You make great graphs; forecasting indeed seems difficult, as your summary with the same content always shows once a quarter, in almost every thread. It would be a miracle if Inderes hit the mark in this macro environment, when even company management finds it difficult to forecast their own business, as we can conclude from all the recent negative surprises.

Would your model be flexible enough for you to make your own forecast or tell us in advance why Inderes’ forecast will not materialize? Everyone already knows that history by reading the earnings report.

As for Talenom itself, in Otto-Pekka’s interview, I was somewhat interpreting between the lines that a dividend might not be paid in the autumn. This is a good thing for the company, but I suspect it will be another negative surprise for the market and a message of weak management in its own way.

“On July 29th, the (list of approved software) should be released.” So, today at the earliest, there should be information on whether Talenom has received approval in Spain according to the e-invoicing directive.

Someone please post an update if information about this becomes available through any channel.

EDIT:

Found it here:

There doesn’t seem to be any investor communication on the matter yet, but it apparently is on the list, and no setbacks on that front.

There are many reasons to sell, but it is not a pleasant observation from the perspective of a potential investor that Easor’s lead is selling off shares quite vigorously:

According to this, a larger amount was last sold in '22. However, it is not currently listed among the insiders there. Of course, if still involved in that business, this certainly doesn’t encourage purchases.

It would be nice to see insider additions at these prices or share buybacks instead of dividends. However, Kaksoismoottori has increased its ownership quite nicely

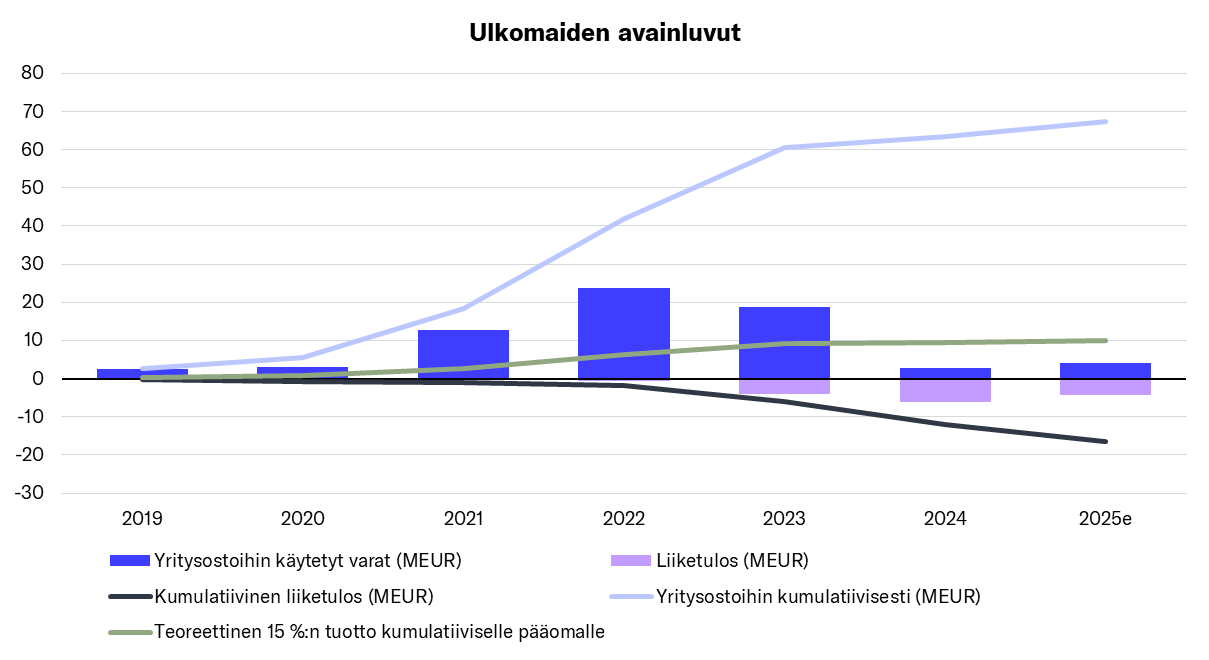

There’s been a lot of talk here about how internationalization, and especially Sweden, has been quite a drag for Talenom. I put together some rough material for another purpose, so I thought I’d share the following graph here as well:

The point probably comes across directly from that, but let’s state the following:

Talenom has invested almost 70 MEUR in acquisitions abroad since 2019 (including 2025e). In practice, this has gone to Sweden and Spain, and a little to Italy. The exercise is furthest along in Sweden, and the results so far are the worst.

My own subjective estimate is that in successful acquisitions in the industry, the payback period would be 5-7 years. This, to my understanding, has also roughly materialized in Finland.

