Sitowise Considers Initial Public Offering and Listing on Nasdaq Helsinki.

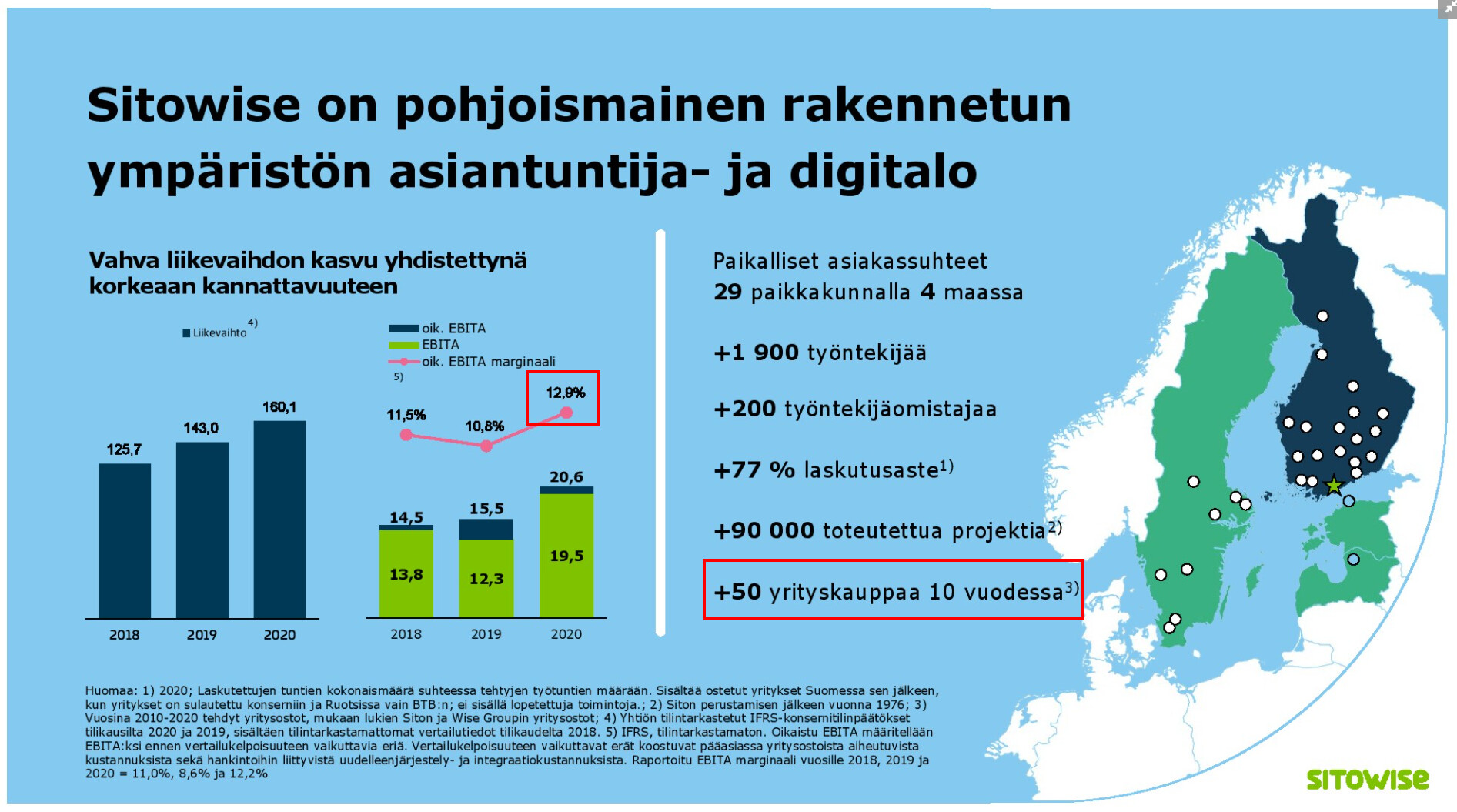

Sitowise, an expert and digital company in the built environment, is planning to list on the Nasdaq Helsinki stock exchange. Sitowise employs over 1,900 experts from various fields whose task is to design more sustainable and smarter living environments.

The company, which has grown rapidly and profitably in recent years, currently operates in Finland, Sweden, Estonia, and Latvia. The aim of the planned IPO is to support the implementation of the company’s growth strategy.

The planned IPO is expected to consist of a share issue by the Company of approximately EUR 75 million (gross proceeds) and a share sale in which certain Sitowise shareholders will sell their shares.

The proceeds from the share issue are intended to be used to repay Sitowise’s current debts and to support its growth strategy, including financing acquisitions.

