I was just wondering last night what has been lifting Talenom all week.

3 Likes

Kinnunen has penned his thoughts on the separation of Easor: Talenom arvioi Easor-ohjelmistoliiketoiminnan eriyttämisestä itsenäiseksi pörssiyhtiöksi - Inderes

It will be interesting to see how Talenom’s story continues from here. A defensive and nicely growing accounting firm will likely act as a dividend machine. Problem areas like Sweden should just be fixed and start generating positive results.

Easor is, to my understanding, a competitor to Fortnox, for example. If the cash flow can be invested back into the business with a good return on capital, one could have quite a compounder on their hands. There would be growth potential, for example, in Spain, if market shares can be successfully gained.

But only time will tell how these companies perform separately. The track record of recent years hasn’t been very impressive, though… As separate companies, the implementation of completely different strategies should naturally

23 Likes

It’s quite quiet here and in the media regarding Easor’s listing process and what was the underlying reason for the announcement. Now, we are finally at a turning point where the company’s true value is about to be unleashed. I personally expected this to happen only in 2027, but the underlying reason seems to be Visma’s anticipated IPO in 2026.

Tallukka’s talk about Easor’s potential listing is a classic “dual-track” process, i.e., a negotiation tactic whose sole goal is to create a competitive situation and maximize the sale price in a direct sale vs. IPO. The real endpoint is redemption, not an IPO. Through an IPO, in my opinion, the company cannot implement its previous “buy and leverage” strategy, as the cash would not allow for very massive acquisitions. Also, in an IPO, the price would remain lower, as the “redemption premium” would be missed + strategic advantages from the buyer would be absent.

I divided the text into Part 1, Easor’s sale, and Part 2, what the new Talenom could look like once Easor is sold. I admit my laziness and partly ran this through Gemini, but everyone can delve deeper according to their interest, as it’s difficult to write a longer personal analysis in this message field. This only gives direction vs. complete silence around the company. This should be related to the company’s current market value of 160m and EV of approximately 253m. Everyone can then calculate what Talenom’s accounting business’s EV/EBITDA will be in 2026 when the exit is made at around 200m. I know that Juha’s task is not to speculate on acquisitions here, but the complete radio silence elsewhere is surprising. How do you, @Juha_Kinnunen, see the depreciation level of Talenom’s accounting business changing once Easor is gone?

Part 1: The Inevitable Sale of Easor – Price, Buyers, and Timeline

1. Probable Sale Price: 180–250 Million Euros

Easor’s value is not based on its current results, but on its position as a modern, scalable B2B SaaS platform.

-

Revenue (ARR): Easor’s annual recurring revenue is approximately 24 million euros.

-

Valuation Multiples: EV/Sales multiples for similar publicly listed SaaS companies currently range from 7x–8x. In private M&A transactions, high-quality ERP software has commanded multiples of up to 9x–11x.

When a strategic premium, which a buyer is willing to pay to eliminate competition and strengthen market position, is added to this, the realistic transaction price will inevitably fall between 180–250 million euros. A transaction price below 200 million would be a clear disappointment.

2. Strongest Buyer Candidates: Facing Strategic Necessity

There are several players in the bidding process, but two stand out, as for them, the deal is not just an opportunity, but a strategic necessity.

-

Visma: The Nordic market leader is preparing for its own massive IPO and wants to go public with a perfect growth story. Acquiring Easor would serve this perfectly. Although Visma has Holded in Spain, Easor is technologically more modern and better positioned for the upcoming mandatory e-invoicing reform. In its home market of Finland, Visma would neutralize a rising competitor whose licensing model for other accounting firms poses a direct threat to their ecosystem. Acquiring Easor just before its own IPO would be a chess move by Visma that would cement its position.

-

Fortnox: The undisputed market leader in Sweden, but at the same time a prisoner of its home market. Continued growth requires internationalization, and opening new markets organically is slow, expensive, and extremely risky. Easor would offer Fortnox a golden “turnkey” solution: immediate entry into both the Finnish and Spanish markets through a ready-made product, technology, and existing accounting firm network. This shortcut is so valuable that they have every reason to pay a premium price for it.

3. Time Window: Next 6–9 Months

Visma’s IPO intentions create a clear deadline for the process. If the deal is to be done, it must be done soon. This is likely the reason why “considering an IPO” came now, and not in 2027. Currently, Easor has strong campaigns like “rest of the year free” to boost user numbers.