Related to the above, I put a theoretical 15% return on cumulative capital there, but in reality, the curve would not, of course, be linear. However, we are now far enough from the first ones that they can already be “judged.”

So far, the earnings contribution from Sweden and Spain has been roughly negative 15 MEUR for Talenom over the last five years. This is not an exact figure, and the forecast for late 2025 will push that even lower.

As a side note, the last period of zero interest rates was otherwise a bad time to hit the gas in terms of acquisitions.

Of course, things take time, and the results include country organizations and other costs, so this cannot be directly attributed to the results of acquisitions – but it hasn’t exactly gone smoothly. This is also the biggest reason why this case has gone the way it has in recent years. Rarely does one put negative returns on investments into Excel, at least not for a very long period.

Well, an optimist would say there’s a hell of a lot of potential if we can get on the right track. A pessimist would curse the whole exercise. A realist might say that this misery is indeed reflected in the share price. I won’t say more myself.

You’re talking nonsense. “Sweden is a s*** country.”

Somewhat less attention has been paid to Spain’s renewed acceleration, after a small lull when the sales director changed. On top of that, Verifaktu may now genuinely bring new business. Empiria reports that authorities there have taken a drastically tougher grip even on private bank accounts.

From the link below, when you scroll to the country-specific table, we can see that Talenom has managed to choose three out of three European countries with the highest unemployment for its business operations (quite an achievement in itself). The positive thing is that in at least one of them, unemployment has decreased from a year ago, as it has on average across the entire EU area. And it’s also positive that, under these circumstances, they have managed to achieve even somewhat tolerable results. And furthermore, it’s positive that Sweden’s results are likely on the rise.

I can’t know for sure, but I assume, based on the news flow and Verneri’s articles, that Europe’s economic development is now on an upward trend. This should be positive for both Finland and Sweden. Our government has also promised to promote entrepreneurship, so there are ingredients for the wave of bankruptcies to subside and even for new businesses to emerge.

The company has surprisingly made a lot of acquisitions since the beginning of the war in Russia. They probably couldn’t estimate the duration of the war and its worsening consequences, such as the energy crisis, rising interest rates, etc. A separate issue is the big duck in America, which has messed up trade policy patterns and created significant uncertainty for companies’ US businesses. This, of course, only has indirect consequences for Talenom. But Sweden’s struggles and the shifting of the jam jar have certainly been sad to watch.

New black swans may emerge again, but this summer too, in our nearby pond, 6 vigorous cygnets hatched, whose grey colour is starting to turn white. So I choose option 1, meaning a lot of potential, getting on the right track, and the stock price

In Talenom, there now seem to be almost daily internal block trades by Danske. This morning, a block trade of 25,000 shares. Within the last week, there have been 3. Last month, Elo was the sole seller. It will be interesting to see who acquires these.

How would this then work in practice? Does Talenom still have an interest in favoring Easor? Would Talenom remain a large owner of Easor? A fairly large part of Easor’s growth path is converting those Talenom customers into Easor users.

Furthermore, in my opinion, Talenom Online has only gone in a worse direction since they changed it to Easor. The latest sales invoicing update is a new low. They apparently pulled back the purchase invoices update? Initially, when it came out, one couldn’t even approve anything but Finnish invoices.

Poor updates and the system’s old rigidities made me look for a different solution for financial administration.

That graph and post are a good description of the financially challenging progress of internationalization.

But, could the root cause for the slow growth, if not outright failure internationally, be the unfounded assumption that “what works in Finland, works abroad“? In practice, things just don’t work the same way in different countries. Furthermore, for expansion, so-called conservative countries have been chosen, where market disruption, when done by a Finnish player, is not a walk in the park.

How one could have analyzed this cultural management challenge, who knows, if the company management boasts about having acquired “the

I am initially negative about this news. What’s the rush to list Easor in this market situation? At least we’ll have two sets of listed company expenses.

This reflection from the previous message is quite relevant, in my opinion. Why on earth would I, as an owner of pure Talenom, want Talenom to favor Easor’s software (if I don’t own Easor myself) over someone else’s in the future?

I get the impression that Easor might not be in as good a market position (or as good software) as is implied, and now has been deemed a good time to “cash in” what can be cashed in. Why not wait a couple of years for Easor to show good growth figures? Easor’s leader just recently cashed in a significant portion of their Talenom shares.

Of course, all this deliberation is speculation/fluff until we know if the listing will happen and how it will practically occur. Talenom’s share price has been lively all week. That also raises some questions.

These issues have been pondered quite a lot earlier in this thread. I wouldn’t necessarily sum up Sweden and Spain in the same category; they are so different countries and Talenom’s development has also been different. But regarding the expansions in Sweden, one could playfully say that what works in Finland will not work in Sweden