I guess Solteq’s risks have been on the debt side. The strong cash flows of the past quarters and the refinancing of the aforementioned loan have significantly improved the situation in this regard.

I don’t really look at goodwill or intangible assets myself, as long as the balance sheet and cash flows are otherwise in order. None of the comparables have any fixed assets, but plenty of intangible assets, which can be very valuable. If there are old sins from failed software and these are written down from the balance sheet, quite often these have already been discounted into the share price well in advance.

Hopefully, Solteq’s positive momentum will continue also in the rest of the year. The CEO seemed quite enthusiastic about the outlook when asked, if one has watched the Inderes interview.

Around six o’clock, we get a notification. First, we remember that we have to make this a mandatory announcement, and almost immediately, another announcement comes:

A slight disappointment that the interest rate couldn’t be negotiated downwards. However, the debt level will come down and durations are at a better level, so the business risk will decrease regardless. We’ll go with this for now.

No, it’s not a hybrid, just a regular unsecured senior loan. I don’t know where I got the hybrid from, but the main thing is that you corrected me A lower interest rate was definitely hoped for and expected. Well, maybe when this new loan is restructured at some point.

Please tell me how this should be interpreted, or have I missed something? So, in the latest announcement, it stated the following…

“Solteq has achieved a significant position during the current year as a provider of software and expert services for the utilities sector in Finland. During 2020, the company has signed several delivery and service agreements, the combined value of which, including options, exceeds 22 million euros.”

Earlier in the year, similar deals were announced, and the matter was phrased as follows…

“Solteq Plc has signed delivery and service agreements worth approximately 8 million euros in total with two Finnish energy sector customers on March 31, 2020, and April 27, 2020. These agreements consist of delivery projects for the customer information system developed by the company and related options (approximately 2.1 million euros), as well as licensing fees for 4-5 years.”

These are apparently the same proprietary software. The only deals published are 13-14 million in sales plus 8 million in other smaller deals. Apparently selling very well.

Could this be one of the least traded stocks on the market? Even yesterday, I saw the trading volume was something just over 300 euros. The day started well again, with some lucky person wanting to maximize their trading fees and buying shares for three euros

Poor liquidity isn’t inherently a problem for a micro-investor like me.

Let’s ask about the Utilities side of things in more detail during the Q3 video, and how regulations affect it. I’m also interested in the potential in Sweden, how much customization it requires and how different that market is there. The company is currently in a quiet period, so I can’t ask for their outlook.

The margins are a bit uneven, so it does effectively curb the rise. The company seems to be heading in the right direction, but the debt burden is quite large, and there would probably be some write-offs on the balance sheet. However, the business cash flow is at a good level, and the operating profit for the beginning of the year has increased by almost 40%.

Those loans are no longer an issue. They’ve been renegotiated, and with improved profitability, free cash flows have significantly increased. I’m sure they’ll be paid off at a nice pace, which in turn will further reduce the risk level, and interest expenses will drop quickly (6% interest).

I’d just say the return potential looks truly excellent. The company’s growth in the COVID year has been among the best compared to its peers, and profitability has improved rapidly. The joker in the deck is its own software operation, which has really picked up steam. There’s no need to fully focus on low-margin consulting. Yet, the company seems to be the most affordably priced of all.

The stock is flying under the radar. You won’t see it even if you’re standing a meter away

Loans aren’t an issue now, but it would be nice if they didn’t exist

I’m also interested in Solteq’s own software development; there’s always the possibility of them coming up with a good product that takes off. I see similar potential in Siili, which is why I have both in my portfolio.

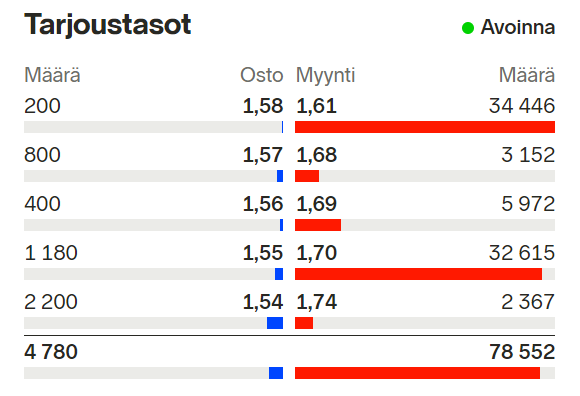

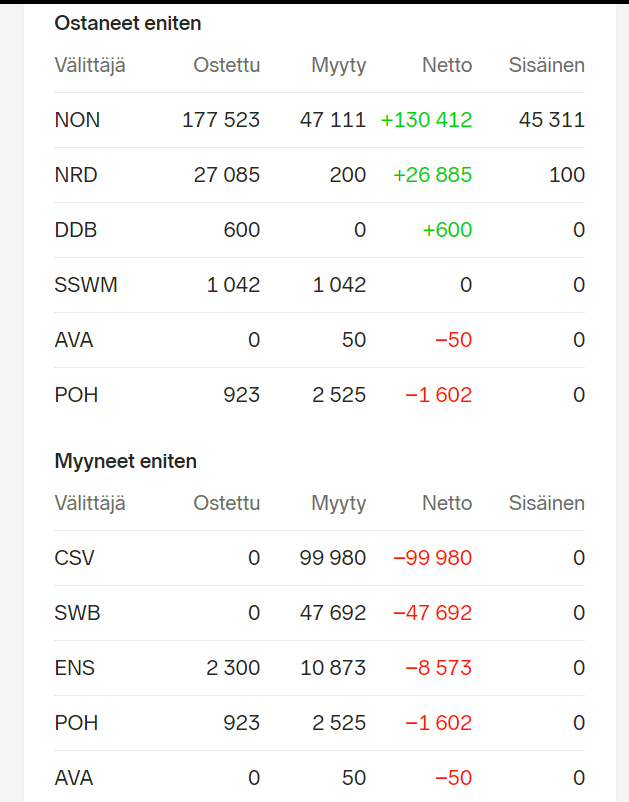

Nordnet users are taking over as Swedbank (SWB) and Credit Suisse (CSV) are selling off big time. Now the largest volume in the last 3 years with over 200k shares, of which 177k shares have gone to Nordnet accounts alone

This was mentioned in the interview. Most operators have not yet made their systems compatible, and Solteq has a working product for them. I’m sure customers will soon be overflowing, which the strong order backlog this year already hints at.

Sweden apparently has the same thing ahead at some point, and the market is three times larger than in Finland.