I consider the patent dispute initiated by First Solar to be the single biggest risk in TOYO’s investment case at the moment.

First Solar filed a complaint in February 2026, which led the U.S. International Trade Commission (USITC) to launch an official Section 337 investigation in March 2026, titled Certain TOPCon Solar Cells, Modules, Panels, Components Thereof (Inv. No. 337-TA-1494). The respondents include, among others, TOYO Co., Ltd., TOYO Solar Texas LLC, and VSUN Solar USA.

First Solar alleges that the respondents’ products based on TOPCon technology infringe upon its patents and is primarily seeking a so-called General Exclusion Order (GEO). If granted, this would be a highly significant ruling, as it could prevent the import of all TOPCon products deemed to infringe on these patents into the United States, regardless of the manufacturer. Alternatively, First Solar is seeking a more limited exclusion order as well as cease-and-desist orders against the respondents.

As of now, no ruling has been issued in the case, and the USITC has not taken a stance on the substance of the allegations. TOYO’s products continue to be imported into the United States normally.

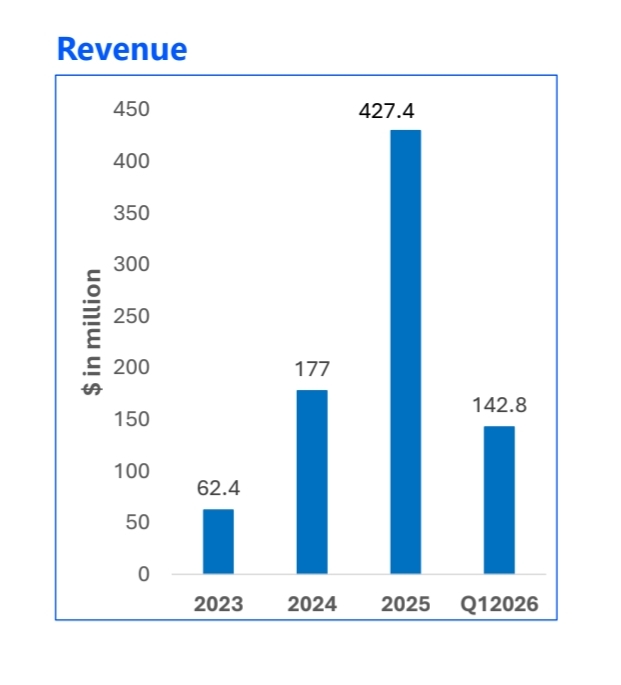

The risk to TOYO is significant, as approximately 80% of the company’s revenue comes from the United States. Although the factory located in Texas assembles modules locally, the cells are still imported from Vietnam and Ethiopia. A potential import ban would target these very cells, so the current production model does not offer protection against this risk.

What makes the situation particularly interesting is that First Solar itself does not use TOPCon technology at all. The company’s own technology is based on CdTe thin-film cells, but it has acquired TOPCon patents through acquisitions and is now using them against its competitors.

This is not the first patent dispute surrounding TOYO. JinkoSolar challenged the TOYO–VSUN–Abalance group regarding TOPCon patents back in December 2024, but the parties reached a settlement at the end of 2025, and the lawsuits were withdrawn in early 2026.

In my own view, however, a complete GEO ruling is unlikely. TOPCon is currently the world’s leading solar cell technology, and a general import ban would affect a significant portion of U.S. panel imports. More likely alternatives could be a settlement, licensing agreements, challenging the patents, or a more limited order concerning only certain operators.

Section 337 cases typically last about 16–18 months, so a decision is estimated to arrive in late 2027. Interestingly, at the same time, TOYO is pursuing an HJT cell factory in Houston. This may turn out to be a strategically very important move, as HJT is a different cell structure and does not fall under the scope of the TOPCon patents. If patent risks regarding TOPCon increase, the HJT factory could effectively serve as an insurance policy for TOYO against this very scenario.