UNH on yksi maailman johtavista terveydenhuoltoyhtiöistä, markkina-arvoltaan ~240 miljardia USD.

Yhtiö tarjoaa vakuutuspalveluja (UnitedHealthcare) ja terveydenhoidon digiyksikköä (Optum), ja kattaa reilusti yli 100 miljoonaa asiakasta ympäri maailman. Lisäksi työntekijöitäkin UNH:lla on noin 400 000.

Miksi kurssi on laskenut?

UNH on laskenut todella roimasti vuoden aikana – osake on tullut huipulta 625$ —> 265$

Keskeisimmät syyt:

Oikaistu osakekohtainen tulos 2Q25 oli 4,08 dollaria, mikä jäi konsensusennusteesta 4,48 dollarista 8,9 %

Osakkeen pulkkamäki saa tietenkin kysymään onko tarjolla ostopaikka. Lähtökohtaisesti tämä on itselleni liian iso,liian ”old school”,liian vaikeasti ymmärrettävä ja politiikalle altis. Luen kyllä erittäin mielelläni jos jollain on kykyä analysoida tätä syvällisesti.

Buffettin ostot nosti UNH:n jälkipörssissä ylös, mutta myös ”Big Short” -mies Michael Burry on kyydissä. Se nappas call-optioita noin 350 000 osakkeeseen ja osti suoraan reilut 20 000 osaketta.

Aika selkeä veto sen suuntaan, että tästä tulee vielä nousua, vaikka kurssi on ollut tänä vuonna vastatuulessa.

Nyt samaan veneeseen hyppäs sekä Buffett että Burry – ei ihan jokapäiväinen näky.

Ihan hyvä, joskin myyntihenkinen (paid talk, exit pump, tms?) esittely firmasta. Stephanie Nivenin firmalla hyvin pieni possa UNH:ssa, mutta Stephanie ilmeisesti seurannut/holdannut firmaa 2012-13 lähtien.

Kyllähän kun tuota firmaa tutkii, niin ellei DOJ:lta tule jotain ihan älytöntä pommia, niin on aika hiton solidi bines.

