Recently, whenever the “man in the leather jacket,” i.e., NVIDIA CEO Jensen Huang, has highlighted trending companies, the returns on those stocks have been outrageous. Most recently, he was hyping up ServiceNow.

So, what does the company’s future look like in the midst of the AI revolution? If Huang is to be believed, it looks bright. Or is it different this time, and is Huang’s vision wrong? Let’s start, however, with what problem the company actually solves in the world.

History

ServiceNow was founded in California, USA, by Fred Luddy in 2003. At that time, however, the company went by the name Glidesoft Inc. until 2006. For the first couple of years, founder Fred Luddy was actually the sole employee, and it wasn’t until 2005 that the first five employees were hired. By 2007, ServiceNow had already turned its business cash flow positive with a revenue of $13 million.

ServiceNow went public in 2012 with a valuation of $210 million, when the previous year’s revenue was just under $100 million.

The milestones of the current decade have been significant partnerships. In 2023, the company announced it would begin collaborating with NVIDIA to integrate AI services into enterprise support software. In early 2026, partnerships were further announced with Anthropic and OpenAI. The goal is to bring their Large Language Models (LLMs) into ServiceNow’s AI platform.

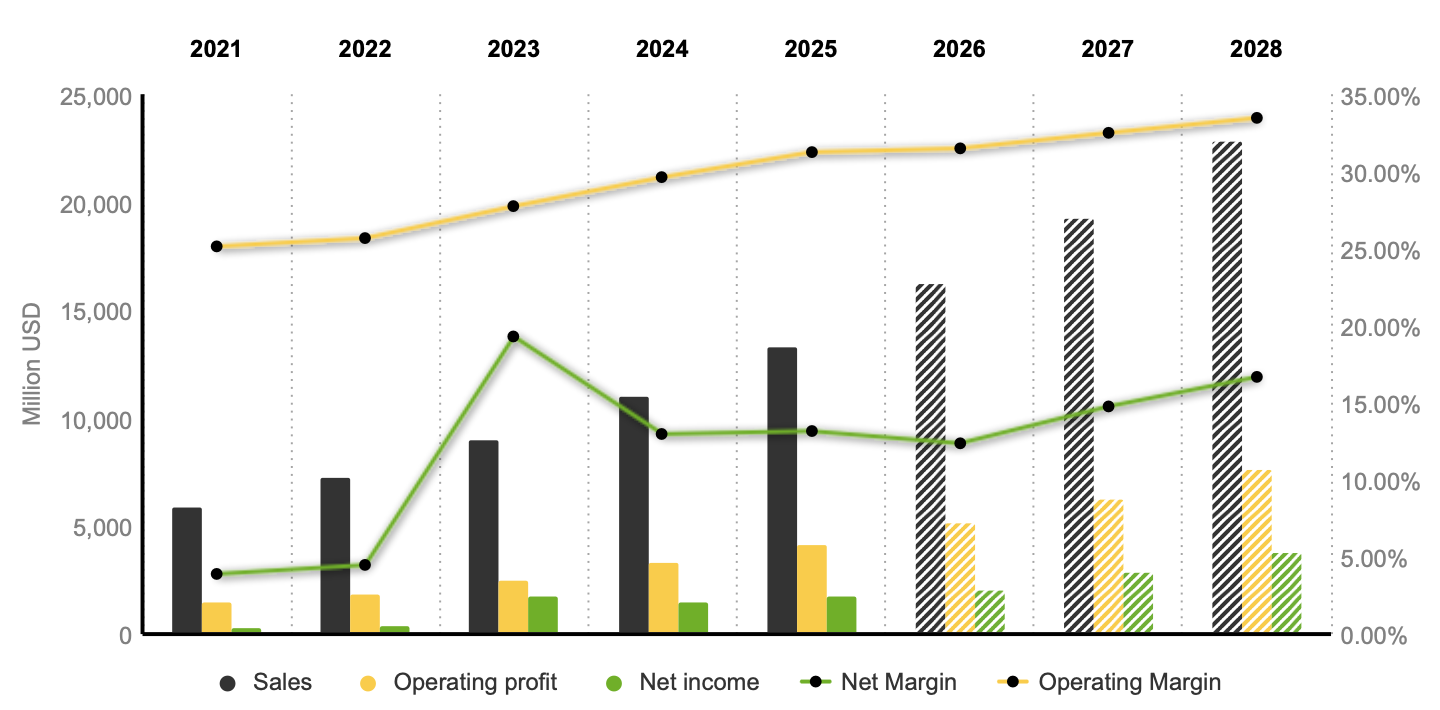

Coming to the present day, the company’s revenue has grown to $13 billion, and the operating profit for last year was over $4 billion. At its peak, the market capitalization hit $230 billion but has now dropped to $93 billion.

Business

All larger companies have a need to streamline processes, and even a small time saving accumulates quickly into a significant financial saving if the processes are repeated numerous times daily. ServiceNow has built a platform intended not just to store data or process tickets, but to model and automate these constantly recurring tasks: approvals, support requests, solution automation, etc. In practice, the platform helps companies manage everything from IT support to HR processes.

Today, however, the business is also strongly linked to AI, and ServiceNow is considered a kind of “coordination layer” between AI agents and enterprise systems. Artificial intelligence vastly increases the number of automatable processes, but in addition to AI, companies also need an audit trail, compliance logic, integrations with legacy systems, and workflow orchestration. So, while many AI startups might be able to create a chatbot, an AI agent, or a Co-pilot-style UI, this is not yet enough for the large-scale utilization of AI in larger corporations.