-

Q4/2025: Official negotiations and due diligence processes begin.

-

Q1-Q2/2026: Intensive negotiations and signing of the sales agreement. I believe the deal will be announced before the summer holidays.

-

Q3/2026: Final implementation (closing) of the deal and transfer of funds to Talenom’s cash reserves.

Part 2: “The New Talenom” – How to Convert Over €100M Net Cash into Shareholder Value?

This is the core of the investment case, which has been forgotten during the stagnation of recent years. The sale of Easor is not the end of the story, but a catalyst that will trigger Talenom’s transformation back into the old growth-phase Talenom. For example, Rantalainen has implemented this very successfully and aggressively in the Nordics. Let’s assume a sale price of 200 million euros.

Phase 1: Balance Sheet Cleanup and War Chest Formation

-

Cash inflow: +200 M€

-

Debt elimination: -92.5 M€

-

Moderate dividend (e.g., €0.20/share 2025): -9.1 M€

-

Result: The company has a debt-free balance sheet and net cash of approximately 98.5 million euros.

Phase 2: Igniting the Growth Engine – Full-Throttle Capital Allocation “The New Talenom” will not sit on its cash. It will do what it does best: use its proven “value creation machine” in Finland and accelerate international growth. The company aims to utilize a 2.5x net debt/EBITDA leverage.

This means the company can use all its net cash AND take on new debt on top of future, larger EBITDA. The calculation shows that this gives the company approximately 270–280 million euros in total capital for acquisitions.

What can this capital acquire from a fragmented market?

-

Acquirable EBITDA: Assuming smaller accounting firms are acquired at a historically justified 7x EV/EBITDA multiple, this capital can acquire approximately 40 million euros in new annual EBITDA.

-

Acquirable Revenue: If the average profitability of acquisition targets is 12%, this means over 330 million euros in new revenue.

Result: The sale of Easor is not just an exit; it is fuel that transforms Talenom from its current, complex, and partly risky hybrid company into a pure, highly profitable, and stable cash-flow-generating Northern European accounting firm consolidator.

This new, clear profile and explosively grown earning capacity would eliminate the current “conglomerate discount” and justify significantly higher valuation multiples (EV/EBITDA 10x–14x). This is the path by which the company’s value can be multiplied in the coming years. When comparing the current 253m EV and the future approximately 200m Easor exit, the sum of the parts in the market is completely wrong. In Sweden, at Fortnox, the main owner First Kraft AB bought the company out with EQT, even though the pricing was not quite this far off. Now, a similar opportunity would exist in Talenom.

46 Likes

Thanks for the inspiring speculation!

I myself have also wondered about the week of silence after the announcement. Juha apparently cleared the jackpot with his comments. If it went as you suggested, this company would also get a proper wake-up call, like SSH or Bittium. Confirmation of the product’s competitiveness from a foreign entity is needed, and once the duck leaves the nest, it will take off quickly. Many other Finnish companies are currently in this state: Robit, DT, Optomed, Qt etc. etc.

However, if Easor gets listed, I don’t think that’s a bad option either. Then, however, it remains to be seen what its true competitiveness is. Unfortunately, I don’t have any insight into the matter. But Spain, in particular, raises hopes. At least Talenom’s timing at the forefront has been good, both regarding accounting firm business and software.

