Admicom has been on a rally now. Last week the stock cost 15.5, now almost 18e. Today the price is up 3.5%, yesterday probably 5% and at the end of last week similar gains.

What’s driving it up now? I’ve been on board since the IPO + immediately bought more. I probably won’t lighten my position yet.

The odds are getting so good that I think the stock will take a breather for a while. Admicom is one of those companies that I would gladly add to my portfolio if the stock happened to dip badly, depending on the reason, of course.

What’s really fascinating about the company is that customer churn is very minimal, meaning customers have a high barrier to switching service providers. And as the company conquers its target markets, the market environment becomes even less attractive to potential new competitors.

What risks do you see for Admicom in the short-to-long term? Or what would be the biggest/most likely risk? I would imagine the biggest risk to be the company’s potential failure to expand into new areas and target markets. Perhaps venturing into unknown waters with new products, e.g., abroad, and making mistakes there. The current market environment is so limited, so business expansion might be quite possible at some point. But fundamentally, I do believe the company will probably make the right choices regarding potential expansions, judging by its track record.

What if there was a recession and many of Admicom’s customers saw their results decline, what would happen with these billings…

Net profit at the end of the third quarter was EUR 2,436 thousand (1,530).

53% of new sales in the third quarter came from the medium-sized segment, divided into building services technology 39%, construction 49% and industry 12%.

The revenue growth forecast for 2018 in the half-year report was 32-36%. We are refining this forecast to be between 38% and 40%. Due to the increased revenue forecast, we also predict that the 2018 EBITDA will end up between 41-43% (three-year target level 30-40%).

This may be a futile wish, but I hope investors don’t burst this bubble in their excitement. Admicom also has its price tag. It will be a more even investment story if all the good isn’t priced in immediately in the first year on the lists.

Greetings again. Although I’ve been quiet for a while, nothing stopped me from reading Admicom’s half-year and full-year reports.

They certainly put up strong numbers, but the valuation is starting to feel pretty high no matter how you look at it. In Petri’s interview, it “grated” on my ears that the company is valued on the high side even compared to other global SaaS companies. And we know that even the big players in the industry aren’t exactly cheap.

Hopefully, this case isn’t a bubble. We’ll see how it goes (heh…SaaS). Maybe the stock price will stabilize now. Time will tell.

I was thinking that if you’re anxious about not having gotten on this train, Efecte could also be a potential option to pour more money into. But that’s a topic for a different thread

When a stock has risen 140% before the end of its first year on the stock exchange, one could easily assume that it is overvalued. But when looking at Admicom’s growth rate and the scalability of its profitability, I believe the current valuation can easily be justified.

Admicom’s revenue is growing at a rate of 40% and its profit at over 50% (this year approximately +70%), and the current valuation, with an assumed EPS of 0.80, is P/E 30. For example, Revenio is currently valued at P/E 42, and Admicom’s growth rate is significantly higher than Revenio’s. Revenio, of course, has better liquidity and a larger size on its side, but both of these aspects will gradually improve as Admicom’s story progresses. Another good comparable is the Swedish Fortnox, which is currently valued at P/E 46 and is probably also why many Swedes have recently invested in Admicom.

I personally like to use Peter Lynch’s PEG ratio to assess whether a stock is overpriced. Based on the PEG ratio, I believe Admicom still has a huge upside before it can be considered an overpriced stock.

The most significant risk related to Admicom, in my opinion, is the failure of future internationalization, as Finland will become too small relatively quickly with a high growth rate. However, this risk is not yet relevant for many years.

There’s no sense in comparing it to Revenio. They’re completely different companies, and Revenio has the security of technology, patents, and years-long regulatory assessments for new products. Admicom has nothing that competitors couldn’t implement if they wanted to. Things have gone quite well so far, but in the future, it could be entirely different. Especially growth is by no means certain, so yes, this is expensive.

I assume you’re buying at these prices, given how positive you are?

I’m a little afraid of the peak of the cycle. And we’re probably right there. Since Admicom’s customers are in the construction industry, that cyclicality is a tough spot for Admicom as well. Given that, Admicom has already been given pretty strong credit. I’ll probably lighten up myself starting next week. I won’t sell everything because I still want to see the internationalization and new product situation with a small stake.

