Ålandsbanken’s report was somewhat mixed.

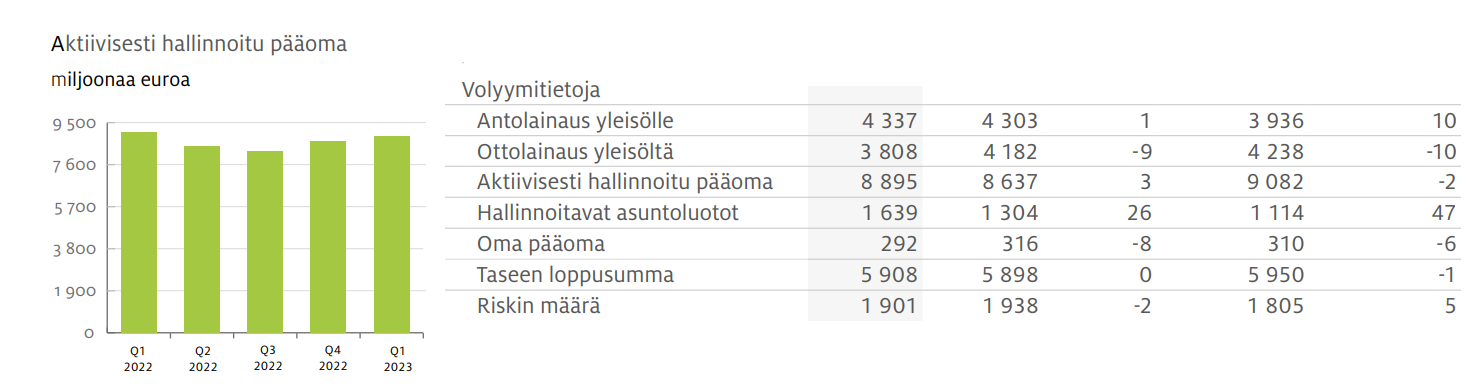

On the positive side, Peter Wiklöf stated in the Q1 report that he still sees new capital flowing into the bank’s investment services for management. Although the market situation has certainly put pressure on the bank’s assets under management (AUM) in Q1, actively managed capital grew by 3% to EUR 8,895 million (8,637).

Based on the report’s figures, Private Banking capital grew by 3% to EUR 8,177 million and Premium Banking by over 3% to EUR 709 million. Looking back at the situation a year ago, Private Banking capital has decreased by 3% from EUR 8,419 million a year earlier. Premium Banking capital has grown by 8% from EUR 654 million a year ago.

Housing funds have suffered from the weakening of the housing market, as has Ålandsbanken’s housing fund. Relatively speaking, assets under management have maintained their level.

Regarding Nordic banks, the situation is somewhat twofold. Net interest income is growing nicely, but there are also question marks looming in the background. A couple of weeks ago, Peter Seligson stated in a Talouselämä interview that money is flooding into European systemic banks, such as the Dutch bank ING. This money is leaving major Nordic banks like SEB or Handelsbanken, and slightly also boutique-type Ålandic banks.

Will the operations of Nordic banks shrink as money flows to systemic banks? At least for Ålandsbanken, during the first quarter, deposits from the public decreased by EUR 374 million, or 9 percent from the turn of the year. Deposits were EUR 3,808 million (4,182). Thus, Ålandsbanken’s loan-to-deposit (LDR) ratio rose to 114 percent (103).

There are clear differences in the financial structure among Finnish peers. For example, Aktia’s LDR ratio was 149% according to the 2022 financial statements, while for S-Bank it was 84% according to the 2022 financial statements (p. 13).

A larger part of Ålandsbanken’s funding now consists of deposits from the public, as the bank no longer has Swedish covered bonds. According to the 2022 financial statements, deposits from the public accounted for 77 percent (66) of the bank’s funding. At the same time, competitors are more active than before in acquiring deposits.

Among competitors, Aktia Bank stated in its 2022 financial statement release (p. 21) that retail deposits are an increasingly affordable form of funding alongside wholesale funding in the current interest rate environment. Consequently, Aktia is more active than before in acquiring deposits.