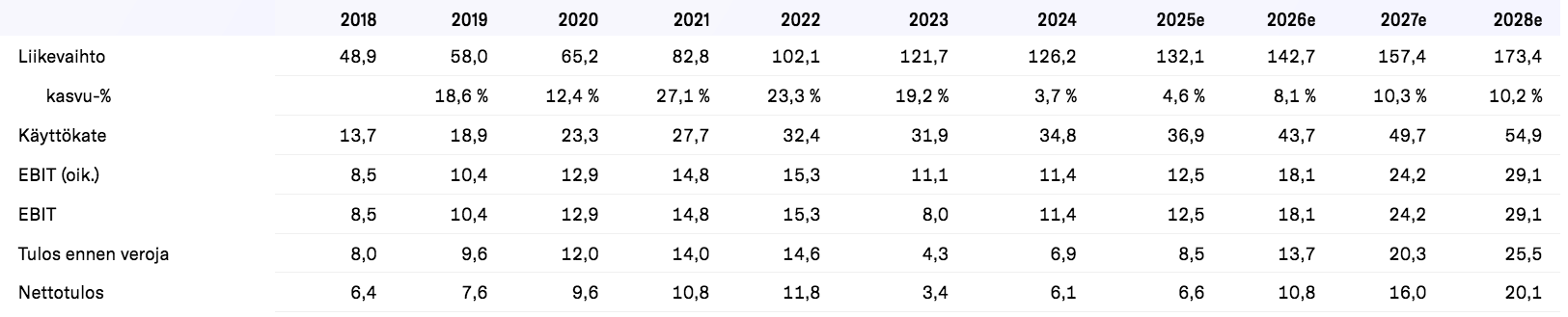

Still of the opinion that this has been pushed surprisingly deep into the ground, when looking at, for example, this time series listed by Inden:

Growth has occurred every year, and EBIT has also remained around 10 million. If they succeed even moderately, especially in Spain, and Sweden progresses as promised, then I suppose those forecasted double-digit growth figures will be reached quite easily. Economic indicators are also on the rise, even in Finland.

EV/S has come down from ten to the current approximately two, so the ‘Market gentry’ isn’t expecting much from this. In my opinion, it should have picked up after the announcement, and I have added a bit. SaaS to see if TaaS gets a beating ; )

13 Likes

Why on earth would Visma buy Easor when it has Netvisor, in which it invests a lot?

6 Likes

Visma’s acquisition strategy is not based on developing a single product, but on controlling the entire market through multiple brands. Although, as you said, Visma has invested heavily in Netvisor, acquiring Easor would be a completely consistent and even expected move. I don’t know how familiar you are with Visma in general. Here are a few reasons why Visma is clearly the strongest buyer candidate:

1. Market Consolidation and Elimination of Competition

- Visma has continuously acquired its competitors and technology providers to strengthen its position in Europe and especially in the Nordics. Easor is a high-quality and modern competitor with a significant customer base already in Finland and now also a little in Sweden and Spain. By acquiring Easor, Visma would not only increase its own market share but, above all, eliminate one of its most significant and potential competitors from the market. This would be good to do immediately, before Easor gains a significant foothold with Talenom outside, and before the valuation gets out of hand. Visma tried to acquire Fortnox in 2016, but the redemption attempt did not go through. I don’t think Visma wants to see this same thing happen again in Finland or Spain, where it has Holded. Visma also has Spiris in Sweden.

- I also don’t believe Visma wants to see Fortnox, with a new owner, acquire Easor and become a direct competitor not only in Sweden but also in Finland and Spain. Alternatively, British Sage, Dutch Exact, French Cegid, which are constantly seeking growth and expansion into new geographical areas. Easor would provide an excellent “bridgehead” to the Nordic markets and bring them a modern, cloud-based product.

- I also don’t believe Visma would want PE firms like KKR to come in and give Easor the necessary resources to share markets with Visma and others.

- Visma is listing on the LSE in London in 2026 with a valuation of approximately 16 billion pounds. An Easor acquisition, complementing the portfolio compared to a competing entity, would be a clear strategic move.

2. Multi-Brand Portfolio Strategy

Visma does not aim to force all its customers into a single system. Instead, it maintains a portfolio of several different software and brands that serve different customer segments and needs. For example, in Finland, Visma already has the Fivaldi software alongside Netvisor.

In addition, Easor could be integrated into Visma’s portfolio as its own product, competing for certain customers alongside Netvisor. Easor would easily go to the smaller end, and Visma would have enough sales and distribution power ready for proper implementation. This would give Visma broader market coverage and reduce the risk of customers choosing a competitor entirely outside Visma.

3. Technology and Customer Base Acquisition

It’s also easy to forget the technology of the Easor software itself, which can achieve up to 90% automation. Acquiring this technology and the expertise behind it is valuable to Visma. Visma has previously acquired companies precisely for their technology, such as FabricAI, which focused on artificial intelligence and automation. Now, the market has started to push AI solutions for only certain parts of accounting, making Easor’s advertised efficiency benefits easier to integrate into the market. At least my accountant said that compared to other solutions in the industry, the software has a clear advantage.

Furthermore, Easor’s existing customer base represents directly acquirable, recurring revenue. This provides a certain security for the acquisition, even if the 2027 sales process would involve more “external customer base” compared to the 2026 sale. On the other hand, this gives Visma the opportunity to acquire before the markets start pricing in the growth of the external customer base + acquisition premium on the stock exchange.