Valuation

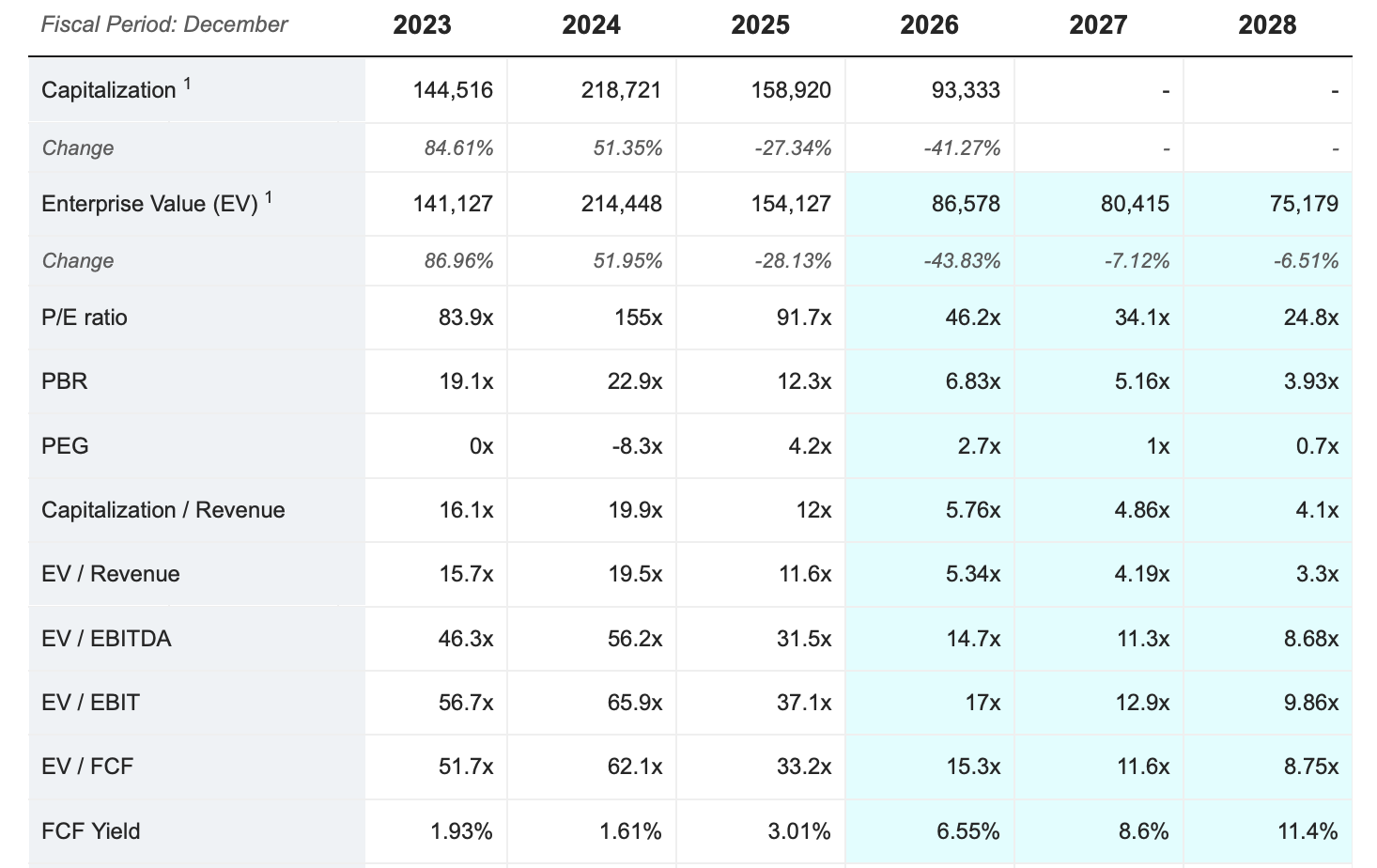

In the spring of 2026, the stock has been hit hard, similar to other software and SaaS companies. It has come down about 62% from its peaks, meaning the stock is hovering around $90 USD, whereas just over a year ago, investors were paying upwards of $230 USD at the highest. The 2024 multiples were truly in the range of EV/S 20x, P/E 155x, EV/EBIT 66x, and FCF yield 1.6%, meaning a lot of good news was priced in. Since then, AI disruption fears have weighed down the entire sector, but the core question for ServiceNow is whether a company that actually benefits from the AI revolution has been thrown out with the bathwater.

At the current price, the valuation looks considerably more reasonable than it did a couple of years ago. Based on last year’s earnings, the P/E is around 53x. EV/S has dropped to approximately 6.5x, which is nearly a 60% discount compared to its historical median. The Forward P/E is now only about 20x, the PEG ratio is under one at 0.81, and EV/FCF is around 19x. Thus, the current valuation is no longer outrageously expensive, at least, but it certainly requires earnings growth to remain strong.

Outlook

The momentum has continued to be quite strong, as Q1 2026 subscription revenues grew 22% year-over-year to $3.67 billion, once again exceeding the upper limit of their own guidance. Nearly 40% more new contracts worth over a million dollars were generated in Q4 2025 than a year earlier, and the group of customers with over $5 million in ACV (Annual Contract Value) grew by about 20%.

