It’s good to mention at the start that the main source was this:

This wasn’t the only source, of course; I visited various sites, I’ve familiarized myself with the industry, and checked out the company’s own pages, but as mentioned, without Lucas Mattsson’s material, I wouldn’t have done this. ![]()

I am responsible for any misunderstandings and errors in the text below, as I may have misunderstood something, etc.

Fortnox is a leading Swedish company providing enterprise resource planning systems (ERP ![]() , a swear-word acronym to me), focusing particularly on the needs of small and medium-sized enterprises. The company’s success has largely been based on its offering of cloud-based software solutions, which include accounting, invoicing, payment, and financial services, etc. Fortnox has been able to meet the modern needs of the market, moving from “folder-notebook-abacus” platforms toward digital and cloud-based solutions.

, a swear-word acronym to me), focusing particularly on the needs of small and medium-sized enterprises. The company’s success has largely been based on its offering of cloud-based software solutions, which include accounting, invoicing, payment, and financial services, etc. Fortnox has been able to meet the modern needs of the market, moving from “folder-notebook-abacus” platforms toward digital and cloud-based solutions.

Fortnox’s growth story can be divided into three significant phases:

-

2001-2010: The company’s early years were challenging. Fortnox struggled with losses and a failed international expansion (sounds like a Finnish firm), which slowed down development.

-

2011-2019: Fortnox began to grow profitably and was able to significantly increase its market share. The company benefited from an expanded product range and was able to scale its business.

-

2020-2023: Fortnox focused on inorganic growth, executing five acquisitions to expand its product portfolio. This strategy further strengthened the company’s position in the market.

Fortnox has also been impressive in terms of revenue, with growth averaging 37 percent annually over the last decade. The company’s profitability has also been significant, as its EBIT margin has risen from 17 percent to 41 percent in the period 2014-2023.

The scalability of the business model is in good shape, as are the gross margins: over 90 percent. Additionally, Fortnox has managed to keep its return on equity (ROE) at an average of 51 percent and return on invested capital (ROIC) at 43 percent.

The growth of Fortnox’s customer base has been a significant driver of revenue, but in recent years, increasing revenue per customer has also become more important; they probably keep pushing additional services at a steady pace. The expansion of the company’s product range and high switching costs have strengthened Fortnox’s competitive position in the market.

Fortnox’s share value has grown substantially—between 2014 and 2024, the share price rose by approximately 7,285 percent (when taking dividends into account), which corresponds to an average of 49 percent annually. “They can’t go up anymore,” said Rookie (Alokas), while looking at the “Magnificent Seven” stock prices in 2019.

In brief:

Fortnox has established its position as a leading player in the Swedish ERP market, especially among small and medium-sized enterprises. The company’s strategy focuses on growing the customer base and expanding the product range, which enables its continued strong growth and long-term shareholder value creation. One would believe that a company like this would succeed better in internationalization in the long run; a strong foundation and inorganic momentum, and that’s that. ![]()

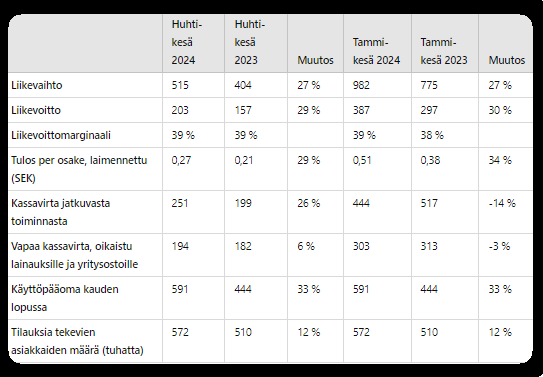

Q2/2024

(I apologize for the clumsiness in the table below. Figures are in “million SEK” unless otherwise mentioned.)

OMXHGI is included in this image, but isn’t visible because it’s almost a flat line. ![]()

EDIT:

I think that @lucas.mattsson will be happy to answer questions. Questions can probably be asked in English or Swedish. ![]()