I don’t have an account myself either. There was a summary of it in Recuro’s newsletter. Exactly, that authors want better compensation. Time will tell if anything comes of this.

1 Like

Strong Q3 results and an update to the 2024 guidance. The new CEO has started.

Highlights

Unless otherwise specified, numbers are for Q3 2024 and are compared to Q3 2023

● Group revenue up 7% to 954 (896) MSEK, and 8% at constant exchange rates (CER)

● Streaming revenue up 5%, and 8% at constant exchange rates (CER)

● Publishing revenue up 13% with an increase in digital sales of 18% and print sales of 6%

● Adjusted Gross profit up 18% to 436 (368) MSEK, equaling a margin of 45.7% (41.1%)

● Adjusted EBITDA increased by 77% to 178 (101) MSEK, equaling a margin of 18.7% (11.3%)

● The Group updates its 2024 guidance on adjusted EBITDA margin to be around 15% (from 13%), on

operational cash flow to be at least 10% (from 8%), and on organic revenue growth to be around 8%

(from 10%)

● Bodil Eriksson Torp assumed the role of CEO of Storytel Group as of October 1, 2024

The previous CEO’s (Johannes Larcher) couple-of-year tenure shifted the company’s direction from ambitious growth to focused profitability. Now that the company has become quite solidly profitable, it remains to be seen how they continue from here. There is still massive growth potential outside of these core markets.

3 Likes

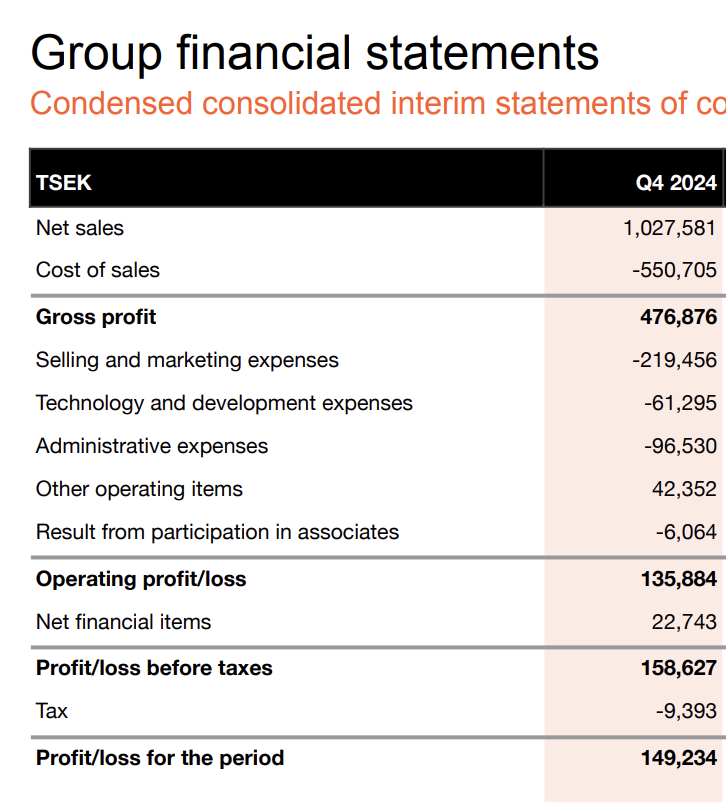

Unless otherwise specified, numbers are for Q4 2024 and are compared to Q4 2023

-

Group revenue up 9% to 1,028 (946) MSEK, and 8% at constant exchange rates (CER).

-

Streaming revenue up 7%, and 6% at constant exchange rates (CER).

-

Publishing revenue up 15% with an increase in external sales of 17% and internal sales of 13%.

-

Adjusted Gross profit up 29% to 477 (370) MSEK, equaling a margin of 46.4% (39.2%).

-

Adjusted EBITDA increased by 96% to 192 (98) MSEK, equaling a margin of 18.6% (10.3%).

-

Items Affecting Comparability (IACs) of 31 MSEK include a one-off compensation of 34 MSEK received from Copyswede relating to private copying levies in Sweden for historic periods.

-

For the full year 2024, Storytel Group exceeds its guidance on organic revenue growth (actual: 9%, guidance: “around 8%”), on adjusted EBITDA margin (actual: 15.8%, guidance: “around 15%”), and on operational cash flow (actual: 12.1%, guidance: “at least 10%”).

