Administer announced today for First North

Administer is a group providing financial and payroll management services, consulting services, and software services. The company aims to reform the financial management services market by developing new technology and new solutions. According to its management’s assessment, Administer is one of Finland’s largest providers of financial management services measured by revenue, and Finland’s largest provider of HR and payroll management services measured by the number of payslips.

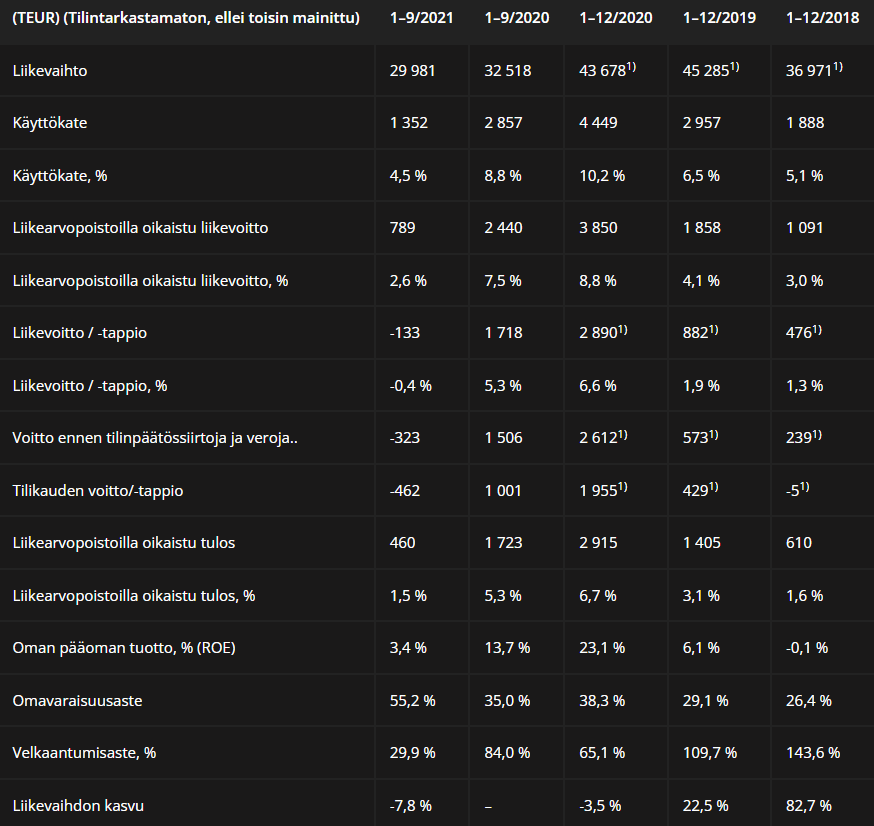

Revenue 2020 44 MEUR, the offering aims to raise 11 MEUR for the company, and in addition, current owners are selling their shares. Subscription commitments totaling 12.6 MEUR if the pre-money valuation remains at 55 MEUR.

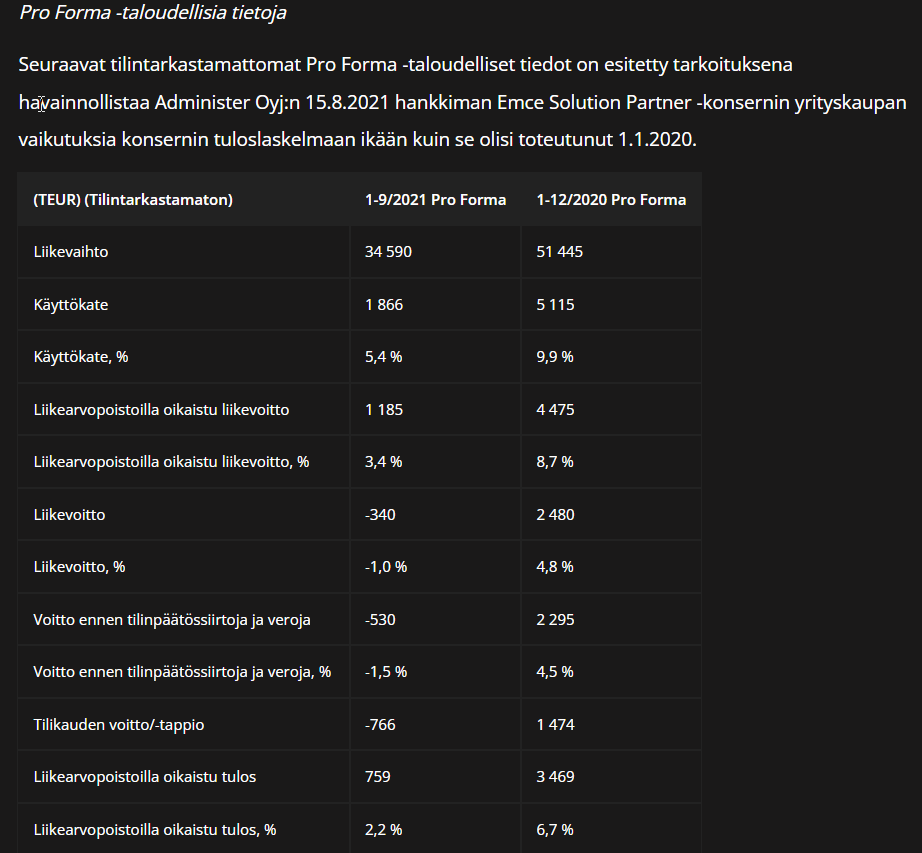

Considering the acquisition of Emce (2021-08), the pro forma 2020 revenue would have been approx. 51 MEUR.

Earnings are on a downward trend, although usually before an IPO there’s talk about earnings being somewhat “pumped,” but who knows in this case.

Administer’s financial targets for the strategy period are as follows:

Administer achieves a revenue of 84 million euros in 2024; and Administer achieves an EBITDA of 24 percent in 2024. According to the dividend policy confirmed by the Company’s Board of Directors, the Company aims to distribute at least 30 percent of its profit adjusted for goodwill amortization as annual dividends.During 2022, Administer aims to continue growth investments as well as organic and inorganic growth. The company aims to make 5–10 acquisitions during 2022. The company’s financial targets for 2022 are:

Achieve a revenue of at least 51 million euros; and achieve an EBITDA margin of at least 8 percent.

Administer estimates that the revenue and result for the financial year ending December 31, 2021, will be weaker than for the financial year ended December 31, 2020.

Administer aims to raise gross proceeds of approximately 11 million euros through the Initial Public Offering, which are intended to be used primarily to implement and support Administer’s growth strategy.

Ilmarinen Mutual Pension Insurance Company, Elo Mutual Pension Insurance Company, Aurator Asset Management Ltd, and certain other professional investors have each separately committed, under certain conditions, to participate in the Offering and subscribe for shares for a total of 12.6 million euros, provided that the valuation of the Company’s entire share capital before the proceeds from the Offering is at most 55 million euros.

https://www.administer.fi/tietoa-meista/administer-yrityksena/