The traction of AI products has also started to show concretely. The Now Assist AI package is on track for $1.5 billion in annual ACV in 2026, which is 50% higher than the original target. Now Assist contracts worth over a million dollars were signed in Q1 at a rate over 130% higher than a year earlier.

Guidance for full-year 2026 subscription revenues is $15.5–15.6 billion, meaning growth is still expected to be around 20–21%. Additionally, cash flow is strong, and the board authorized an additional $5 billion share buyback program. On the other hand, in typical US company fashion, stock-based compensation is quite generous, which would dilute shareholders if shares were not also being bought back simultaneously.

Risks

Of course, it’s not all sunshine and rainbows. Firstly, AI disruption could hit ServiceNow itself. If future AI agents are capable of replacing workflows without a separate orchestration platform, ServiceNow’s role as a coordination layer will diminish, but at least for now, the trend has been the opposite.

Secondly, competition is intensifying. Salesforce, Microsoft, and numerous smaller AI-native startups are all targeting the same enterprise budgets. ServiceNow’s advantage is its deep integration into customers’ IT ecosystems and long-term contracts, but the competitive pressure is real.

In any case, as things stand, AI is more likely to increase the need for managed automation. We’ll have to wait and see if Huang is right with his vision this time as well. I don’t own ServiceNow yet, but I’ve at least added it to my watchlist.