Solwers Oyj is one of the smallest companies on the Helsinki Stock Exchange, but its acquisition-based growth strategy and its attempt to expand into Central Europe make it an interesting investment target.

In this video, I delve into Solwers’ business model, assess its risks and opportunities, and consider whether this company, valued at 33 million euros, could offer growth potential for a long-term investor.

Why does Solwers’ business model attract interest? What challenges are associated with the acquisition strategy? Is the profitability challenge only temporary? How could changes in market dynamics affect its future?

I listened to a rookie investor’s presentation. My interest was piqued, and I researched the company. This put me in a buying mood. Solwers’ Chairman of the Board acquired company shares for nearly 150,000 euros

March 26, 15:27 ∙ Arvopaperi

Consulting company Solwers’ Chairman of the Board Leif Sebbas acquired company shares for 148,960 euros through investment company CEB Invest.

The acquisitions were made on March 20 at an average price of 3.92 euros. A total of 3,800 shares were acquired.

Now the share was available for less than this purchase price, so it was easy to follow suit.

Thanks to the rookie investor for the nice investment tip,

I would be interested to know Inderes’ view when Solwers moves to the main list. For example, how would funds investing in small companies act, i.e., do they have the desire or are they even “forced” by their rules to buy a slice of Solwers.

Hmm, it’s difficult to comment on what would be the funds’ desire to buy a specific individual company. It certainly depends on how they view Solwers’ investment story and attractiveness as an investment target, which is subjective.

Yes, there are already small-cap funds on that ownership list, so in that sense, there doesn’t seem to have been any collective obstacle even before the main list transfer. I don’t believe it’s mandatory, as I can’t immediately think of a fund that would consist of all the companies on the list.

Yes, moving to the main list has the potential to improve recognition and liquidity, but liquidity is formed by many factors, and in my estimation, it cannot be changed by a mere list transfer. These other factors include, for example, the number of freely tradable shares and general attractiveness as an investment target.

Inderes could ask Solwers in their next meeting about the status of moving to the main list. Moving to the main list would bring visibility to the company and increase interest as an investment target. What is Inderes’ view on the additional costs this would bring to the company? Can Sitowise be considered the closest comparable?

Let’s ask! As far as I understand, it’s still being worked on, but indeed, no information about the schedule has been given. Regarding those additional costs, I believe we’re talking about a couple of hundred thousand annually, but I still need to confirm this.

If you’re thinking of a comparable company for the business on a general level, then Sitowise is indeed a good comparable, but based on that, one cannot pinpoint the direct effects of their different listing statuses on the cost structure.

Thanks for the information! The company states that planning is purchased upfront and paid plans may never be implemented. And thus, there is still demand even though construction is in a slump. You could also inquire if there are already clear signs of growth in planning. Offhand, Solwers is one of the first beneficiaries when construction eventually picks up.

I at least have a feeling that the next phase of, for example, housing construction has probably already been planned; the designers don’t seem terribly busy yet.

Solwers’ advantage is its very broad service offering: Starting from architecture. It includes structural and building services design, infrastructure design, project management, environmental and measurement services, and safety and supervision services. This means services can be offered for very different economic situations. As a result, the company has been profitable even in such a depressed time.

Let’s note this down, as I happened to spot it. I don’t follow the company, so I don’t understand why they only refer to Q4 figures and not the full-year results; is the reporting period somehow exceptional? A negative profit warning in any case at 6:00 PM on a Saturday evening – at least the management still has time for Saturday evening activities, though not on the “five to the sauna, six to the drunk tank” schedule Solwers Oyj: Sisäpiiritieto: Solwersin IFRS EBIT -liiketulos on ollut loppuvuonna 2024 odotettua pienempi | Kauppalehti

Aha, here too some strange slowdown has occurred in December, a bit like with Talenom. Should one be worried more generally!?