-

After the period, Storytel Group acquired a majority stake in the Swedish publisher Bokfabriken. Following discussions with the Swedish Competition Authority (SCA) in February, Storytel has decided to voluntarily give the SCA an opportunity to review the transaction, even though there was no obligation to do so.

5 Likes

This is exactly the development I hoped to see after the last quarter: marketing and sales costs are growing less than revenue (and at the same time customer retention has improved / churn has decreased). The efficiency of customer acquisition is thus significantly improving.

This suggests that the company does not need massively long free trial periods in the same way (or at least people don’t leave after them).

This is probably already reflected in the stock price, but I’m starting to have enough confidence that I’m seriously considering jumping on board.

3 Likes

No, they don’t leave, as customers were promised a permanent -50% price in a campaign last year for as long as the subscription is valid. That makes even me keep my Storytel subscription active without interruption. Ten euros a month with a hundred-hour usage limit is a pretty good deal for the consumer.

3 Likes

Good information! In theory, that certainly drastically reduces the revenue from some subscriptions, but on the other hand, the total customer value can increase quite significantly when churn is reduced, and the customer doesn’t always have to be “bought” back in with new campaigns (and money spent on advertising).

1 Like

Tulos

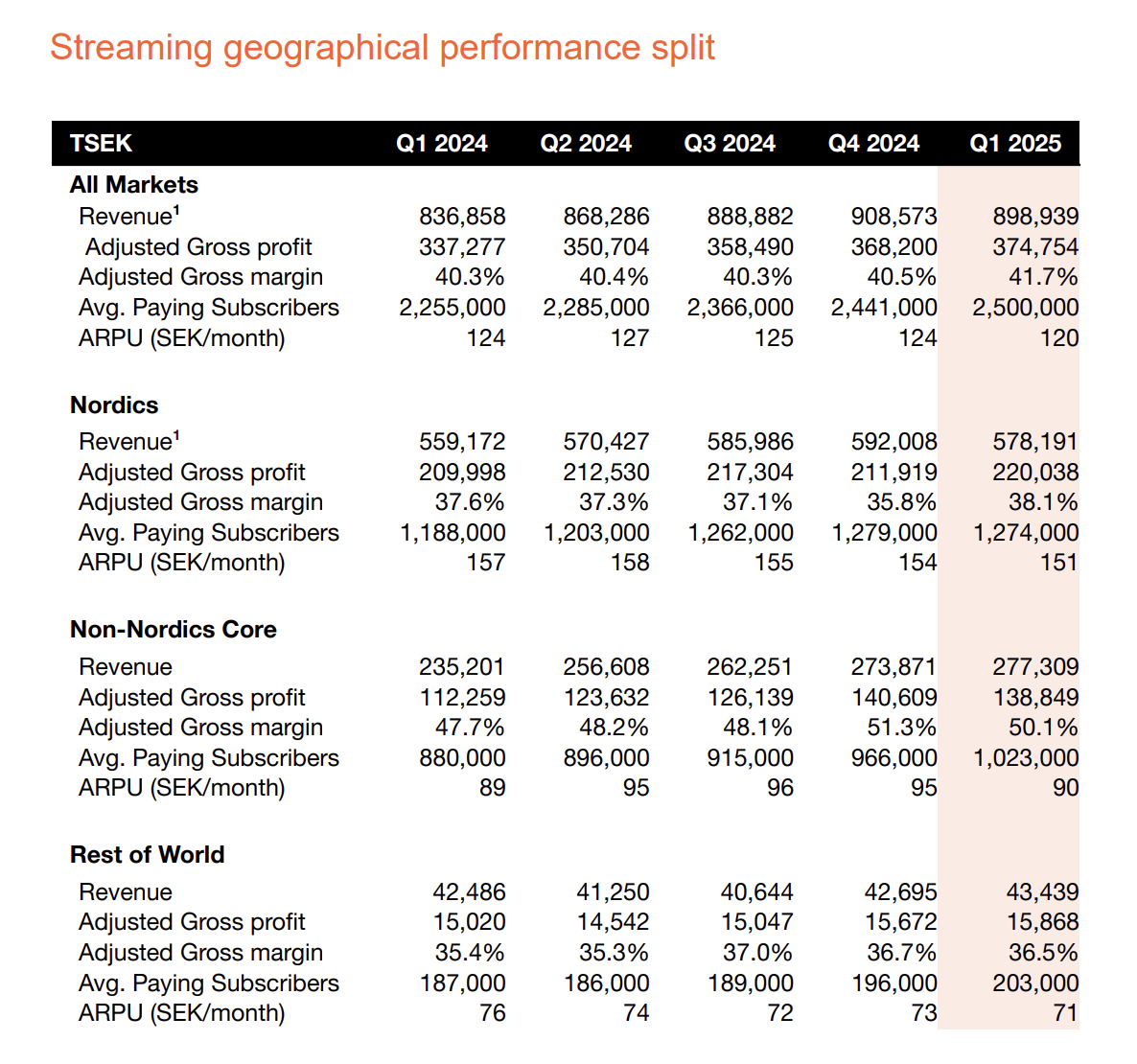

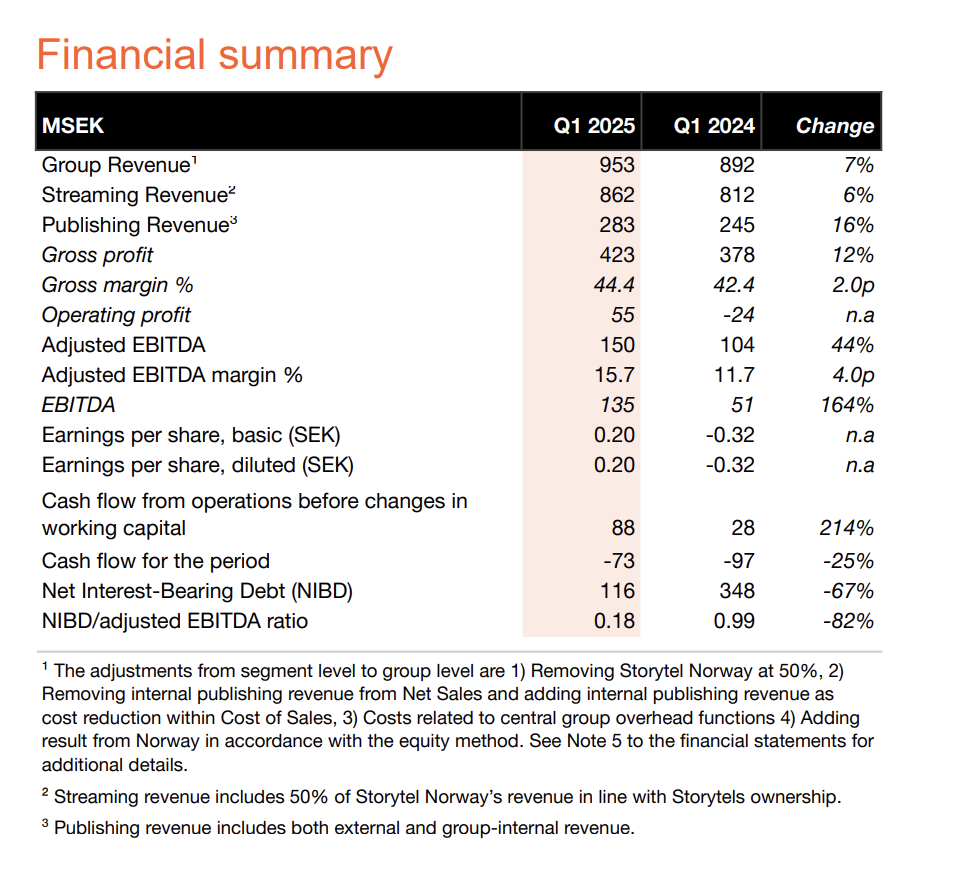

Storytel Group reports solid operational performance, surpassing 2.5 million subscribers in the first quarter 2025