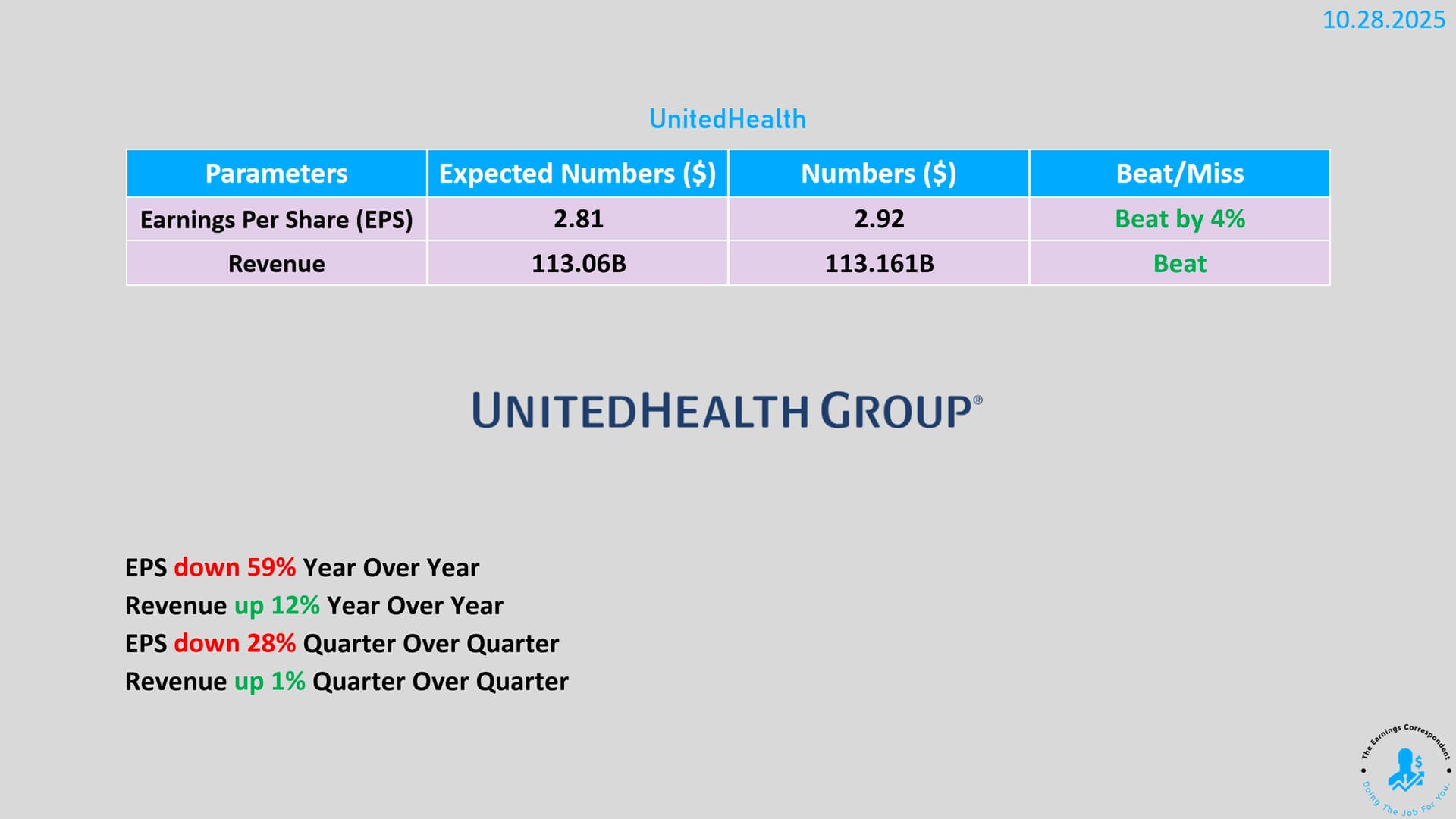

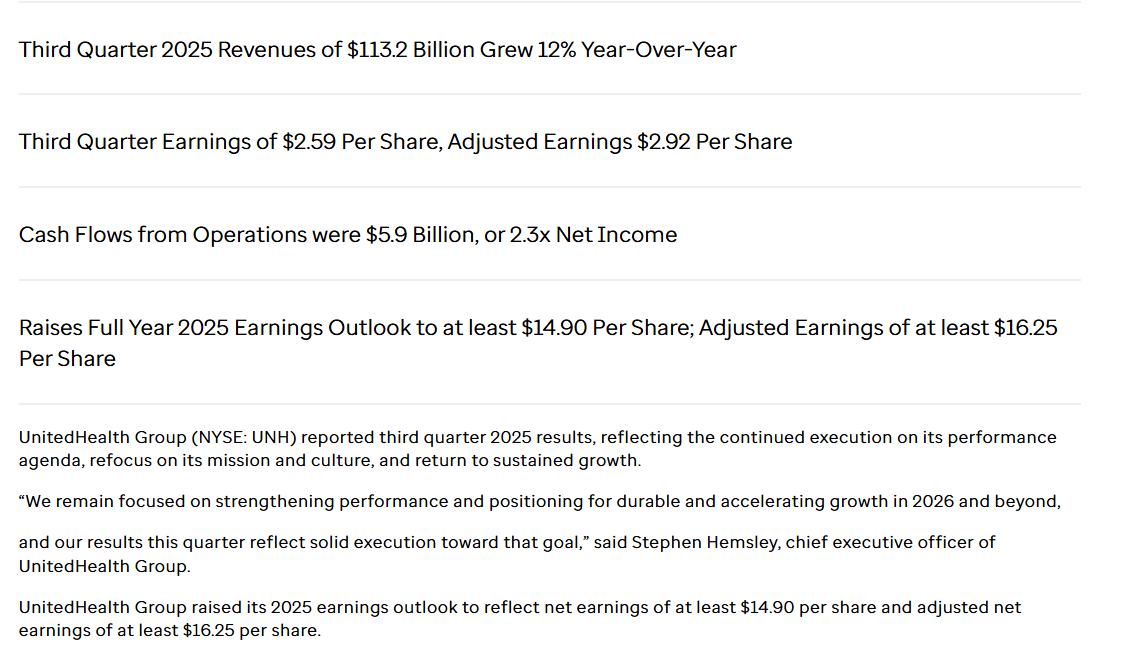

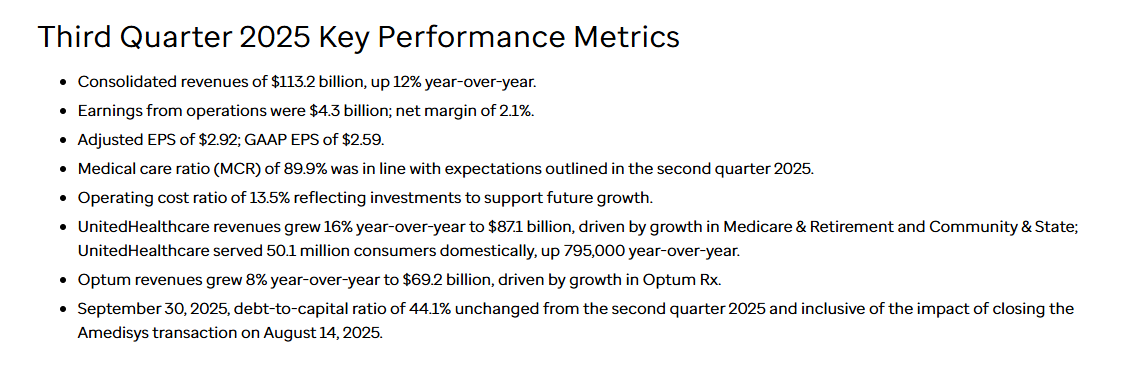

UnitedHealth rapsas kasvua liikevaihdossa, lisäksi myös EPS ylitti odotukset. Koko vuoden ohjeistusta on myös nostettu, mikä lupaa hyvää tulevan kannalta.

Liiketoiminnan eri segmenteillä meni hyvin esim. vakuutuspuolella jäsenmäärät kasvavat ja apteekkiliiketoiminta vetää erityisen hyvin. Haasteita sen sijaan aiheuttavat kustannuspaineet, mutta toisaalta yhtiö korosti olevansa valmis nopeampaan kasvuun tulevina vuosina.

Alla olevan jutun mukaan UnitedHealth lopettaa noin miljoonan Medicare Advantage -jäsenen sopimukset, koska kiristyneet korvaukset, kasvavat kulut ja tiukempi valvonta ovat tehneet osasta yhtiön asiakkaista ilmeisesti liian kalliita. Kyse on siis strategisesta vetäytymisestä eikä mitenkään yksittäisestä virheliikkeestä.

Tämä tarkoittaa sitä, että moni iäkäs jäsen joutuu nyt etsimään uutta vakuutusta ja huomaamaan, miten lisäedut niukkenevat ja lääkäriverkostot kapenevat. Samalla tässä yhteydessä paljastuu, kuinka herkästi suuret vakuutusyhtiöt voivat muuttaa pelisääntöjä omien marginaaliensa turvaamiseksi.

The UnitedHealth retrenchment is not just a story about one company, it is a stress test for the entire Medicare Advantage model. For years, private plans have grown on the promise that they could deliver richer benefits at lower cost than traditional Medicare, in part by managing care more tightly. Now, as payment formulas tighten and oversight increases, the trade offs are becoming more visible. The report that describes how UnitedHealth Cuts 1 Million Seniors in the Largest Medicare Purge in 20 Years notes that this is part of a broader period of contraction for the industry, not an isolated blip.

UnitedHealth Group has agreed to sell its last South American business Banmedica to Brazilian private equity group Patria Investments for $1 billion, two sources with knowledge of the matter said on Sunday.

The final agreement was signed on Saturday and an announcement is expected on Monday, the sources added, asking for anonymity to disclose private talks.

UnitedHealth has been trying to exit Latin America since 2022 and had previously sold its businesses in Brazil and Peru.

The sale of Banmedica, which currently operates in Colombia and Chile, has been under discussion for almost a year.

Patria and UnitedHealth did not immediately reply to requests for comment on Sunday. Banmedica had 1.7 million health insurance plan members, seven hospitals and 47 medical centers as of June, after its divestment from Peru.

The exit from the region reduces one more distraction from the turnaround efforts led by CEO Stephen Hemsley. UnitedHealth, a member of the Dow Jones Industrial Average, raised its annual profit forecast in October and said it aims for a return to growth in 2026 that should accelerate in 2027.

