Vuosi on lyhyt tarkasteluväli, mutta teen silti lyhyen päiväkirjamerkinnän kuluneesta “tilikaudesta”. Onpa sitten tällainenkin tallessa, jos tekee mieli joskus katsoa menneisyyteen. Saa tätä ketjua tietysti muutkin käyttää, jos haluaa vetää omaa vuottaan yhteen, tuuletella hyviä suorituksia tai kirota huonoja. ![]()

Aluksi muutama yksittäinen osakepoiminta, hyvä ja huono. Vuoteen lähdettäessä ylipainotin Nokiaa selvästi (30% salkusta), ja tuo osoittautuikin varsin hyväksi liikkeeksi, kun helmikuussa markkinan pessimismi alkoi purkautua. Sittemmin Nokian paino salkussa laski ihan normaalitasolle, ja vähän q3-raportin jälkeen lähtivät kokonaan salkusta. Negarin tullessa siirtyisin mahdollisesti takaisin ostopuolelle.

Toinen ylipainotus oli Danske Bank, pankkia koskevan kohun velloessa. Tässä aliarvioin selvästi fundamenttien jarrutusvaikutuksen, momentumin merkityksen ja yliarvioin itseni lyhyellä aikavälillä, ja otinkin komeat turskat kurssin syöksyessä yhä syvemmälle. Onneksi ostot tein kuitenkin muutamassa erässä, enkä kerralla ensimmäisellä ostohinnalla (170DKK). Dansket saivat lähteä salkun vuosisiivouksen yhteydessä.

Kolmas ja vuoden viimeinen ylipainotus oli Harvia, jonka ostot tein kahdessa erässä lokakuun aikana. Näitä keventelin marraskuun lopussa kurssin korjattua, mutta edelleen osa on salkussa, ja nykyisillä hintatasoilla olen ehdottomasti ennemmin osto- kuin myyntipuolella.

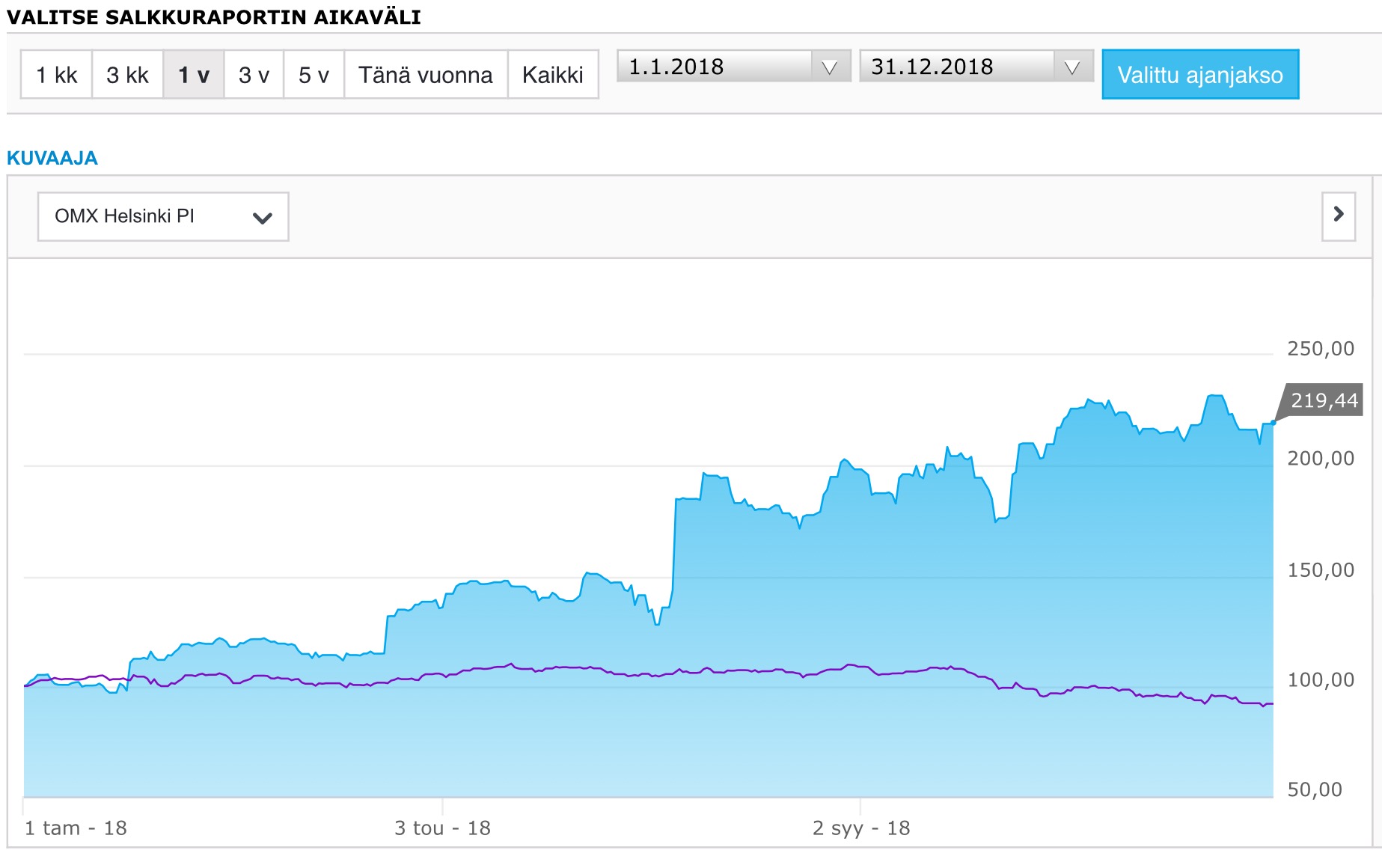

Salkun tuotto vuoden alusta oli 5,66%, mikä itsessään on jo ihan ok lukema, mutta varsinkin indeksiin verrattuna tuotto oli jopa erinomainen.