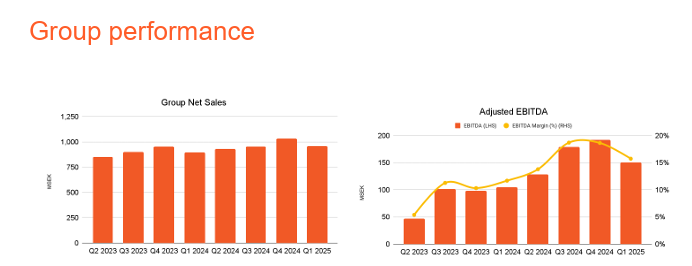

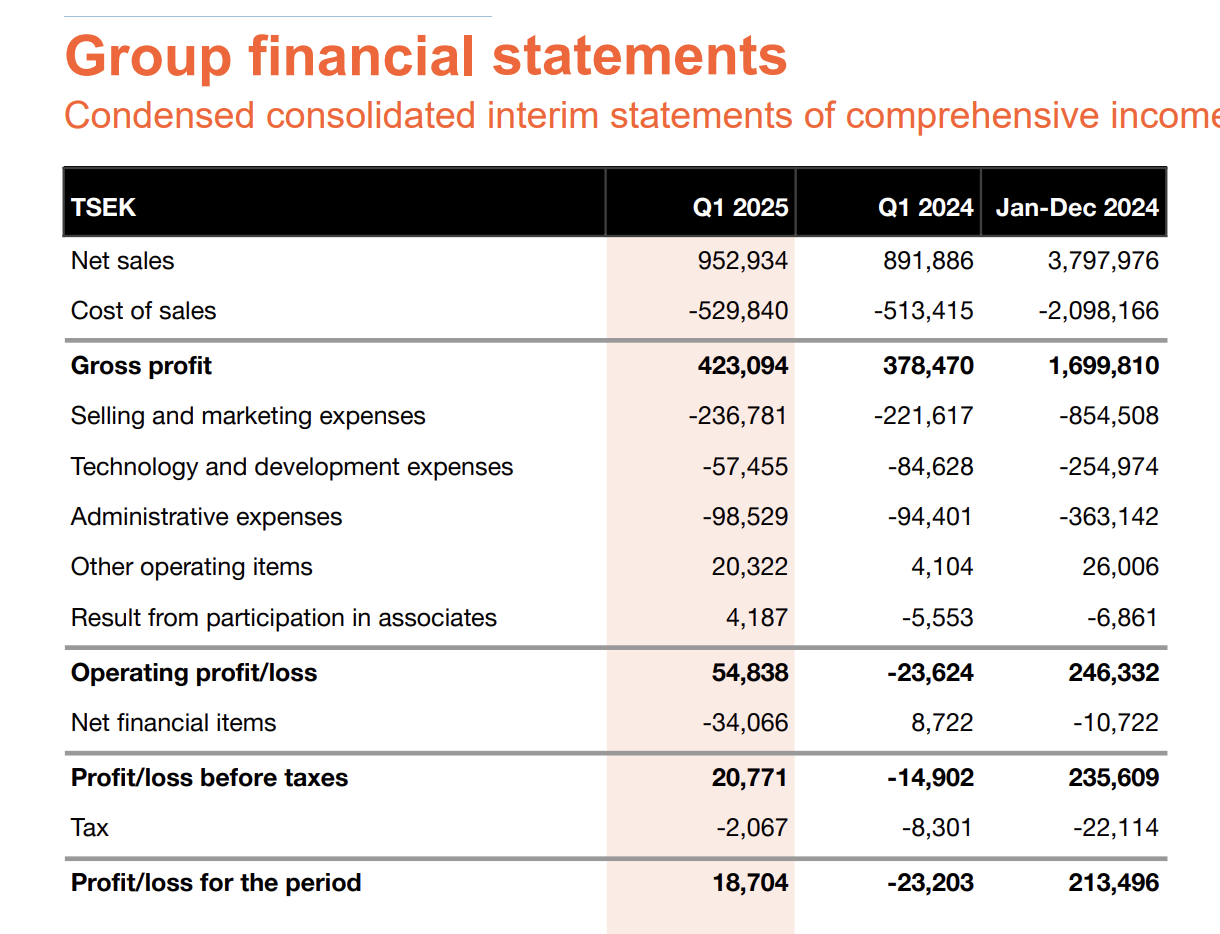

Group revenue up 7% to 953 (892) MSEK, and equals 7% at constant exchange rates (CER).

● Streaming revenue up 6% and Publishing revenue up 16%.

