Ruotsin SCA eli Svenska Cellulosa Aktiebolag nostaa havusellunsa hintoja Euroopassa. Onko tässä jääräpäisenä tervaskantona alettava uskoa, että merkkejä ![]() markkinan paranemisesta on ihan oikeastikin?

markkinan paranemisesta on ihan oikeastikin?

24 tykkäystä

Kappas, yli 6% lisää.

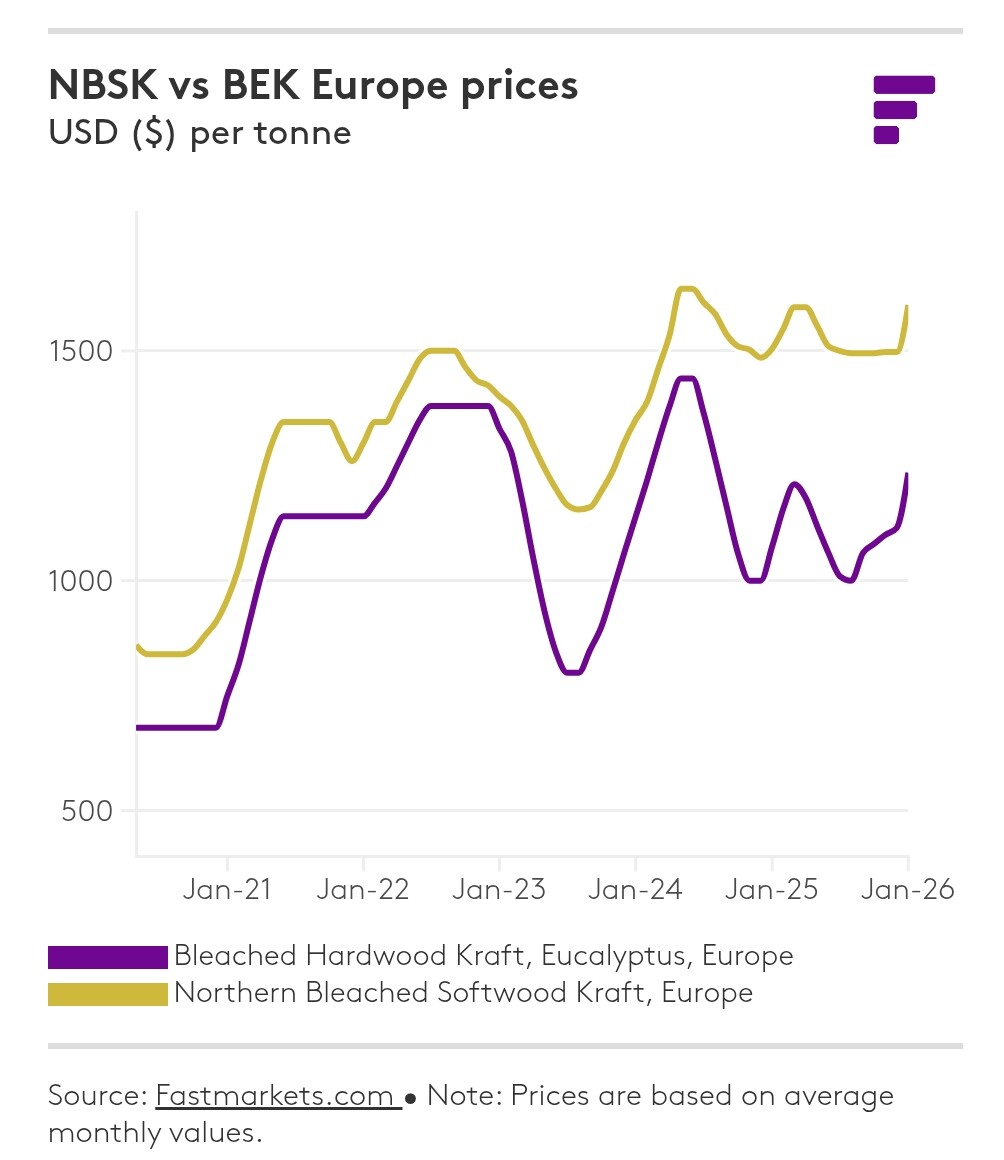

Fast Marketsin mukaan jo aiemmin joulukuusta tammikuuhun hintataso olisi noussut 1500->1600 usd/t

- Press release

- 13/02/2026, 08:32 am

SCA will increase the price on NBSK pulp (Northern Bleached Softwood Kraft) in Europe. The new price will be 1,710 USD (+100 USD), effective for March deliveries and invoicing.

