How do people own the company/are there any intentions to buy?

- in portfolio

- considering

- don’t see potential

0

äänestäjää

How do people own the company/are there any intentions to buy?

In the portfolio! First purchases with euros ![]()

Scanfil delivered an impressive performance again in Q1. Achieving their guidance for this year would also be a tough feat, although I remain somewhat skeptical in this regard, considering general economic data. From a big-picture perspective, the results of a single year do not have a transformative impact, and Scanfil’s medium-term outlook remains favorable, with their competitiveness intact. Additionally, I would be quite surprised if the company didn’t also make a reasonably priced acquisition within 1-2 years to accelerate growth.

It was already evident that the manufacturing of network equipment had slowly started to recover. Perhaps 5G is doing so well at the moment that visibility is relatively good.

This has been a burden for a longer time, and other segments have been driving growth. Perhaps the parts are changing.

It’s probably a good sign when the management team is shopping.

Here’s a link to comments on Scanfil’s Q1 report in video format, and a discussion about Scanfil as a company, its market position, and its general situation. Both are from Inderes’ YouTube channel ![]()

The CEO had transferred 110k shares.

And on the same day, two board members had both bought 55,000 shares. Quite an interesting maneuver.

A slightly larger market-making operation for an illiquid stock. And a slightly larger bathroom renovation. ![]()

So the shares went to the Takases, the two largest owners, who own nearly a third of the entire company. 100,000 shares is a rather small amount for them, but it keeps the company more tightly controlled.

To clarify, Harri and Jarkko own just under a third. There’s also a large number of other Takases as main owners.

Dividend tomorrow €0.15/share ![]()

I had Scanfil in my portfolio before the corona crash, and still do. Below are some clarifying questions:

Does Scanfil work extensively with companies in the 5G sector, e.g., Nokia and Ericsson? And how is the collaboration divided between these two, for example?

More about customers. Has customer cyclicality changed over the years?

I still think the stock’s valuation is affordable. P/E is 12 and P/B is under 2. The dividend is around three percent. Could Scanfil become a publicly traded company paying a fair dividend in some year?

Scanfil may have fared better than others during the corona crisis. Would there be opportunities for acquisitions in these uncertain times?

So, if we delve into the company’s history, it was originally largely about network equipment manufacturing. This is also indicated by the fact that a large part of the old management has a background with Nokia. Over the years, and especially after the acquisition of Partnertech, sales are divided very evenly among five segments. But yes, Nokia and Ericsson have been among the biggest customers, as well as Kone, ABB, and similar.

Indeed, these numerous different segments balance out cyclicity. Network equipment deliveries have been low for years, but other segments have supported growth. A similar situation would have been catastrophic for results at some point in the past, but development evolves. Compare the situation, for example, to Incap in terms of customer dependence and the extent of the factory network, and the risk profile is somewhat different.

Regarding that skewed concept of dividend distribution, it’s difficult to please Finns :face_with_raised_ebrow: The company has invested heavily in growth and allocated a significant portion of its earnings to growing the business. Over this period, a quick glance shows that the dividend has almost quadrupled while the payout ratio has remained very low. A long-term shareholder receives a 20-30 percent return on their 60-70 cent shares based on their purchase price, not to mention hundreds of percent in capital appreciation. So, in terms of total return, the company is one of the best-performing stocks, even if it doesn’t get much media attention.

Scanfil has long-term customers, who make up a rather large portion of their customer portfolio. More information about this has been provided in the report.

The company now has an 8-year history of increasing dividends, so why wouldn’t the dividend also increase at some point, given that the business operations and future prospects are on a good footing.

You can download Inderes’ comprehensive report on Scanfil from this page. It’s worth reading through @materia89 ![]()

You’ll find a lot of information about the business operations and the company in general!

@Antti_Viljakainen had already linked the report to this discussion earlier ![]()

Amen to this. Scanfil has shown its ability to invest capital with a 15-20% expected return, and the industry dynamics (organically growing business, industry structure supporting M&A) offer good opportunities for this in the future as well. It would be against the interests of shareholders to pump up the dividend payout ratio and simultaneously weaken the investment capacity (i.e., equity needed in exchange for debt availability), considering the prevailing framework. Very few investors, however, can achieve such returns with their investments in the long term, so it’s better to leave the capital to be allocated by the proven management/board within the company. Of course, nothing prevents maintaining a steadily rising payout by increasing the dividend by a cent or two per year (which would likely also support the valuation) while patiently scouting for good investment targets, if earnings development allows this.

For example, before the PartnerTech acquisition, Scanfil’s equity ratio was over 70% and its net gearing was clearly negative. However, the total return for shareholders would have been much smaller over the last 5 years than what was realized, if the balance sheet had not been allowed to strengthen to those levels and the company had started paying out large dividends earlier.

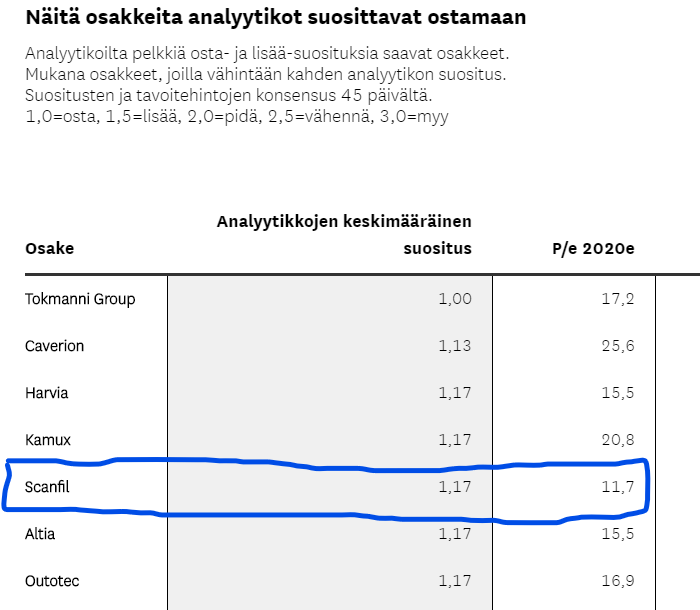

Overall, Scanfil has received very good recommendations from analysts.

Scanfil sells one of its subsidiaries in China. This is expected to slightly reduce revenue (approx. -15 MEUR) and adjusted operating profit (approx. -1 MEUR). A one-off operating profit of approx. +11 MEUR is expected in Q3/2020.

Refined guidance is a positive signal; corona will not cause a negative impact. Inderes’ target price, given current key figures, has been set quite generously on the low side, in my opinion.

Here’s a quote from analyst @Petri_Gostowski’s quick comment:

"Scanfil announced yesterday that its board of directors has decided to sell all shares of its subsidiary Scanfil (Hangzhou) Co., Ltd, located in Hangzhou, China, for a purchase price of 18.4 MEUR […].

Scanfil (Hangzhou) Co., Ltd is a factory focusing on sheet metal mechanics, with a turnover of 29 MEUR and an operating profit of 2.2 MEUR in 2019. The purchase price corresponds to a relatively modest EV/EBIT multiple of approximately 8x, which is below Scanfil’s own valuation multiple."

Out of curiosity, I ask how Inderes was able to calculate or estimate the subsidiary’s purchase price of 8x EV/EBIT multiple based on the information in Scanfil’s announcement?