19 Likes

I believe I am reasonably well-informed about Visma. They already have many similar products at different price points, and Visma has also made significant improvements to Fivaldi. I consider it highly unlikely that Visma would acquire Easor. Easor is not a significant competitor to Visma compared to Procountor and Fennoa. I am not convinced about the modernity of Easor’s backend either, though I could be wrong.

11 Likes

If Talenom’s software, now Easor, were to be abandoned in Finland, I myself don’t believe Visma would be interested in it in any scenario. Instead, Accountor Group’s Accountor Finago could come to the carcass as part of some larger long-term plan. Accountor could simultaneously buy Talenom’s remaining parts and consolidate a bit more of the market at once. One would need to know a bit about the owners’ mindsets to know if this is realistic…

In Spain, however, Talenom’s software might even interest Visma, but would it become too difficult to carve up all the work of the last 5-6 years and get crumbs from here and there? Too many cooks in the kitchen?

Fortnox has tried to enter Finland, and that salty puddle between Finland and Sweden seems surprisingly difficult to cross, from either side. So, Fortnox is unlikely to be interested in this carcass. Perhaps some international private equity investor?

It’s really hard to make sense of Talenom anymore. It feels like the competitive advantages the company had five years ago have somewhat gone down the drain, and now they are only looking for dividends and a final climax.

6 Likes

Accountor’s accounting firm business is currently under Aspia. In Finago’s software business (Procountor, etc.), KKR is the main owner. Of course, KKR/Finago could in some scenario be interested in Easor if the product is truly competitive, and a few other parties as well, but I consider Visma an unlikely buyer.

In Spain, Talenom seems to use Nomo as a platform, which was acquired in 2022? Is Easor even used in Spain?

Is Nomo now part of Easor, after all? I don’t know if this has been commented on anywhere, but one would assume it is.

For Visma, this would likely be more of a competitive market buyout of a potential competitor. KKR & Accountor Software, on the other hand, would be able to grow its scale closer to Visma and specifically open up Spain + Sweden. KKR has the Next Generation Technology Growth Fund III, which is a $3 billion fund. This is specifically aimed at high-growth European SaaS companies. Accountor Software originally came from the KKR European Fund VI.

Here’s the difference between the funds:

KKR’s European Fund VI is a large-scale private equity fund (buyout fund) designed to acquire majority stakes in established, profitable companies with significant revenue. Accountor Software, with reported revenue of 132 million euros and a history of ten years of uninterrupted growth, fits this profile perfectly.

In contrast, KKR’s Next Generation Technology Growth fund family typically focuses on earlier-stage, high-growth technology companies with a different risk-return profile. A global player like KKR has separate capital funds for different strategies, and Accountor Software’s maturity and size made it a clear target for a private equity fund, not a growth equity fund. Easor fits this category more easily. On the other hand, Accountor Software’s subsidiary Accountor Finago acquired Heeros, so it’s difficult to say which of these funds would be relevant. It depends on whether the intention is to combine them “under the same umbrella” or keep them separate.

3 Likes

That’s a good question, I’d be interested to hear facts about this, if there are any.

1 Like

Spanish software is also under Easor. That’s where Easor’s biggest “organic” growth opportunity is in the coming years.

Nomo is more of a customer interface, and Talenom has also built an accounting firm view and related features. As I understand it, the a3 system, which is a local market leader, is used for accounting in the background – similar to how in Finland there was historically another system/database on top of which proprietary functionalities were built before it was completely phased out. I recall it was Vivaldi here at one time, but I might be wrong – I didn’t bother to dig up old notes now.

The accountant’s features are probably still limited, but it’s no longer the same Nomo that was acquired 3 years ago. I’m not entirely sure if the brand is still in use in Spain, but development has progressed.

Edit: Not Vivaldi but Tikon. Thanks for the correction @tj_hodl

16 Likes

This text completely lacks realism.

Easor’s revenue outside of Talenom is close to zero, so all evidence is yet to be presented. I recommend rethinking the EV/Sales multiple and especially considering what Sales figure should be used here.

6 Likes

Hey @Massimo1

Great speculation, which this thread (too) needs ![]() I’ve been a bit busy lately, so commenting has been left undone, but here are some thoughts.