CORRECTION: SCA to increase NBSK price – SCA https://share.google/tUumcQ06Hhe19dGXD

12 tykkäystä

Olen täältä palstalta aiemmin ymmärtänyt, että nuo Euroopan noteeraushinnat on lähinnä viitteellisia, kun valtaosa myydään “alennuksella“. Ja Euroopan todellinen hintataso olisi lähellä Kiinan tasoa. Siellähän hinnat ei ole juurikaan liikahtaneet.

9 tykkäystä

Ilmankos tuossa linkatussa Fast Marketsin jutussa puhutaan NBSK spotista Euroopassa hyvin erilaisesta tasosta spottimarkkinoihin liittyen…

Fastmarkets assessed pulp, northern bleached softwood kraft (NBSK), spot, dap Europe, at $730-745 per tonne net in January on February 10, up by $10-15 per tonne from the December level of $720-730 per tonne. This was based on business transacted on a euro basis more or less unchanged from December, but the exchange rate pushed the dollar level upward.

7 tykkäystä

Metsä Groupin Joutsenon sellutehtaalla tuotantoseisokki

Talvikausi päättyy pikkuhiljaa, ja pelko jäätymisestä katoaa, niin voidaan tuotanto ajaa alas odottelemaan parempia aikoja. Ei näytä sellubisneksen tulevaisuus kovin hyvältä Suomessa.

9 tykkäystä

Seuraamme markkinatilannetta ja päätös tuotannon ylösajosta tehdään sen pohjalta.

Mikäli itse olisin työntekijänä tuolla, niin alkaisin kyllä tuommoisen lauseen jälkeen katselemaan töitä ihan pysyvästi muualta ![]() Taisi löytyä se bingo siihen seuraavaan pysyvästi suljettavaan tehtaaseen.

Taisi löytyä se bingo siihen seuraavaan pysyvästi suljettavaan tehtaaseen.

5 tykkäystä

Alkaa olla samoja merkkejä Joutsenossa kuin oli kauan sitten UPM:llä Kajaanin paperitehtaalla ennen lopullista lakkautusta.

12 tykkäystä

Kuitupuun hinta Suomessa on taas pitkästä aikaa hitaasti noussut 2-4 viikkoa. Pohjat olivat noin 20-25% korkeammalla tasolla kuin hinnat ennen Ukrainan sotaa. Ja tämä tilanteessa, jossa 1-2 sellutehdasta seisoo kokonaan tai osittain kysyntä/kannattavuusongelmien takia. Kun puun hinnasta ei tule tämän enempää apua, niin ei näytä hyvältä sellutuotannon tulevaisuus Suomessa. Kuka kolmesta antaa ensimmäisenä periksi ja sulkee yhden sellutehtaansa?

12 tykkäystä

UPM puukaupasta vastaavat on tietyillä alueilla lomautettu pariksi viikoksi. Lomaviikot on saanut itse valita. Kertoo ainakin sen että puu ei liiku.

2 tykkäystä

https://view.info.upmmetsa.fi/?vawpToken=AJFHNCFNEYUUNP6SWPDLXH7WT4.510007

Tällainen viesti tuli juuri tänään, kertoo samaa tilanteesta.

2 tykkäystä

@Antti_Viljakainen miten näet tämänpäiväisen UPM:n transformaatiojohtajan nimityksen? Valmistautuvatkohan paperiliiketoiminnan irroittamisen myötä tulevaan muutostarpeeseen vai miten näet? Mielenkiintoista myös, että transformaatio ei ole osa strategiatiimiä, mutta se nyt on kuriositeetti.