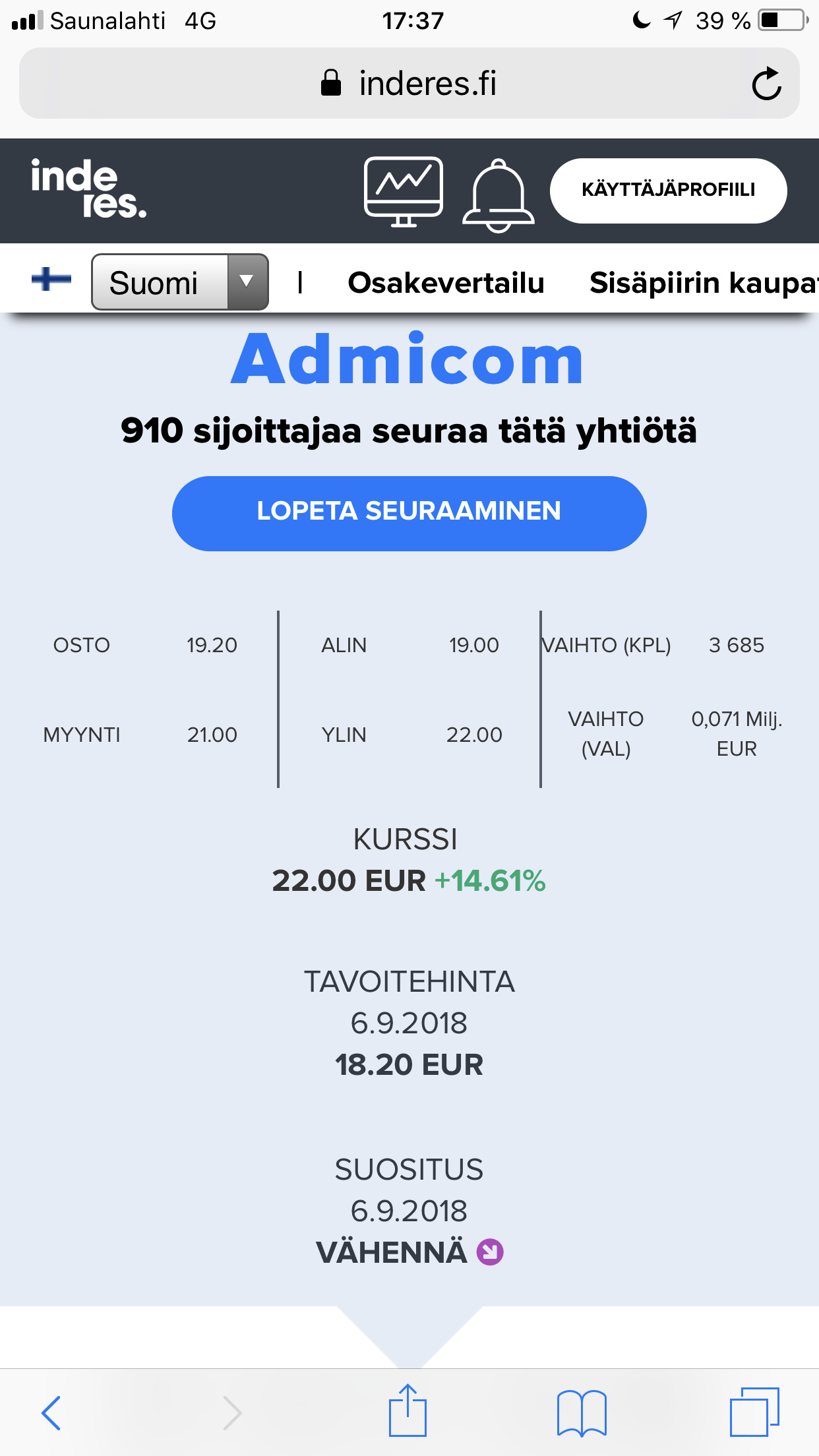

New target price 23.0e (previous was probably 18.2e). The company report will be published in the next few hours. Such a significant increase provides good support for the current price.