● Gross profit up 12% to 423 (378) MSEK, equaling a margin of 44.4% (42.4%).

● Adjusted EBITDA increased by 44% to 150 (104) MSEK, equaling a margin of 15.7% (11.7%).

● Items Affecting Comparability (IACs) of -15 (-55) MSEK, fully related to long term incentive programs and not affecting cash flow

● Net profit for the period amounted to 19 (-23) MSEK.

● Earnings per share, before and after dilution, amounted to 0.20 (-0.32) SEK

● The Board of Directors of Storytel Group proposes to the Annual General Meeting a one-off dividend of SEK 1.00 per share.

4 Likes

The numbers look good there, but the market reaction is a harsh -15% currently. Perhaps it’s explained by a somewhat weak performance compared to the previous quarter. I’ll have to chew on it more later tonight.

1 Like

This looks pretty good to my eye, and I am considering adding more.

- Growth has been steady, although there was a dip compared to the previous quarter (the larger drop was, in my opinion, on the publishing side, about -50M SEK, where seasons have a greater impact)

- Marketing costs increased slightly vs. Q4/24, but cost of sales decreased more.

There are also some negatives/questions:

- A one-off dividend of one krona is proposed. I don’t quite understand why such a thing.

The Board of Directors of Storytel Group proposes to the Annual General Meeting a one-off dividend of SEK 1.00 per share.

- Subscriber growth in the Nordics stalled (dropped by 5,000 subscribers vs. the previous quarter - though this is only less than 0.5 percent).

- ARPU decreased moderately everywhere. However, this is reported in SEK, but revenue comes in other currencies, so perhaps the weakening of the euro (or other currencies) at the beginning of the year vs. SEK affects this?

4 Likes

New competition is entering the market: this time, the paid podcast service Podme – owned by Schibsted, a quite significant player in the Nordic region – is starting to offer audiobooks as well (at least in Finland and Sweden): Podme laajentaa sisältötarjontaansa äänikirjoihin | Podme

I don’t believe this will have a significant impact (at least not yet), but Podme’s strength lies precisely in its “original content,” which Storytel has also been striving to create. Of course, on Storytel’s side, this includes both podcasts and its own books/audio series.

1 Like

Audiobooks are available to subscribers of Podme’s new subscription option, Premium Total. In Finland, the price of a Premium Total subscription, which allows the user to listen to audiobooks for 100 hours per month, is 19.99 euros/month. A Premium Total subscriber can also listen to unlimited premium podcasts.

It seemed to be the same price as Storytel. I, for one, value Storytel’s original content more.

As stated before, I have previously used audiobook services for short periods, like a few months. However, a lasting relationship with Storytel was formed when the premium subscription was once promised permanently at half price. That is, ten euros a month. Currently, a similar subscription model is offered for the standard subscription: Hinnat ja tilaukset - Storytel

Such campaigns do eat into the margin, but they certainly help immensely in retaining the customer base.

There will certainly be more audiobook services, but large players naturally have a considerable advantage in offering original content and better prerequisites to compete profitably in terms of price.

3 Likes

Q2:

- Group revenue up 4% to 958 (924) MSEK and equals 8% at constant exchange rates (CER).

- Streaming revenue up 2%, equals 7% at CER, and Publishing revenue up 14%, equals 15% in CER.

- Gross profit up 6% to 434 (411) MSEK, representing a margin of 45.3% (44.4%).

- Adjusted EBITDA increased by 28% to 163 (128) MSEK, representing a margin of 17.0% (13.8%).

- Items Affecting Comparability (IACs) of -2 (-17) MSEK, fully related to long term incentive programs and not affecting cash flow.

- Net profit for the period amounted to 47 (32) MSEK.

- Earnings per share amounted to 0.55 (0.38) SEK before dilution, and to 0.54 (0.38) SEK after dilution.

- Cash flow from operating activities of 155 (78) MSEK.

- The Swedish Competition Authority approved Storytel Group’s acquisition of Bokfabriken

From the CEO’s review:

Our streaming segment achieved strong subscriber growth, with average paying subscribers totaling 2,546,000, an increase of over 11 percent year-on-year.