5 tykkäystä

Puu ei liiku kun yhtiöillä on hakkaamatonta talvileimikkoa paljon ja syy siihen koska talvet on tälläsiä niin metsään ei ole koneella päässyt. Varsinkin suoalueet/ kosteat. Sen maan pitäs olla lumessa ja jäässä että sinne voisi mennä. Eli reserviä on kasvamassa. Eiköhän toi keväällä vähän piristy.

8 tykkäystä

Suoraan sanottuna ajattelin, että yhtiöön/johtoryhmään palkattiin strategiajohtaja vähän modernimmalla tittelillä, mutta näköjään kyseinen tuoli olikin jo täytetty. Eipä tästä nimityksestä suurempia näkemyksiä herännyt tässä vaiheessa. Nopeisiin muutoksiin en usko jo tiedotettujen suunnitelmien lisäksi, mutta pidemmällä tähtäimellä UPM:n portfoliopelissä on toki mahdollista transformatiivisiakin siirtoja tehdä.

Transformaatiojohtaja on muuten 13 jäsen UPM:n johtoryhmään ja oletettavasti vielä yksi on tulossa lisää, kun Korpeisen CFO- ja Energia -hatut jaetaan kahdelle henkilölle. Yhtiöitä voi toki johtaa monella tapaa, mutta omaan makuun varsin raskaan oloinen kokonaisuus UPM:n monialarakenteesta huolimatta.

13 tykkäystä

Kiitos näkemyksistä! Hyvä huomio toi johtoryhmän leveys. Toivoa sopii, että uusi transformaatiojohtaja auttaa toimitusjohtajaa suoristamaan rakennetta nyt, kun muutenkin on paperiliiketoiminnan divestointia ja vaneribisneksen strategista arviointia.

4 tykkäystä

Henkilöstön vaihtuvuus on ilmeisesti ollut myös kovaa ainakin joillain ostoalueilla. Itse tein puunkaupan syyskuussa 2025 ja yhteyshenkilö vaihtui 3 kertaa 6 kuukauden aikana. Näin ei ole ollut ennen.

2 tykkäystä

On kyllä tosi leveä. Oma kokemus työelämästä on, että yli 7 hengen kokoukset alkavat mennä tiedotustilaisuuden puolelle, ei niissä enää päätetä mitään. Yleensä johtoryhmässä on ollut TJ, tuotekehitysjohtaja, markkinointijohtaja, myyntijohtaja, huoltotoiminnan johtaja, tuotantojohtaja, HR-johtaja

Toki UPM on monialayhtiö, mutta silti.

4 tykkäystä

Poikkeuksellisen varhain tullut kevät pakottaa metsäalan yritykset keskeyttämään osan korjuutöistä ja jakamaan lomautusvaroituksia.

4 tykkäystä

Eli ei isoja muutoksia puuraaka-aineen hinnassa viime kuusta, mutta pitemmällä aikavälillä alas.

Aamulla luin myös, että maakaasun hinta tänään 35 % ylös. UPM:n Leuna on käsittääkseni kytketty alueen energiaverkkoon, jossa vähintään yhtenä pääpalkkina maakaasu. Sen lisäksi, että Umpin Leuna käyttää oman laitoksensa puupohjaisia sivuvirtoja. Pohdiskelin, että mitenköhän Umpin Leunan katteisiin ja yleensä toimintavarmuuteen vaikuttaa tällainen riippuvuus fossiilisesta kaasusta, jonka hinta pomppii sinne tänne? Onkohan @Antti_Viljakainen tietoa tästä asiasta tai tullut missään esiin?

9 tykkäystä

Tuli mieleen myös tämä kaasun hinnan mahdollinenvaikutus kierrätyslaatuihin(kartonki)? Oliko näin, että edellisessä energiakriisissä etenkin eurooppalaiset WLC-valmistajat ottivat osumaa kustannusrakenteen reilusta pompsahtamisesta, joka johti ensikuitukartongin kasvaneeseen kysyntään?

2 tykkäystä

Itellä ollu kans mieles, että joko nyt kohonneet hinnat, ja mahdollinen energiakriisi alkaa olemaan viimeinen niitti euroopan yksittäisille perheomisteisille paperitehtaille ?

3 tykkäystä