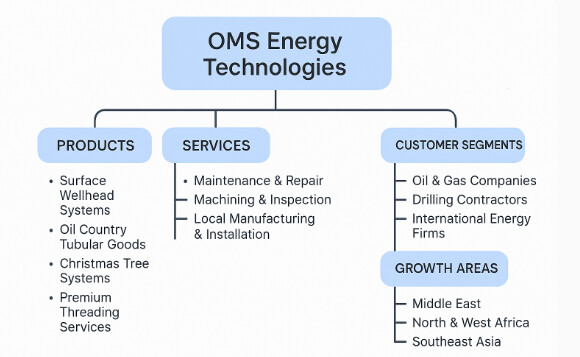

This is an interesting company story. Oms Energy Technologies was founded in 1972 and manufactures pipe fittings, connectors, etc., for the oil industry. Their headquarters are in Singapore, and they have operations in Saudi Arabia, Singapore, Malaysia, Thailand, and Indonesia.

The company’s business includes selling pipelines and fittings, as well as their installation, maintenance, repair, and inspection activities.

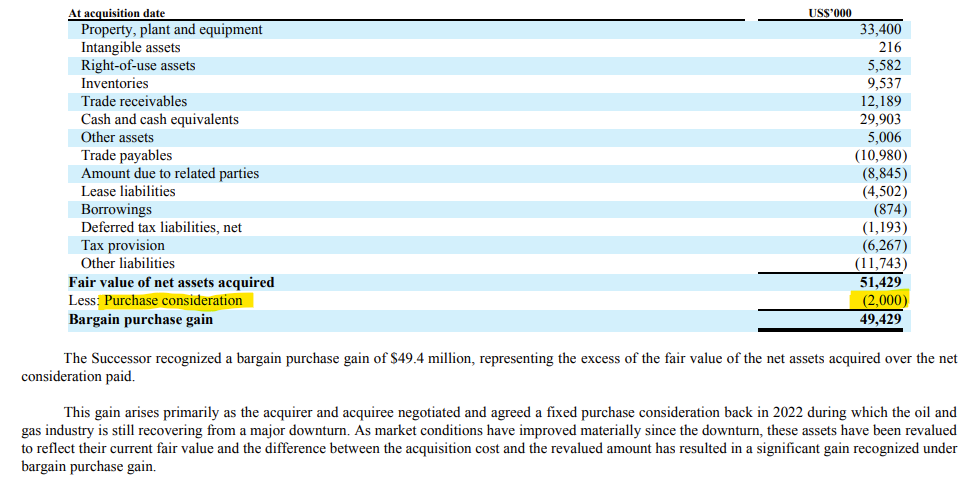

The company’s current management bought it from the Japanese Sumitomo Corporation for $2 million in 1/2023. The new owners listed it on the stock exchange on May 13, 2025, and in the offering, 3,703,704 new shares were sold to investors at a price of $9 per share. The total number of shares is currently 42.45 million.