Katseet vuoteen 2019

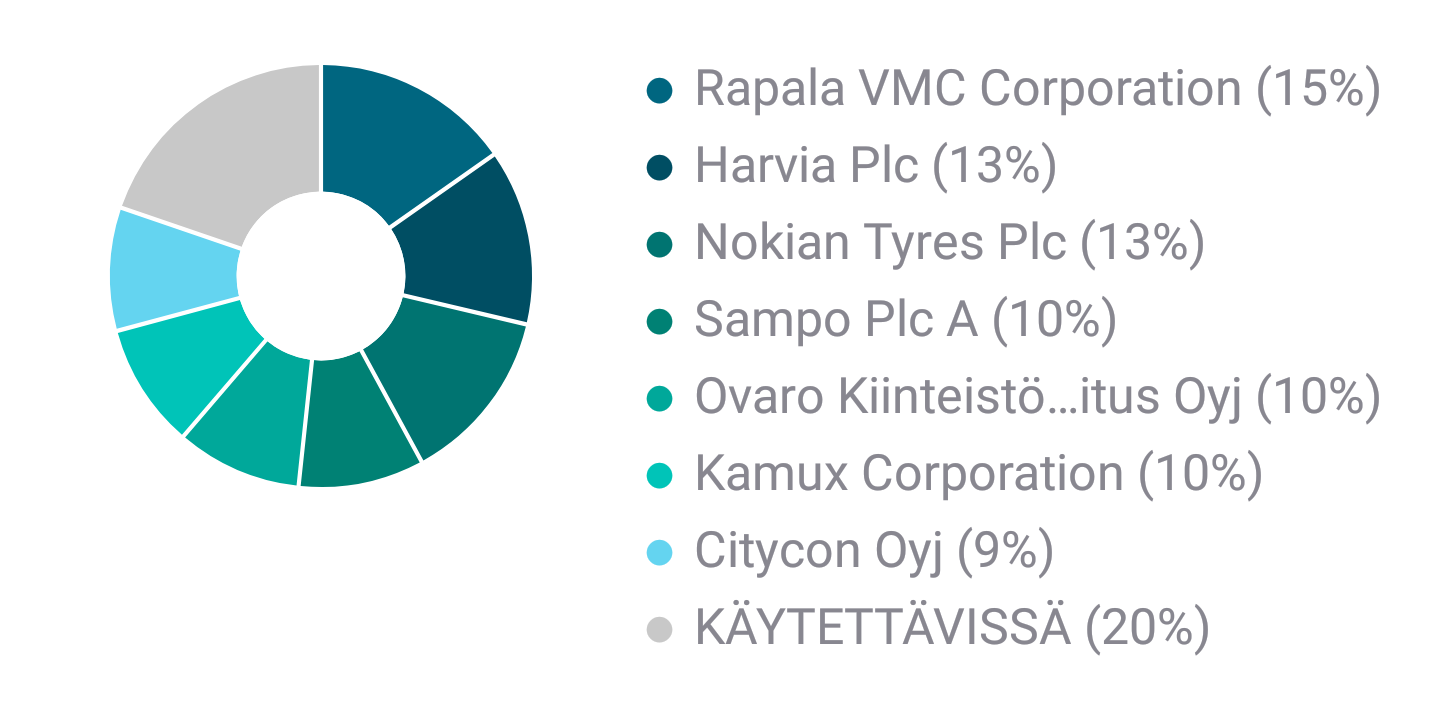

Jatkan ensi vuoteen samoilla teeseillä kuin lähdin tähänkin. Perusteollisuutta ja muuta syklisempää ei ole kiire kauhoa salkkuun, vaikka kieltämättä arvostukset näyttävät monen yhtiön kohdalla huomattavasti järkevämmiltä kuin vuosi sitten. Näistä metsäyhtiöt kiinnostavat ehkä eniten, mutta ei ihan näiltä tasoilta vielä. Salkku on siis tavallaan viritetty vähän puolustuskannalle hankkimalla pääosin sellaisia yhtiöitä, joiden oma kehitys ei ole niin vahvasti sidoksissa maailmantalouden kehitykseen vaan ennemminkin yhtiön sisäisiin asioihin. Aivan kaikki valinnat eivät kuitenkaan tällaisia ole, vaan esimerkiksi Nokian Renkaat on alttiimpi yleisen taloustilanteen kehitykselle. Hinta on kuitenkin ollut sellainen, että sillä voi mielestäni näin laadukasta liiketoimintaa omistaa. Citycon, vuoden viimeinen osto, taas tuntuu halvalta, ja aivan kaikki tietävät kyllä kivijalan alennustilan - se lienee hinnoiteltu jo vähintäänkin tehokkaasti. Tässä on optiona myös Katzmanin ostotarjous, mihin itse todennäköisesti tarttuisin, jos se tuolta +1,80€ tasoilta tehtäisiin. Tässä vielä koko salkun sisältö vuoteen lähdettäessä:

Salkun ulkopuolelta tarkkailussa ovat mm. metsäyhtiöt, Nokia, Tokmanni ja Rovio. Myös kaikkia omistamiani yhtiöitä olen valmis lisäämään hintojen laskiessa edelleen.

Oikein hyvää ja tuottoisaa uutta vuotta 2019 kaikille palstalaisille ja Inderesin toimistolle.