I’ve been a bit busy lately, so commenting has been left undone, but here are some thoughts.

If Talenom (or its owners) wanted to sell Easor, a dual track would, in my opinion, be the right way to maximize the price. And your idea of a “Northern European accounting firm consolidator” is not, in my opinion, ruled out, considering the main owners. I don’t believe for a second that the Tahkolas would sell Talenom entirely. But selling Easor in a situation where they could then accelerate the service business… ![]() I can’t paint their soulscape that precisely, but if the price was right, then a strong maybe.

I can’t paint their soulscape that precisely, but if the price was right, then a strong maybe.

I wouldn’t be so confident about Visma as a buyer. My feeling is that Visma is still doing well and it’s more Accountor (Procountor) that has been struggling a bit. It feels clunky and more like a legacy system to me, but of course, I use Visma more myself, which might distort my perception. Of course, Easor is a threat to Visma in itself, but I wouldn’t be that worried there. The IPO story, growth, position, and so on, can certainly act as an incentive, but how deeply would Visma then be willing to dig into its pockets? I don’t know, I wouldn’t rely on that.

Fortnox could be an even more potential candidate through its international expansion, but I don’t really know how that would fit into their ecosystem. Would it just be accepted that we have this in Sweden and then abroad we go with this spearhead, when our own previous plans have not succeeded? Potentially possible. I haven’t followed their strategy more closely since the takeover bid, I’ll have to look into it. Presumably, they need to get growth from somewhere, otherwise, the acquisition wouldn’t have made sense.

Although that is tempting speculation in itself, I would probably still consider the most likely scenario to be that the IPO will eventually happen. In itself, Easor is still in such an early stage even next year that if one believes in its competitiveness and future, a possible exit should only be made later. A few years of strong growth and conquering positions, and the acquisition candidates would not be limited to “strategic” ones, but there would be private equity firms in line. At least currently, this sector is hot, and I don’t believe the situation would change, at least if the numbers pointed northeast. That, of course, doesn’t mean that a dual track couldn’t be underway in the background anyway - sales just wouldn’t go through ![]()

Perhaps a bit of a boring answer, but who knows about these things. We’ll keep following.

30 Likes

Thank you for the answer. It was Tikon which was previously the market leader and which Talenom used.

5 Likes

That’s exactly right. I had already forgotten that such a thing existed. Vivaldi is still alive, and has apparently received some updates too.

2 Likes

And Vivaldi is therefore Fivaldi. Visma as a name (e.g., “I use Visma at work” doesn’t mean anything) is now more of an umbrella for hundreds of applications, increasingly also in Central Europe, as expansion through acquisitions began towards Southern Europe in the early 2020s. In Finland, people probably talk about Visma, although more accurately, the largest user base consists of Visma Solutions’ Netvisor users and should be referred to as (Visma) Netvisor. The same company, however, also sells (Visma) Fivaldi nowadays, as the old Visma Software was merged with Solutions.

Visma is a collection of acquired SaaS companies from different sectors, in different countries. Wilma, the student information system loved by everyone, is software founded by StarSoft, which Visma acquired about ten years ago. Since then, it has been part of rebranded country companies and is now part of Visma Aquila. Visma is Visma…

Visma’s acquisition strategy, however, especially recently, has been to acquire more small, growing, and particularly nationally or geographically strong SaaS companies. From Oulu, for example, they acquired Suomen Vesitieto last year, which offers a specific SaaS product with strong growth and profitability to municipalities and water utilities. Perhaps they could expand that to Sweden, but after that, the products turn into cash cows.

Visma does not actually acquire cash cows, but rather opportunities that offer growth. Of course, the different life cycle phases of Visma products mean that eventually, those cash cows are inevitably carried along, which they try to bury or extract what can be extracted from them.

If one considers this, why would Easor be of interest. It probably only offers some industry-specific (machinery and car trade) synergies, where Talenom once ironed out certain reverse charge VAT processes, but in terms of software, that’s probably where it ends, at least in Finland.

A bit off-topic, except for industry specifics and speculations regarding Talenom’s future. ![]()

14 Likes

Now Jutila has completely disappeared from the latest ownership list. As a correction to the previous (statement), it seems he is not Easor’s leader but holds the title “Senior Sales Manager, Easor Oy, Talenom Oyj”.

2 Likes