In the Nordic region, we achieved solid growth of 7 percent year-over-year, adding over 80,000 paying subscribers, of which 10,000 net new paying subscribers during the second quarter. Meanwhile, our Non-Nordic core markets are accelerating, growing by an outstanding 18 percent year-over-year and adding 35,000 new paying subscribers during the second quarter

The CEO forgot to thank Mikael’s book and the discount campaign for these figures.

4 Likes

Will comment better later, but here are a few highlights. Overall, it seems like a pretty OK quarter to me - growth is quite moderate but profitability is improving well.

- Streaming revenue actually dropped from Q1/25: 862 MSEK → 853 MSEK (but marketing costs dropped proportionally more, which is good)

- Profitability continued to improve well

- Cost of sales dropped slightly from the previous quarter, even though revenue increased

- Sales and marketing costs dropped from the previous quarter: Q1 -236.8 MSEK vs. Q2 -217.4

The earnings reaction seems to be quite similar to last time, with a small drop after the release. Let’s see if it recovers in the coming weeks.

Slightly annoyingly, these numbers in the reports are always only compared to the same quarter of the previous year, so below are both Q1/25 and Q2/25 numbers:

Q1:

Q2:

6 Likes

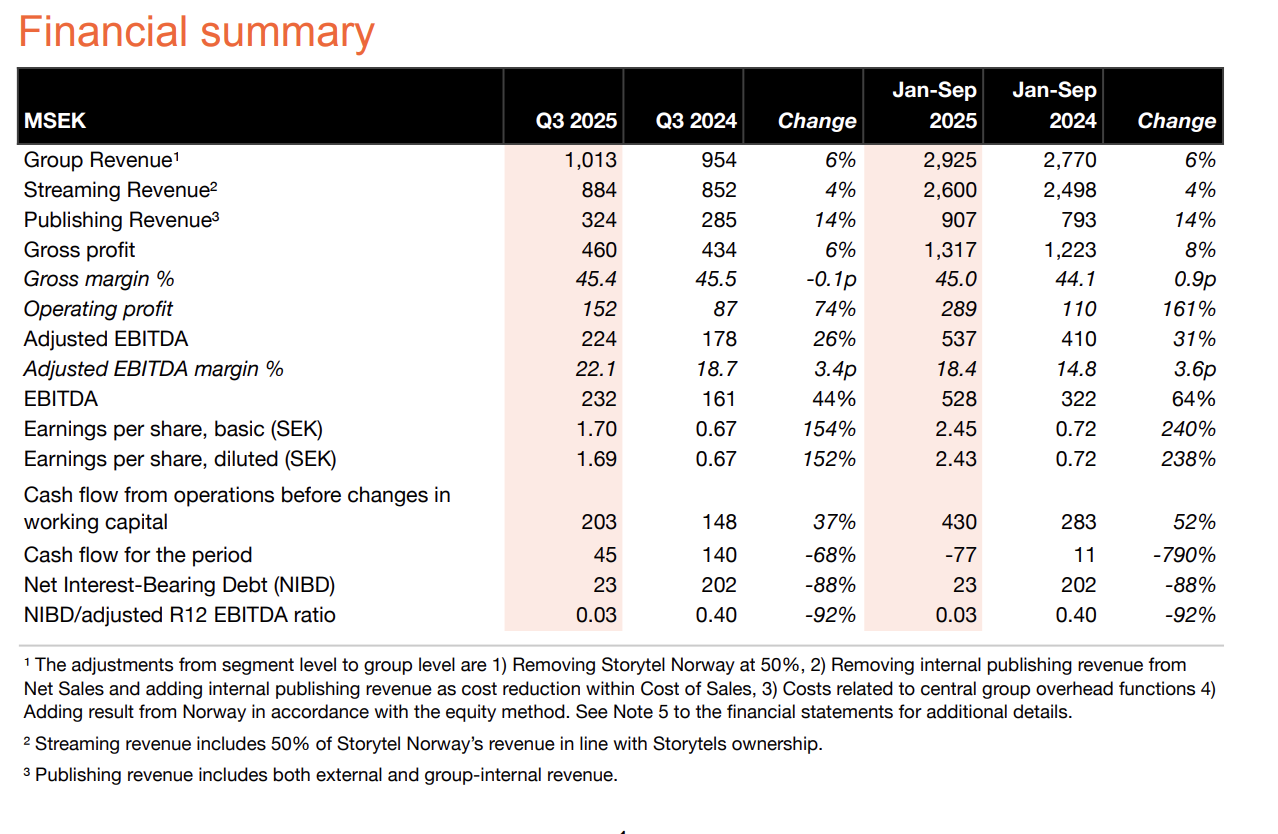

Q3

-

Group revenue up 6% to 1,013 (954) MSEK, and 9% in constant exchange rates (CER).

-

Streaming revenue up 4%, and 7% at CER.

-

Publishing up 14%, and 16% at CER.

-

Gross profit rose 6% to 460 (434) MSEK, for a margin of 45.4% (45.5%).

-

Adjusted EBITDA increased by 26% to 224 (178) MSEK, for a margin of 22.1% (18.7%).

-

Items Affecting Comparability (IACs) of 7 (-18) MSEK, related to long term incentive programs.

-

Net profit for the period amounted to 138 (55) MSEK.

-

Earnings per share amounted to 1.70 (0.67) SEK before dilution, 1.69 (0.67) SEK after dilution.

-

Cash flow from operations before changes in working capital increased to 203 (148) MSEK.

Significant events after the period

● We raise our 2025 adjusted EBITDA margin guidance to 18.0-19.5 percent (from 17.5-19.0).

3 Likes

Now I finally had time to look at this in more detail. I have somewhat mixed feelings about this: the train is going in the right direction regarding profitability and EPS quite well, but growth is indeed modest.

Pros

- Churn is on a downward trend

- Marketing costs barely grew even though revenue increased somewhat.

- Profitability is improving rapidly, and the full-year forecast was even slightly raised.

Question marks:

- Average subscribers grew by only about 2% from the previous quarter (and ~10% from a year ago) - can this even be called a growth company anymore?

- Streaming revenue growth is modest (Q1-Q3/25 increase of only 4% YoY). Profitability can be improved up to a certain point, but I believe there should be more growth as well.

- Of course, now that profitability is reaching a better level, perhaps we will start to see more rapid expansion in the future?

Here are the compiled figures:

5 Likes

Hesari writes that Spotify is now also starting to offer audiobooks in Finland.

And Spotify’s own press release. It is indeed expanding to the Nordics, and this is a bit of an unpleasant matter from Storytel’s perspective, as the Nordics is its largest market area.

5 Likes

I ended up selling my Storytel shares due to this news: I took a small loss, but for now, I decided to exit because:

- Growth is rather modest, and

- Spotify’s entry into the market will likely erode profitability, as more money will probably need to be invested in content production and marketing.

- Spotify Premium’s penetration is already very good in the Nordics. According to some studies found with a quick Google search, 95% of music listeners stream it, and nearly 50% pay for it (with Spotify likely taking the lion’s share), so this immediately impacts Storytel, even if the selection is narrower, etc.

Of course, this could still turn out very well, and I’ll gladly jump back on board when the picture clears up, but for now, I’m happier watching from the sidelines.

2 Likes

It took years from the first news that Spotify’s audiobooks became available here too.

At first glance, it seems unbeatable. It appears to have everything that Storytel/Bookbeat/Nextory has (excluding their own content) and, in addition, even more comprehensive English content, which I have had to buy from Audible due to its absence from other services. There are even a few books from my wishlists that I haven’t found in any other audiobook service.

In addition to the books included in Premium, some books can be purchased through the service.

When one is already paying for a music service anyway and gets a comprehensive selection of audiobooks for the same price, then it’s a truly challenging position to compete against.

I honestly didn’t expect such a good selection right from the start.

3 Likes

Spotify indeed had a comprehensive catalog, it completely surprised me.

The only consolation from Storytel’s perspective is that Spotify offers only 12 hours of audiobook listening per month included in Premium. Additionally, with an €8 surcharge, you only get 10 more hours, which makes the pricing quite steep compared to dedicated audiobook services.

Of course, this is where the competition begins, and it’s difficult to challenge Spotify’s might.

2 Likes

Exactly, Spotify is so expensive that I don’t necessarily see much pressure in the short term. Premium’s 12 hours is only enough for a casual listener, not for the target audience of audiobook services. An additional 10 hours for 8 euros will hardly change the situation much. When I myself pay 10 euros a month for Storytel’s 100 hours a month, I wouldn’t even think of switching.

4 Likes