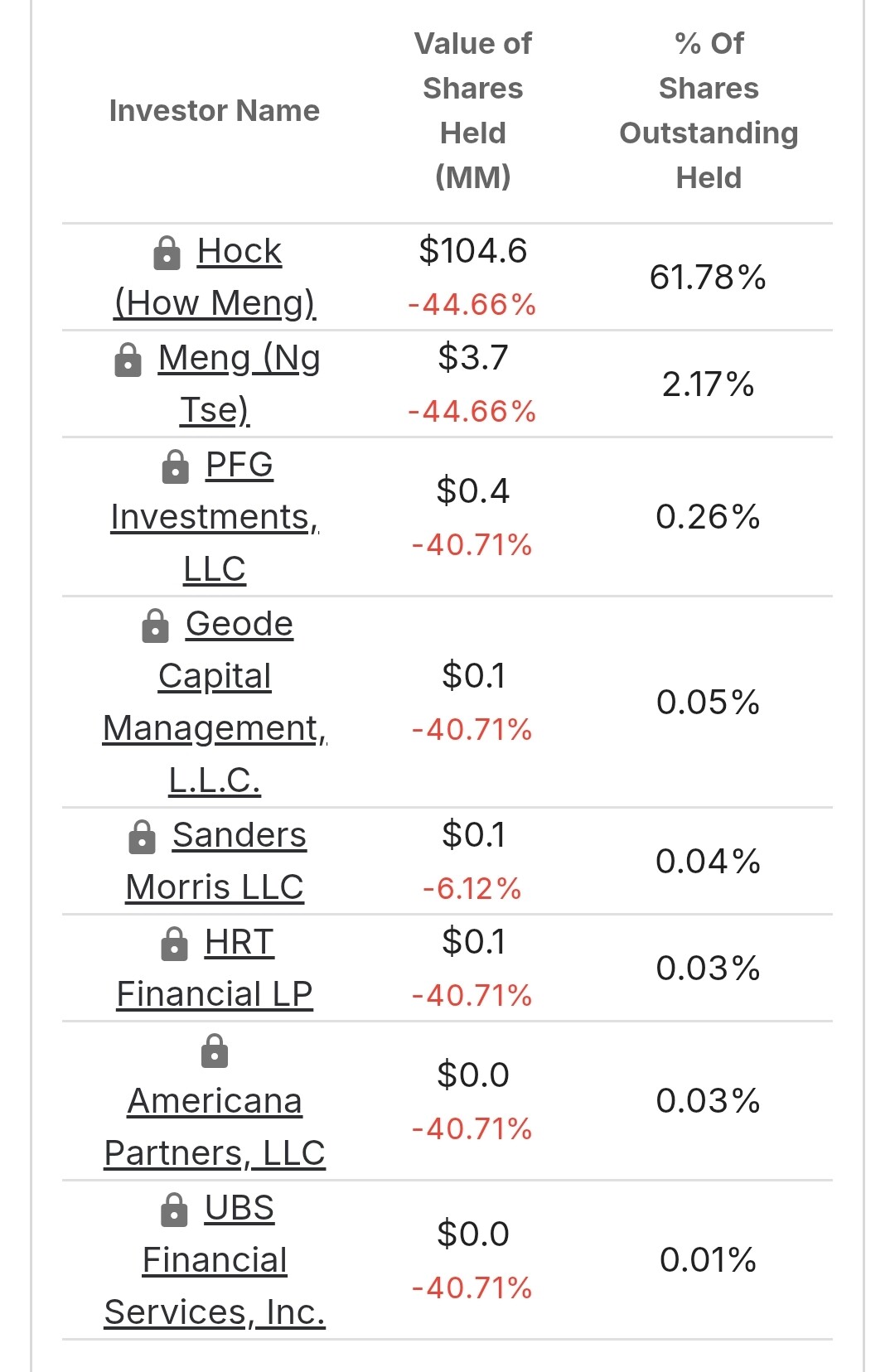

The company has grown rapidly over the past few years and has been very profitable. The current CEO owns 61%, and in my opinion, institutional investors have not yet discovered it.

What makes this interesting, in my opinion, is that the company signed a 10-year agreement with Saudi Aramco in January 2024, which will bring in $120-200 million in annual sales. So, the company’s cyclical business is well protected thanks to this deal.

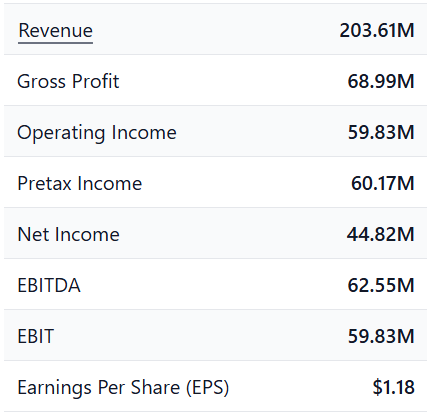

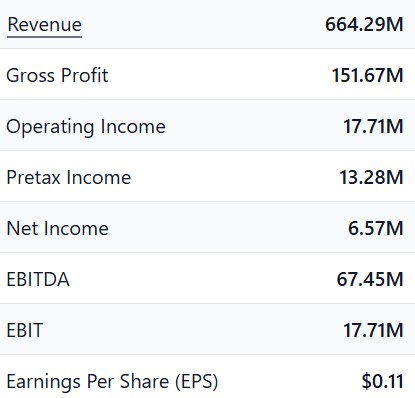

In addition, the company’s net cash is approximately $2.25 per share, and EPS should be around $1 per year for the coming years. The share price at the time of writing is $3.58.

