation to have products available nearby,” says Hovi.

K-Group can also plan to increase production in cooperation with Ahlstrom-Munksjö and Filterpak if needed.

“The manufacturers are assessing whether new production lines need to be set up or if new processors will join. Ahlstrom-Munksjö also makes materials for other manufacturers.”

This Finnish AM turnover in the production of mask materials is quite small considering the company’s overall business. I have been wondering if AM has prepared to start production in other countries. This epidemic is likely to continue for a very long time. And it is possible that the entire future ahead is different. Global mask consumption may permanently rise to a completely new magnitude.

Vaccination is unlikely to eliminate the risk of infection. It remains to be seen what its effectiveness will be, but I would not be surprised if it remains at 30-50%. Even that is already a significant benefit. What will AM’s share be in mask production in the future? At least they have acted quickly domestically.

A&M has mask fabric manufacturing plants in the United States, Brazil, Belgium, France, and Tampere. In total, the plants can produce approximately 800 million masks per month.

"Among the nine mask fiber manufacturing plants, Tampere is among the smallest in terms of production scale. Four of the plants can produce fiber for 150 million masks per month.

Of the large plants, two are located in the United States, one in Brazil, and one in Belgium. There is also a plant in France, whose fabric production is sufficient for one hundred million masks per month."

I think this is a real shame. We were supposed to start reaping the fruits only from next year onwards. Back then, Ahlström looked like a really boring company, but the merger with Munksjö and the many acquisitions that followed made the company very interesting. It’s a shame that this also goes now with a premium of over 30%, even though, for example, in a year’s time the share might be hovering around those levels as the earnings performance improves.

Edit: Ahlström Capital’s dual role looks a bit shady. They are selling and buying the company at the same time. They apparently want to get rid of other investors.

I was wondering about this myself. The board recommends accepting the tender offer while the companies they represent are buying A-M. I think the premium is a bit low, but this is clearly what’s happening.

I bought into the corona dip in the spring and would have liked to see AM in my portfolio for a long time still. I’m not particularly excited about this takeover bid, but I think it’s likely to go through at this price. I immediately sold my shares and the freed-up capital has already been reinvested.