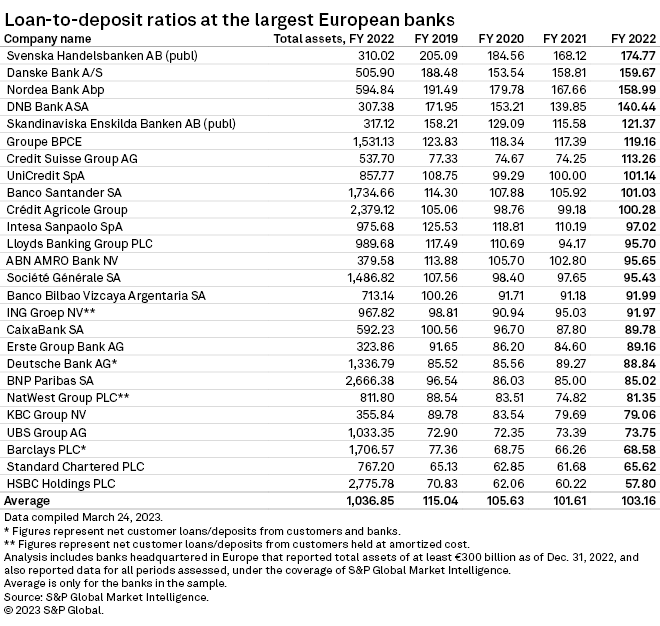

Banks’ dependence on wholesale funding varies. Among Swedish banks, Handelsbanken had an LDR ratio of 175% at the end of 2022, and the bank is highly dependent on wholesale funding. Credit rating agency DBRS Morningstar wrote in its report at the end of March that Handelsbanken’s dependence on wholesale funding is very high compared to other European banks and the highest among Nordic countries, which could be a potential vulnerability in the current environment. DBRS Morningstar Confirms Handelsbankenâs LT Issuer Rating at AA (low), Stable Trend | Morningstar DBRS

The topic gained more visibility at the beginning of April when S&P published a story about European banks’ loan-to-deposit ratios. Handelsbanken, Danske, and Nordea were at the top of the list. Many certainly consider the loan-to-deposit ratio an old-fashioned metric of a bank’s financial situation. On the other hand, many of the sophisticated liquidity management metrics used by banks’ treasury units are very laborious and too complex in rapidly evolving crisis situations.

Ålandsbanken’s core capital ratio (CET1) has been on the decline. At the end of 2022, the average CET1 ratio for European banks was around 15 percent. For Ålandsbanken, at the end of 2020, it was still at a good level of 14.3 percent, but by the end of 2022, the CET1 ratio was only 12.0 percent. Now, during the first quarter, the CET1 ratio grew to 12.4 percent, so things are moving in the right direction again.

The rise in interest rates is now boosting the bank’s coffers. For Ålandsbanken, net interest income grew by 38 percent to EUR 19.8 million, compared to EUR 14.3 million a year ago. The growth in net interest income was at the same level as a couple of other banks that have published their results. Handelsbanken Finland reported on Tuesday that net interest income grew by nearly 40 percent from a year ago. Yesterday, Nordea reported that net interest income grew by 35 percent, reaching nearly EUR 1.8 billion. Aktia will not publish its interim report until May 11, so we will have to wait a couple of weeks for the competitor’s figures.

Yesterday, Borgo also published its annual report.

In its financial statement release on February 1, 2023, Ålandsbanken stated that it currently owns 19 percent of Borgo, so the bank remains among Borgo’s 4 largest owners. The year 2022 was loss-making for Borgo, but according to the annual report, the construction phase is progressing.

-

CEO Gustav Berggren states in his review (p. 3) that Borgo is developing into a full-scale mortgage company.

-

At the beginning of 2022, Borgo carried out an investment round to finance the acquisition of Ålandsbanken’s mortgage portfolio. A total of approximately SEK 1.3 billion in capital was raised, with participants including investment companies Persson Invest, Proventus Real Alliance, and Neptunia.

According to Berggren (p. 3), another important milestone was Borgo’s first one-billion-kronor covered bond. -

Together with distribution partners, Borgo aims to increase volumes. Sparbanken Syd has joined as a new mortgage distributor. According to Berggren (p. 3), the plan is to reach the targeted profitability level during the autumn.

“Our plan is also to reach profitability during the autumn. If we live up to that, we have good opportunities to become the primary challenger in the mortgage market during the year.”