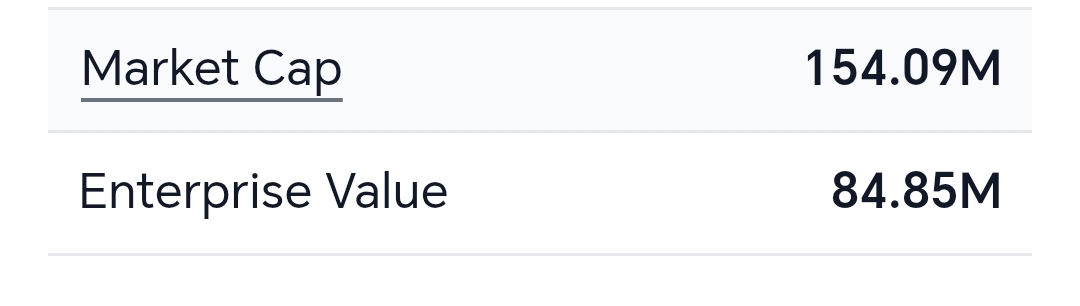

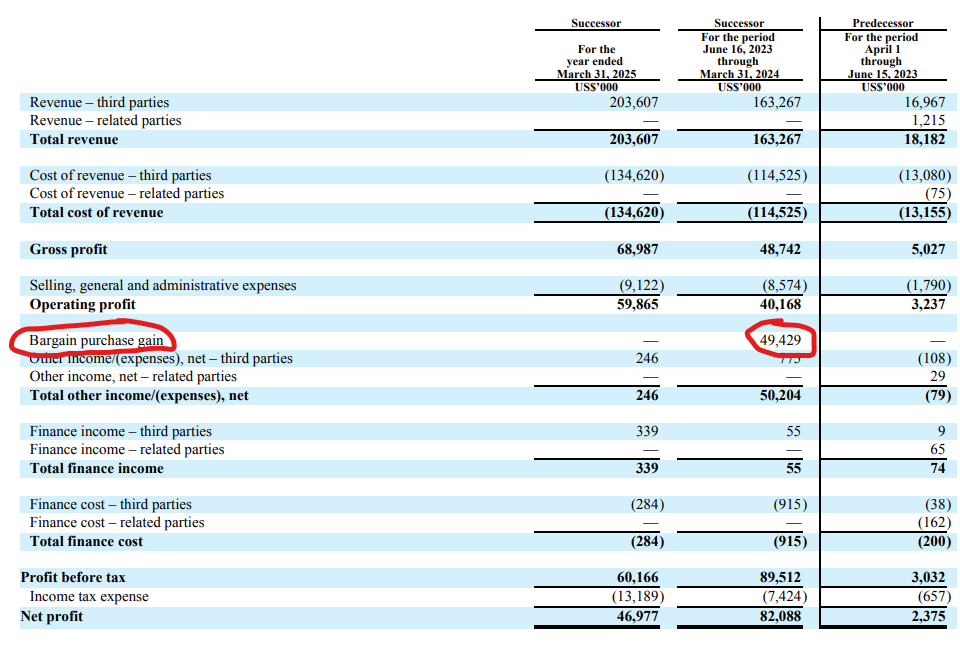

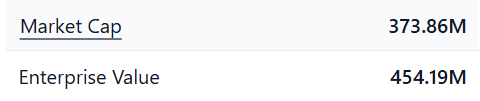

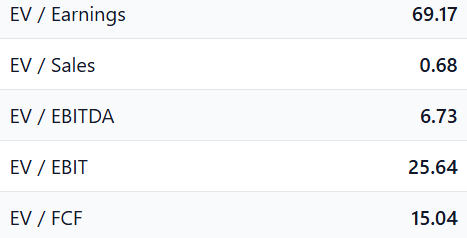

Then the best parts, the numbers. Note that the ratios below will change slightly once the $33.3 million from the IPO is reflected in the balance sheet.

So, the company’s financial year indeed ended in 3/2025, i.e., before the IPO. The company has not published an interim report since then, so the IPO will bring in approx. 33m to the cash, meaning the EV after that is approx. 50m. The numbers above are from the balance sheet, before the IPO.

The company apparently publishes its results twice a year, according to Singaporean rules.

A quick glance suggests the company’s business looks very profitable and the valuation relatively low. The customer risk with Aramco is high, but on the other hand, becoming their preferred supplier is inherently a sign of competitiveness and quality.

After a brief screening of the prospectus, a question arises: why is this case available in the equity markets at such a low price? The company has sufficient cash, and the comments in the prospectus about how the IPO funds were used did not provide any clarity (general working capital, as is often the case). From a business perspective, IPO financing was not needed, and if a growth transaction is in mind, the company could obtain other financing more easily.

The company is under the control of the main owner, and in such a case, a small investor is a passenger sitting behind quite a few wagons, receiving information with a significant delay. So why did the main owner want to list a relatively small stake? Does he truly believe it will bring added value to the business and a high valuation in the future? If so, why is the quality of IR materials minimum effort? Why did Sumitomo sell this so cheaply? How did Aramco’s very long framework agreement align so well with the MBO? On the other hand, the valuation has taken quite a slide since the IPO, which, combined with the strong earnings, contributes to today’s affordability.

The company’s auditor, Marcum Asia LPA, is not a familiar entity to me. They have some news about fines, so a more well-known international auditor would increase confidence. However, the company has been under Sumitomo, which in turn adds more reliability to its past history.