Q4 revenue realization was 21-22M€, whereas Inderes/Nordea had expected 21.8M€ and 22.1M€. Q4 EBIT will now be around 0, while Inderes/Nordea’s expectations were 1.5M€ and 1.2M€. Solwers prefers to report EBITDA, and there hasn’t been much mention of that in this context.

“Our order book is on a good footing, and our revenue has grown compared to the previous year’s reference period. The end of 2024 was burdened by one-off items such as changes in additional purchase prices, write-downs of uncertain receivables, and preparations related to a potential main list transfer. Also, the scarcity of billable hours in December and fierce price competition partly affected the profitability of the year-end.”

These are quite credible one-off explanations in themselves, but hopefully the “well-positioned” order book is, however, more profitable than what was realized in December. We will likely only see that in the next couple of quarterly reports.

Why does @Petri_Gostowski Solwers report such an EBITA from which depreciation of leased premises is adjusted, meaning rents are not fully accounted for? But those rents still have to be paid, or what is being tried to be conveyed with such a figure? Or have I misunderstood something?

“EBITA Adjusted EBIT excluding depreciation and impairments of intangible assets and leased premises = EBIT + depreciation of intangible assets and leased premises + impairments”

That EBITA is a very typical earnings measure for companies that make acquisitions and thus amortize purchase price allocations arising from these acquisitions (often referred to as PPA amortizations, which comes from purchase price allocation). Solwers, however, has mainly recorded intangible assets as goodwill in connection with acquisitions, so those PPA amortizations hardly arise.

I believe the company has ended up reporting EBITA because other players in the industry do so, and also due to that inorganic growth. Of course, I don’t know how the matter was considered in the companies back then, so this is just my own speculation

I myself encountered for the first time with Solwers such a way of recording lease liabilities, meaning they are recorded as intangible assets and thus are not conventional amortizations. I once asked the company’s previous CFO about this, and the practice was based on the fact that the right-of-use assets for premises were considered an intangible asset rather than a tangible one. In a way, I understand this; they don’t actually have tangible assets when they have the right to lease something, so those rights to use premises can be seen as an intangible right. However, this differs from how these are generally treated in financial statements and illustrates, in a way, the discretion present in accounting practices.

Based on that interpretation, the company’s EBITA thus differs from what it is for others. I have also written about this in a comprehensive report, or rather, about the fact that the EBITAs of industry players are not comparable. And you are absolutely right, rents must be paid just like by everyone else, and in my opinion, you haven’t misunderstood anything. That differing approach is simply not easy to notice unless one delves deeply into the matter.

Petri lowers the target price to €2.8 and changes its recommendation from ‘add’ to ‘reduce’ in its latest report.

“According to preliminary information provided by Solwers on Saturday, the company’s performance in the last quarter of 2024 has been weak in terms of results. Some of the factors behind this weak development are, in our estimation, related to a very weak operating environment and thus likely temporary. On the other hand, the recent economic news flow does not support expectations of a rapid recovery in market activity. Reflecting the forecast changes, we lower our target price to 2.8 euros (previously 4.20e) and our recommendation to ‘reduce’ (previously ‘add’). The high valuation of the share, together with increased indebtedness, in our opinion, create a weak return/risk ratio over a 12-month horizon.”

This kind of Saturday night fiasco should get one into some kind of IR Hall of Fame, as this is already championship-level fumbling. One shouldn’t dream of the main list just yet with this level of performance. There’s plenty of work to do, no matter what kind of EBITA adjusted for lease liabilities we’d use until the very end.

Petri’s warm-up for Solwers’ H2 report, to be published on Friday at 9:00 AM, is here

Reflecting the profit warning issued in February, the overall picture of the Q4 result is known, and based on it, the quarter has been weak in terms of figures. In line with the decline in profit, we predict the company’s dividend will decrease from the previous year. The company has not typically provided clear revenue or profit guidance, and we do not expect it now either.