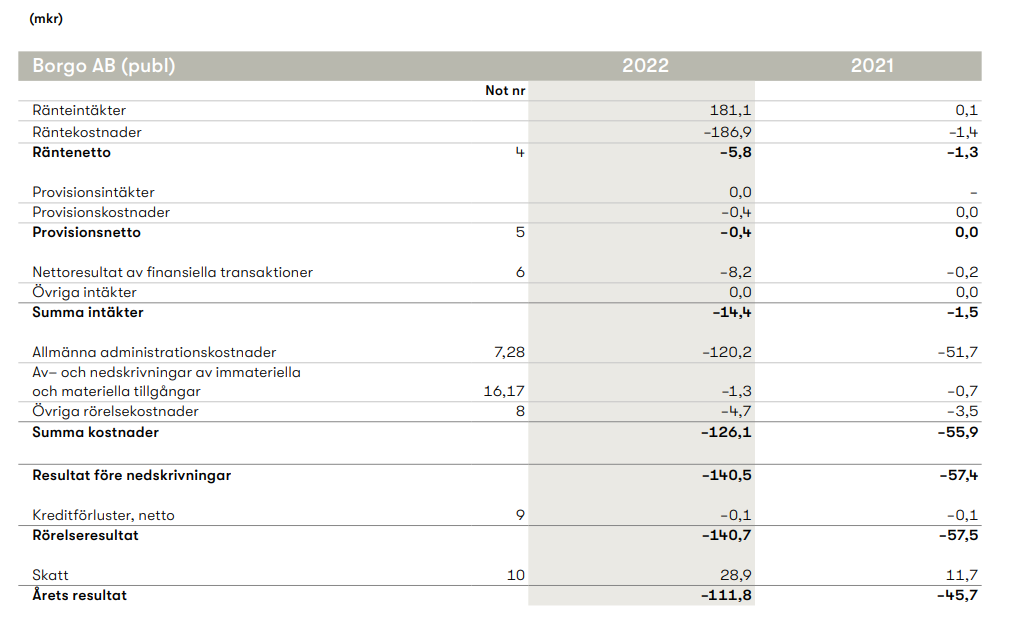

- Borgo’s result for the 2022 financial year was SEK -111.8 million, compared to SEK -45.7 million the previous year.

- Net interest income was SEK -5.8 million. The negative net interest income was mainly due to pre-financing of completed and future acquisitions.

- Expenses grew to SEK 126.1 million (55.9), mainly due to investments in the company’s construction phase, which Borgo expects to support the company’s future earning capacity.

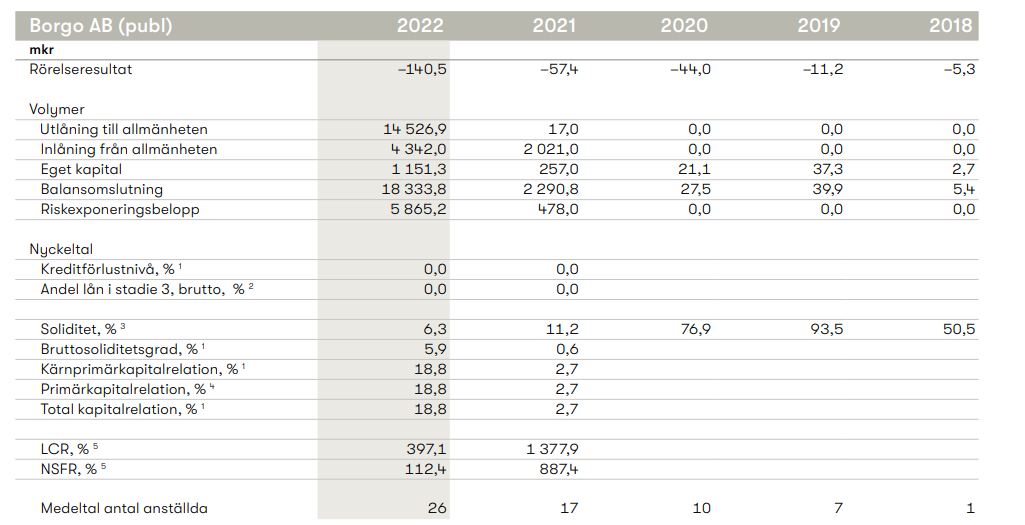

- Borgo’s lending to the public grew to SEK 14,526.9 million (17.0) following the acquisition of Ålandsbanken’s loan portfolio.

- Deposits from the public grew to SEK 4,342 million (2,021).

(report pages 25 and 28)

Borgo’s Owners

According to page 4 of the annual report, Borgo’s largest owners are ICA Banken, Ikano Bank, Söderberg & Partners, and Ålandsbanken. Other owners include Sparbanken Syd and investment companies Persson Invest, Proventus Real Alliance, and Neptunia. Persson Invest, Proventus Real Alliance, and Neptunia all participated in the funding round carried out in 2022.

- The chair of the board is Eva Cederbalk, who has previously served as the CEO of SBAB Bank, among other positions. The board also includes Ålandsbanken’s CFO Jan-Gunnar Eurell.

- Both Eurell and Cederbalk are also members of the board of Plusius AB. According to the corporate register, Cederbalk was elected to the Plusius board in October 2022 and Eurell in March 2023. Ålandsbanken invested in Plusius last year. Styrelser | hitta.se