This thread is for discussing Easor.

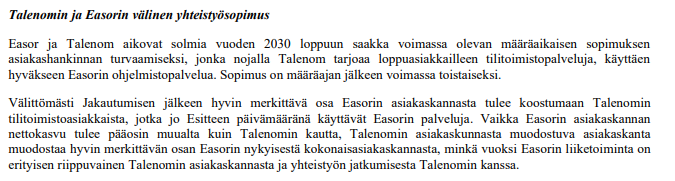

Talenom is splitting into two: Talenom and Easor. A decision on the matter is expected to be made at the General Meeting on January 27, 2026, and the demerger is intended to take place during H1/2026. Current Talenom shareholders will receive shares in both Talenom and Easor in a 1:1 ratio.

Otto-Pekka Huhtala has been proposed as the CEO of Easor. Harri Tahkola has been proposed as the Chairman of the Board, and Johannes Karjula, Taina Sipilä, and Saara Kauppila have been proposed as the other members of the board.

Unaudited pro forma key figures:

Easor’s guidance for 2026:

“Net sales are estimated to grow by 3–10 percent compared to the 2025 carve-out-based net sales. The operating profit margin is expected to weaken due to the construction of distribution channels and growth investments. These measures create the conditions for long-term growth. The operating profit margin will also be burdened by the costs of operating as a separate listed company.”