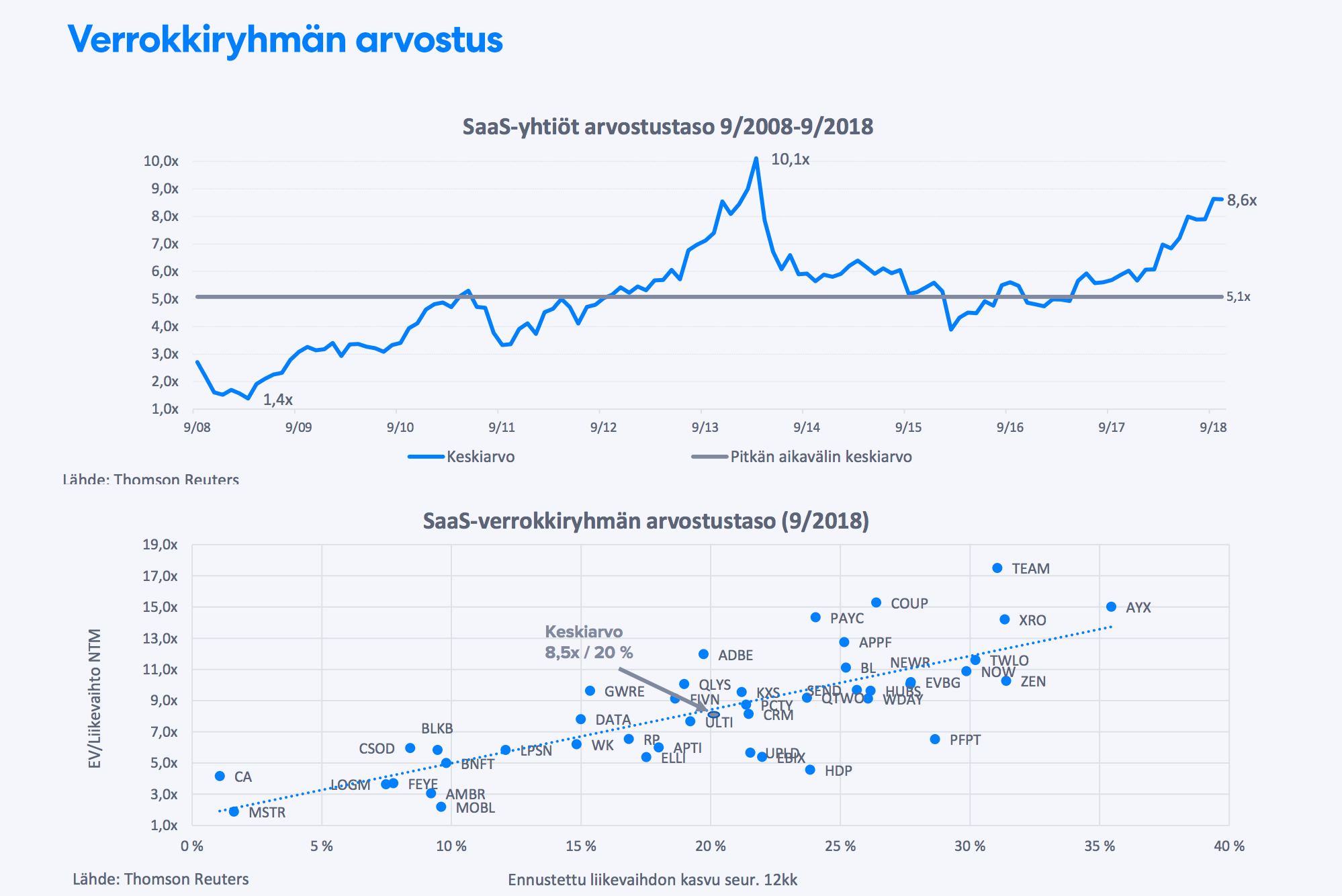

It’s interesting how the pricing of the entire industry has fluctuated between 1.4x-10.1x in the last 10 years. In efficient markets, it has been difficult to decide how much to front-run in stocks.

Revenue exceeds the forecast, but EBITDA is estimated to be in line with the previous forecast.

A bit of a murky positive - if it’s even positive at all

Well, it’s good that it’s not negative after all

Note that the operating profit margin % is estimated to remain at the same level relative to this new revenue guidance of 41-43%, meaning that the operating profit has also grown along with revenue.