Hemsley returned as CEO in May after leading the company from 2006 to 2017 and has been working to regain investor and consumer trust after a difficult period for UnitedHealth that included the murder of a top executive, an unexpected surge in medical costs and a federal probe.

He was brought in as a part of a management shakeup after the company’s first earnings miss in over a decade in April.

UnitedHealth booked an $8.3 billion loss last year related to the sale of its South American operations, $7.1 billion stemming from the Brazil exit and $1.2 billion from Banmedica.

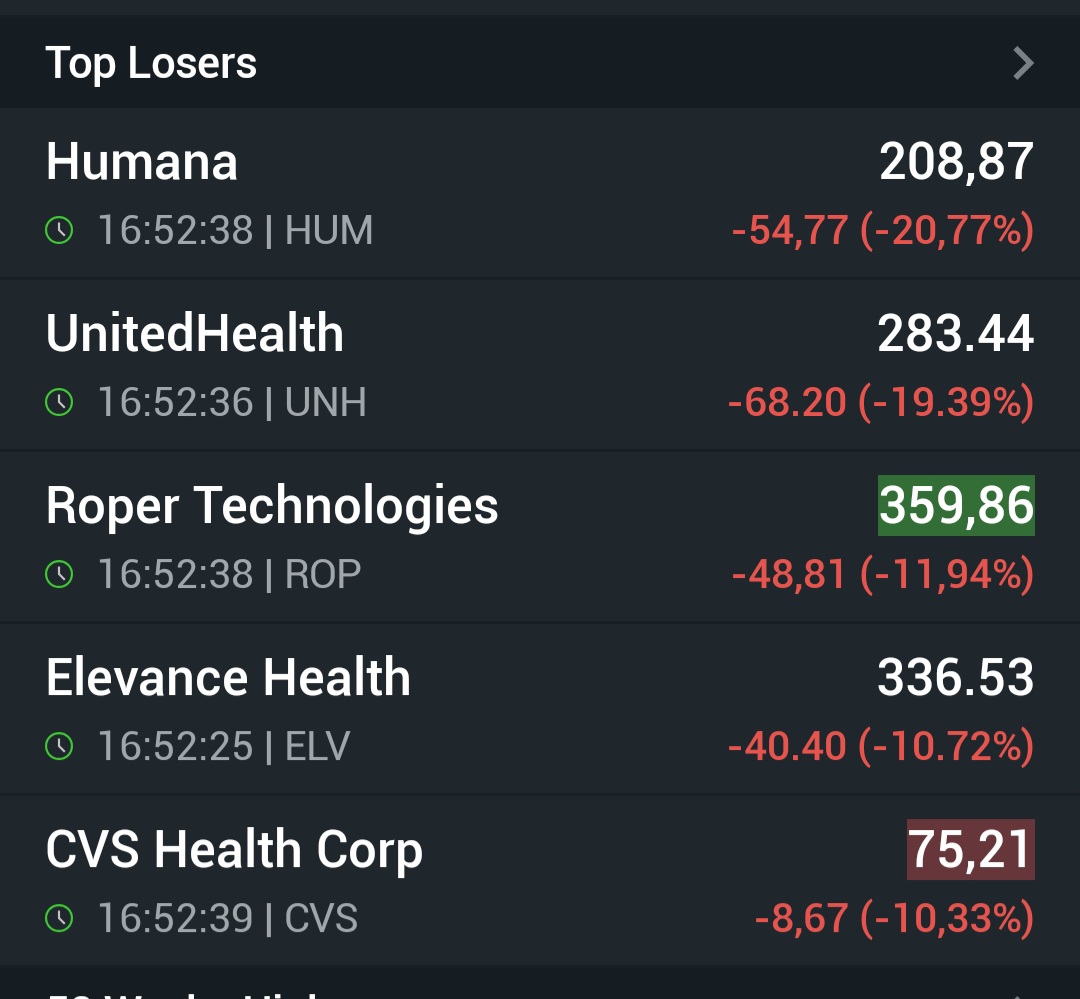

Jan 26 (Reuters) - The U.S. has proposed an average rate increase of 0.09% in payments to private insurers next year for the Medicare Advantage plans they manage, the government said on Monday, driving shares of the companies down more than 10%.

