The Sarastia plan is indeed interesting to hear about; it brings a massive headcount, and the business serves public sector operators. If methods other than staff reductions are seriously proposed to improve profitability, I would take those claims with a grain of salt. In Sarastia’s client field, future tenders involve risks because winning is difficult without competing on price.

From the outside, it is easy to think that Administer has made these moves post-IPO just to be a big player because it’s nice to be big. For example, Econia is effectively a staffing agency, and due to its large size, Administer gained a very cyclical piece in its package, whose weak performance has been a drag (dead weight) on the rest of the group. In other words, a major sideline.

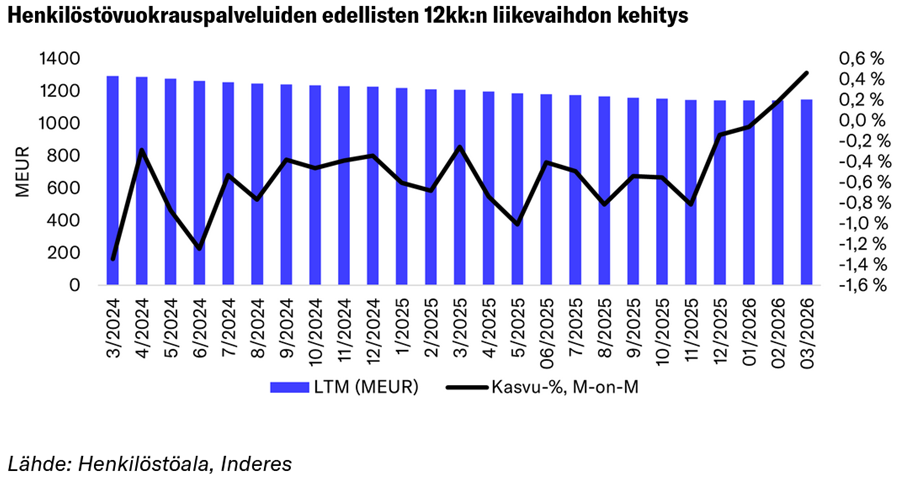

Consequently, one would expect the turnaround of Econia to show up strongly in the figures, if such a turnaround is to happen. In its morning newsletters, Inderes publishes staffing industry revenue statistics (e.g., related to Eezy analysis), which, after a long slump, has shown signs of a turnaround at the turn of 2025-26. Interestingly, in Atte’s Q1 forecast, the development is -10%, meaning the early part of the year would have gone significantly worse than the rest of the market. Econia’s top-line development has been roughly in that -10% range for the past few quarters; we will soon see if they have truly been left behind ![]()