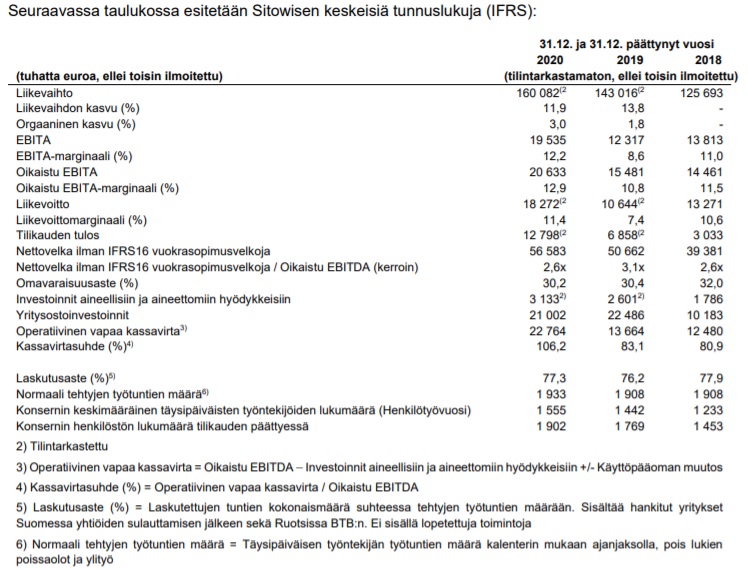

The Group’s net sales in 2020 were approximately EUR 160 million and the Company employs over 1,900 experts. Sitowise has strong employee ownership; in addition to its largest owner Intera Fund III Ky, the Company has over 200 employee-owners.

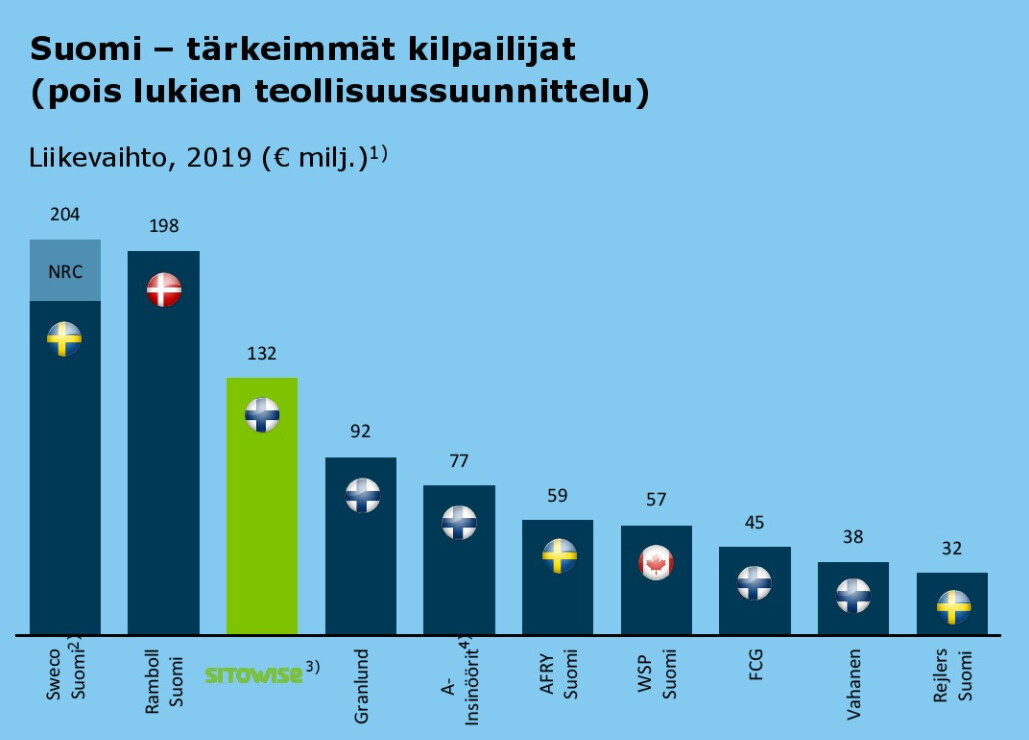

The Company offers consulting services for projects of various sizes and is involved in over 10,000 projects annually.

Sitowise has grown strongly both organically and through acquisitions. The Company’s net sales grew by an average of 12.9 percent per year between 2018 and 2020. At the same time, Sitowise has been able to maintain high profitability: its adjusted EBITA margin was 10–13 percent between 2018 and 2020, and during the same period, the operating profit margin was 7–11 percent.

Sitowise’s revenue and adjusted EBITA margin development, along with low capital expenditures, have led to a strong operating cash flow, reflected by a strong cash conversion ratio of over 80 percent between 2018 and 2020. A strong cash conversion ratio, in turn, creates good conditions for continued strong growth, acquisitions, and/or dividend distribution.

Sitowise’s Board of Directors has set the following financial targets for Sitowise in connection with the planned listing:

• Growth: Annual revenue growth of over 10 percent, including acquisitions;

• Profitability: Adjusted EBITA margin of at least 12 percent;

• Indebtedness: Net debt to adjusted EBITDA ratio of no more than 2.5x, except temporarily in connection with acquisitions

• Dividend policy: Sitowise aims to distribute 30–50 percent of its net profit as dividends.

Sitowise’s net sales for the financial year ended December 31, 2020, were approximately EUR 160 million, and adjusted EBITA was approximately EUR 20.6 million, corresponding to an adjusted EBITA margin of approximately 12.9 percent.

“Sitowise Press Release”