Shares of health insurers UnitedHealth (UNH.N), CVS Health (CVS.N) and Humana (HUM.N) were down between 8% and 13% in after-hours trading, while shares of Elevance Health (ELV.N), Centene (CNC.N) and Molina Healthcare (MOH.N) were down nearly 5%.

Trump selvästi haluaa ettei terveysvakuutusmaksut nousisi. Tämä vaikuttaisi vakuuttajien katteisiin luonnollisesti. Olemme nähneet että katteet on ollut paineessa ja alhaiset historiaan nähden. Vaikea sanoa mitä Trump lopulta ajaa, mutta itse luulen että hän ottaa tämän vaaliaseekseen. Voi olla että joku parempi diili vielä saadaan, mutta reiluja korotuksia tuskin nähdään vaalien takia. Tämä on taistelu jonka hän voi voittaa toisin kuin Gröönlannin valloitus.

Edit: Lisätään vielä että nollakatteet ei ole kestävä tilanne. Voisi luulla että jos hintaa ei voi nostaa, tulee karsia osa väestöstä pois vakuutuksen piiristä tai tehostaa omaa tekemistä esim. AI:lla ja laittaa omaa väkeä pihalle.

Liikevaihto kasvoi noin 12%. Tulos heikko. Ohjestus ihan ok imo.

Full Year 2025 Revenues of $447.6 Billion Grew 12% Year-Over-Year; Earnings of $13.23 Per Share; Adjusted Earnings of $16.35 Per Share

Full Year 2026 Revenue Outlook Greater Than $439.0 Billion; Earnings Outlook Greater Than $17.10 Per Share; Adjusted Earnings Greater Than $17.75 Per Share

Kun katsotaan Q4 nettotulosta niin se jäi $10M plussalle. Kuulitte oikein eli UNH teki liikevaihtoa kvartaalilla $113 215M eli reilu 113miljardia ja viivan alle jäi 10miljoonaa. Kun katsotaan tulosta ennen veroja niin se oli jopa 720 miljoonaa pakkasella. Ei ihme että premarket näyttää reilua laskua. Tähän kun vielä otetaan huomioon Trumpin uhkailut niin varmasti heikoimmat terveysvakuuttajat uhkaa kaatua jos tällaista jatketaan pidempään. Harkitsen että laitan oman UNH position laitaan ja katson myöhemmin uutta mahdollista ostoa alempaa. En välttämättä näin kuitenkaan tee. Riippuu hinnasta…

Vakuutusyhtiöt ei ole pitkään enää onnistuneet kasvattamaan asiakaskuntaansa vaan tuloskasvu tulee vain jatkuvista hintojen korotuksista. Hyvä nyt nähdä ettei piikki ole loputtomiin auki. USAN epätehokkaan ja epäoikeudenmukaisen terveydenhuoltojärjestelmän on aika disruptoitua.

Onneksi en luopunut UNH positiosta sillä nyt näkyy selvästi valoa jo tunnelin päässä. Aiemmin muutama viikko sitten saimme tietää että korotuksia tulee enemmän mitä odotettiin.

The Trump administration announced a 2.48% payment increase for Medicare Advantage plans for 2027 – a much bigger boost than an earlier proposal that essentially kept rates flat.

Tänään UNH raportoi tuloksen. Jättimäinen tulosylitys. Tämän vuoksi osake pomppaa avauksessa ja nyt voi jo sanoa melko isolla varmuudella että pohjat on takana.

The company brought in revenue of $111.7 billion in the first quarter, up 1.9% from $109.6 billion in the same period a year ago and against a FactSet estimate of $109.4 billion. Adjusted earnings per share came in at $7.23, beating the FactSet consensus of $6.58.

The margin of the bottom-line beat was the widest since the first quarter of 2021, according to FactSet data.

Jonkunlainen posari tämä kai myös on: Expects adjusted earnings per share of at least $18.25 for the year, compared with the $17.75 it guided for last quarter, and the current average analyst estimate compiled by FactSet of $17.86.

Kai tämä vaan kannattaisi jättää ikiholdiin kun kerran sai alta $300 poimittua ja tulevaisuus näyttää taas paljon paremmalta. Ei markkina olisi tarjoillut tällaista ostopaikkaa jos kaikki olisi ollut selvää eikä epävarmuudesta olisi ollut tietoakaan.