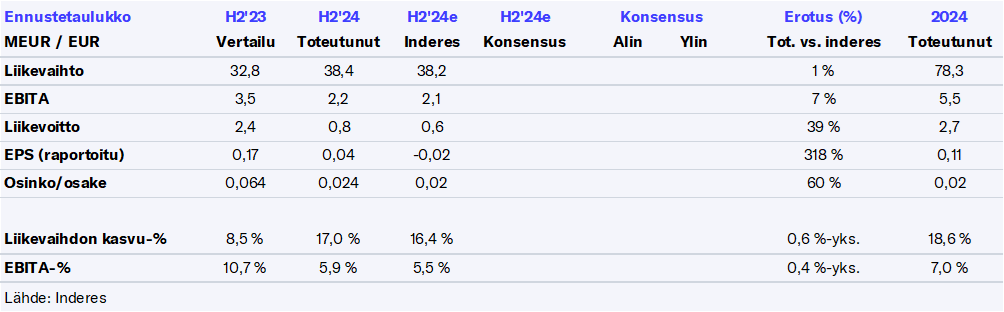

Full-year revenue totaled EUR 78.3 (66.0) million. Revenue grew by 18.6%, with annual growth of EUR 12.3 million.

EBITA was EUR 5.5 (7.0) million, representing 7.0% (10.7) of revenue

EBIT was EUR 2.7 (4.8) million, representing 3.5% (7.3) of revenue

Utilization rate was 79.9% (81.5%)

Equity ratio was 43.6% (46.4)

The equity ratio was higher than the medium-term target of over 40 percent, revenue growth was close to the 20 percent growth target, and EBITA profitability fell short of the medium-term target of 12 percent.

Earnings per share (EPS) was EUR 0.11 (0.32)

Net cash flow from operating activities was EUR 4.3 (4.7) million. The company’s cash reserves remain at a high level, enabling the implementation of the growth strategy through acquisitions.

Number of personnel at period end was 724 (635)

The implementation of the growth strategy through acquisitions continued, and six new operational companies joined the group: four in Sweden and two in Finland. In addition, the company acquired strategic expertise with a 33.3% minority stake in an environmental consulting company.

Decision made on geographical expansion to Poland and a country company established

The company’s Board of Directors proposes to the Annual General Meeting scheduled for April 15 that a dividend of EUR 0.024 per share be distributed, corresponding to a total of EUR 244,092.19.

CEO Stefan Nyström’s review

The year 2024 showed encouraging signs in the consulting and engineering sector, but a significant market turnaround is still awaited. Our order book improved towards the end of the year, and the utilization rate remained at a good level. Profitability, especially towards the end of the year, was affected by one-off costs and investments in future growth.

Solwers’ core business continued its good performance despite market challenges. Revenue grew by almost 19 percent, exceeding EUR 78 million. We are pleased to see activity picking up in Finland and investment operations slowly starting. We are particularly satisfied with the improvement in the performance of subsidiaries that have faced challenges in previous years.

Overall, the business environment remains more favorable in Sweden, and our Swedish subsidiaries generally have a positive impact on business.

Preparations for the transfer to the Nasdaq Helsinki stock exchange list have progressed well in 2024. The company’s Board of Directors carefully evaluates the transfer schedule and prevailing markets, ensuring that the decision is in line with the company’s long-term strategic goals and the interests of shareholders.

These are starting to show below the line

Group-level administrative expenses increased by EUR 1.2 million from the previous year. Most of this relates to development projects that are now in the finalization phase. We believe these investments bring added value to our business and are essential as our growth journey continues.

Other expenses include write-downs of doubtful receivables and the recovery of social security contributions related to the research and development (R&D) activities of one subsidiary, which negatively impacted IFRS operating profit by EUR 1.1 million. In addition, a significant customer who temporarily suspended the purchase of consulting services has affected the operations of three of our Swedish subsidiaries. The estimated impact is approximately EUR 0.5 million.

Here it is also in table format in relation to a year ago and the comparison period.

The cost structure presumably contains some non-recurring items, but on the other hand, other operating income was surprisingly high. I need to find out more precisely during the day what the figures include