UB is pretty cool.

Ruoholahti proletarian Sauli has produced a comprehensive report on United Bankers, and like other comprehensive reports, it is available for everyone to read and there are no paywalls ![]()

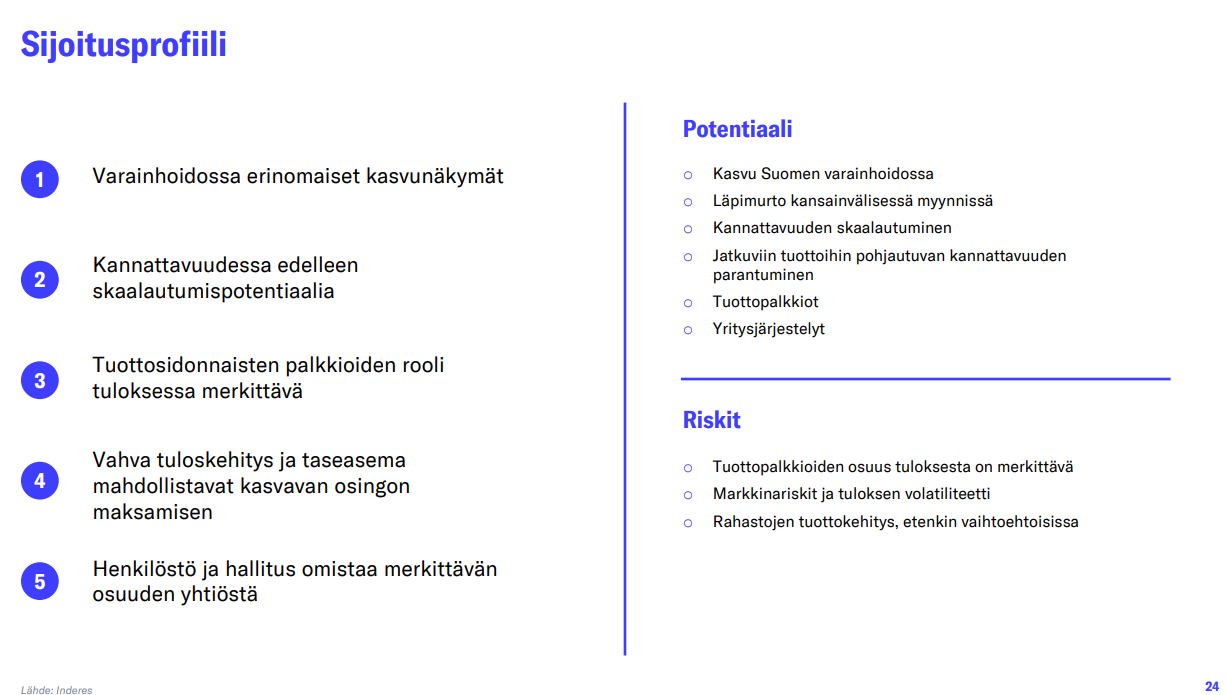

UB’s investment story has improved significantly in recent years, and it has emerged as a high-quality asset manager. We believe the longer-term earnings growth outlook is very good, but in the short term, the challenging market situation for alternatives is throwing a wrench in the works. Without brisk earnings growth, the stock has no upside, but if forecasts materialize, the expected return is good. We want to see concrete signs of accelerating earnings growth and reiterate our Reduce recommendation with a target price of EUR 19.0 (prev. EUR 18.0).

Quotes from the report:

Still potential in scalability

Due to the fixed cost structure, the operating leverage of the business is significant, which has been reflected in Asset Management’s figures in recent years: from 2018 to 2024, approximately 50% of the growth in Asset Management’s revenue has flowed through to EBITDA. We believe this level is reasonable but clearly pales in comparison to the sector’s top companies, where operating leverage has consistently been between 70% and 100%. The company’s fixed costs have increased continuously as it has expanded its product offering and grown its sales force. The company should therefore have the potential to raise its Asset Management profitability significantly from current levels, especially if performance fees remain at a high level. We believe this higher operating leverage is realistic over a couple of years as the company’s sales accelerate from current levels and the growth investments currently being made are completed.