Excellent questions. I also looked into the company yesterday, inspired by the opening post, and wondered about the price. The share price has halved since the IPO. Something has happened, but what? Revenue has grown, but profitability has halved. Have profits been invested in growth, or have margins suffered due to competition? Many questions and few answers. I need to continue researching today.

Extremely interesting find! I’m also wondering how something this good could be available so cheaply.

My own interpretation of Sumitomo’s departure is that How Meng Hock had his buying pants on at a turning point when the company and the sector were in a significantly worse state.

My sources for this interpretation are this news article and radio interview:

I’m puzzled by the failure of that IPO, whether it was bad luck, timing, or something else. My own speculation on the matter is that it could be due to the IPO’s timing coinciding with a tariff panic, especially since the company is Singaporean and operates in several countries, although on the other hand, I can’t think of any immediate consequences of the tariff mess for the company’s business.

If one considers the situation that we investors would hope for, namely that the company is heavily undervalued, I believe the following factors speak in its favor:

Limited coverage: the company is currently followed by two firms (according to the company’s IR pages), both of which have been involved in the IPO in one way or another.

Small size: with a market capitalization of $169 million, the company falls into the microcap category in the US.

Strong financial figures: these have already been discussed by other participants above.

As an additional thought, I’m still wondering how you see what the company’s short interest tells us? The short interest as a percentage of float is 0.42%, but on the other hand, when looking at trading volume in relation to shorts, it is relatively larger.

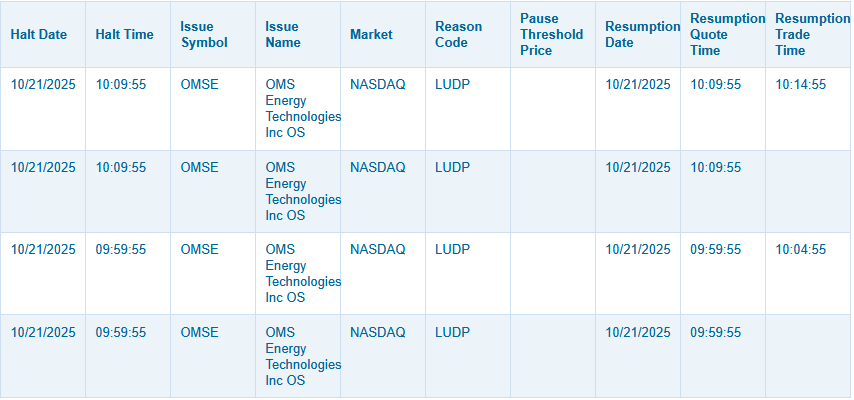

It’s been quite a hectic pace today. I couldn’t get on board because Nordea didn’t sell. I also noticed that the stock has been halted twice due to such high volatility.

Yeah, I also noticed that today might be the most traded day for the stock since its IPO. I guess this is only now starting to gain public awareness and the market will correct the “pricing error”.

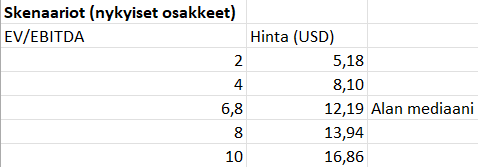

I don’t see any other catalysts for now than the rise in valuation multiples, but for example, a rise in oil prices would be a plus. My investment thesis with this is to buy quality business below its fair value. As for what its fair value is, there are as many ways to calculate it as there are calculators. My own calculations are above.

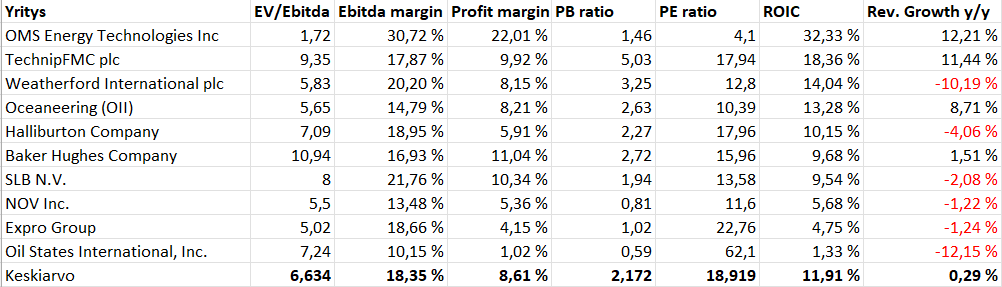

I researched its competitors a bit and found one similar company, Oil States International, Inc. (OIS), which has a similar business model and product portfolio to OMS. Oil States is valued at significantly higher multiples, even though their profitability is worse than OMS’s.

Oil States will publish its Q3/2025 results on October 31st, so then we will see which direction the oil pipeline market is heading

In their Q2/2025 earnings release, the order backlog had at least still grown: