Is SRV cheap or expensive?

If one looks at the P/E metric, the P=Price side is unusually clear, i.e., the stock price.

The E=Earnings side, on the other hand, has been severely flawed, and the company has repeatedly discovered large write-downs and made a couple of share issues in recent years, perhaps even to keep itself afloat.

Well, history is history, but one can certainly ask if the industry is so impossible that one cannot make money from it?

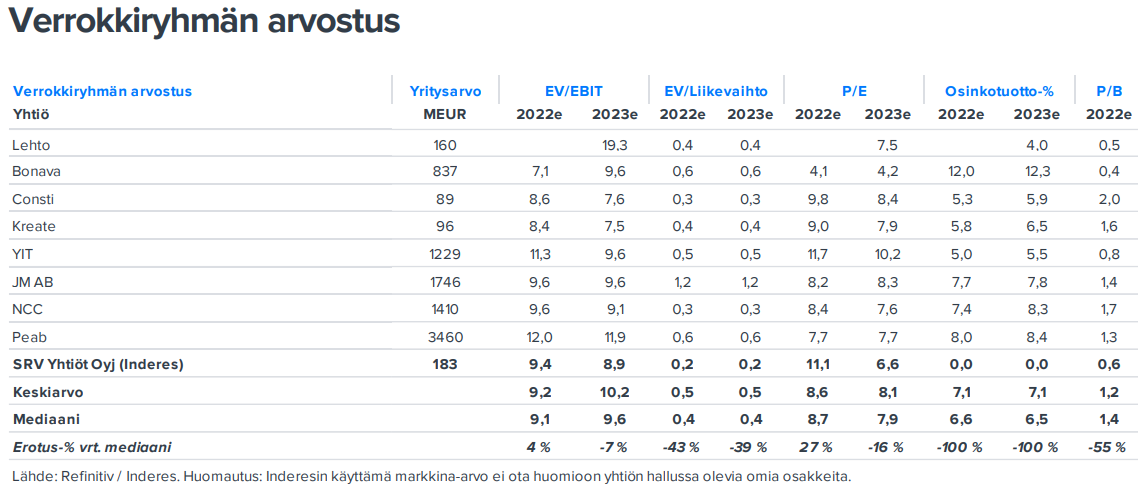

The report on July 22, 2022, refers to competitors. If one looks at them a bit, the EV/EBIT or P/E ratios are not bad at all.

I also looked at what kind of results (operating income) the companies have made. I took 12 months rolling if readily available, otherwise just H1 2022.

Although I’m not trying to make any comparable analysis here, SRV and Lehto certainly stand out, but not in a good way.

Secondly, it seems that a 3-6% operating margin would be achievable in the industry when looking at the references.

Thirdly, even with an estimated 2.4% operating profit for 2023, SRV’s P/E was <5.

Of course, if companies in the industry are capable of performing, what about the board, management, and other personnel of a single company? This is the problem.

SRV’s 15-year stock market journey has been, if not a continuous decline, then at least almost, including the most recent 6 years.

Have the board, management, and board learned something? Other than that, rights issues bring in money?

Are pricing models for projects able to incorporate some kind of risk margin?

Can project costs be kept under control?

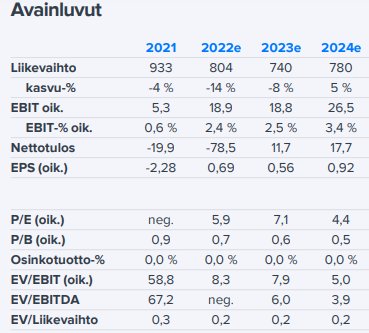

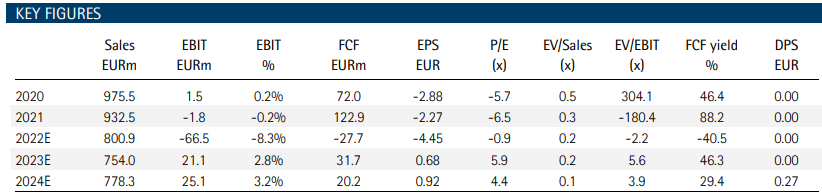

SRV’s good result is yet to be completed?

Examples:

-Skanska (12 mths rolling): revenue 160442 mSEK, operating income 9417 → 5.9%

-NCC (12 mths rolling): net sales 56462 mSEK, operating profit/loss 1786 → 3.3%

-PEAB (H1 2022): net sales 29402 mSEK, operating profit 895 → 3.0% (12 mths rolling 5.1%)

-Bonava (12 mths rolling): net sales 16886 mSEK, operating profit 1433 → 8.5%

-JM (H1 2022): revenue 7644 mSEK, operating profit 898 → 11.8%

-YIT (H1 2022): revenue 1063 mEUR, operating profit 44 → 4.2%

-Consti (H1 2022): revenue 132.9 mEUR, operating result 3.3 → 2.9%

-Kreate (H1 2022) revenue 117.4 mEUR, EBITA 3.5 → 3.0%

-Lehto (H1 2022): net sales 163.9 mEUR, operating result -21.5 → -13.1%

-SRV (H1 2022): revenue 402.1 mEUR, operating profit -75.6 → -18.8%

- and SRV (H1 2022): Operative operating profit 14.7 → 3.7%

-and SRV (Inderes 2023): 898 mEUR, operating profit 22.8 → 2.4%, EPS=0.73. P/E=5 at current price 3.50

-and SRV (Inderes 2024): 931 mEUR, operating profit 33.2 → 3.6%, EPS=1.22. P/E=3 -“-

-and SRV (Inderes 2025): 953 mEUR, operating profit 42.8 → 4.5%, EPS=1.70 - P/E=2 -”-

https://www.inderes.fi/fi/system/files/company-reports/yhtiopaivitys_srv_q222.pdf