Portfolio today 104,500.

To the original question.

I originally started saving and investing sometime back in 2005. I had landed a permanent job where I still work. The salary was reasonable for a young man, mainly due to shift work. Since then, the job description has changed several times. However, the employer is still the same.

At that time, using an inheritance I received (I think it was around €8,000), I opened a savings insurance policy (säästövakuutus). I saved something like €100/month into it. The portfolio contained completely idiotic funds. Some expensive proprietary OP funds like Prospering Middle Class, America, Super Note blah-blah-blah—whatever they were. And then Russia. I didn’t understand anything about investing. I put all sorts of things in there as long as it had a fancy name. Money did accumulate, and there were some returns. I don’t have any records from that time. Occasionally, I withdrew money for larger purchases. Mainly when cars were swapped. I also got to live for several years in an estate-owned apartment almost for free, which allowed for more savings. Man, if only I had had some understanding of where it’s worth putting that money. Sometimes a year would pass without me checking my investments; at other times, I was more interested. But it never occurred to me that one could actually learn about investing from somewhere!

Life situations changed. I found a wife, we had kids, we got a puppy. We bought a terraced house, the down payment for which was taken from the savings insurance again. We swapped the car for a bigger one again. Down payment from the savings insurance. We sold the house. We got almost the purchase price back ( this was the first lesson in real estate investing) and we made a contract to have a detached house built. We took on a semi-insane amount of debt. Again, we dipped into the savings insurance.

this was the first lesson in real estate investing) and we made a contract to have a detached house built. We took on a semi-insane amount of debt. Again, we dipped into the savings insurance.

We paid off the mortgage for the detached house in a way that life wasn’t otherwise very lavish. We flew abroad once a year, plus quite a bit of domestic travel by car driven by hobbies. Swapped cars again and dipped into the savings insurance. The house was lovely. Just what we wanted. Everything in life was pretty great, except the dog died  .

.

The savings lived their life in the insurance wrapper, where they had accumulated to about €20,000. One cannot, of course, speak of compound interest effects when the savings insurance was used as a cash fund. Nor had much else been invested there, as the money went into the foundations. The rest belonged to the bank.

Then a bomb dropped  . On Ukraine. At that time, I had been following my investments in some way (I still didn’t understand anything), and the Russia fund had performed well. I had increased it to a clear overweight in my portfolio. Then the fund was closed. No one knew what was happening. I waited and watched. The fund, which I recall was worth about €3,400 in my ~€20,000 portfolio, started showing a value of €2.2. (Or something. This is just an illustrative example.) Other rates probably plummeted drastically at the same time, I don’t remember that well. So the blow was quite significant! OP announced that the Russia fund (

. On Ukraine. At that time, I had been following my investments in some way (I still didn’t understand anything), and the Russia fund had performed well. I had increased it to a clear overweight in my portfolio. Then the fund was closed. No one knew what was happening. I waited and watched. The fund, which I recall was worth about €3,400 in my ~€20,000 portfolio, started showing a value of €2.2. (Or something. This is just an illustrative example.) Other rates probably plummeted drastically at the same time, I don’t remember that well. So the blow was quite significant! OP announced that the Russia fund ( ) would be closed and all activities regarding it would end. I felt that 17% of my savings were practically stolen. That was the investor’s risk and the worst possible scenario that can come true. It taught me a lot of caution, and I guarantee and underline that I will never have anything to do with Russia (sic) again. And this isn’t just because of my own financial losses.

) would be closed and all activities regarding it would end. I felt that 17% of my savings were practically stolen. That was the investor’s risk and the worst possible scenario that can come true. It taught me a lot of caution, and I guarantee and underline that I will never have anything to do with Russia (sic) again. And this isn’t just because of my own financial losses.

My biggest mistake as an investor is that I didn’t study the matter at all when I started. The second biggest, and partly due to the first, is that I trusted Russia.

Then another bomb dropped . The second one. Divorce. That lovely detached house and the kids went up for sale (wait, what the hell?! No, I didn’t have to sell the kids. ) Despite the difficult situation, this real estate deal went surprisingly fast, and we even got our own back from it. Maybe a few thousand on top.

I moved into a rental and continued working at the same firm. I paid an equalization payment to my ex-wife. I paid off the rest of the car loans and started with a bit of a clean slate. I was left with €62,000. I terminated that eternal and expensive savings insurance. I started studying investing. I opened an equity savings account (OST) and a book-entry account (AOT) at the bank. I opened a new savings insurance because I value the ability to modify the content as I please, depending on the situation.

I invested my assets into these three.

My investment strategy:

Keep the size of the savings insurance at about 70% of total investment assets. This is the fundamental part of my investments.

OST 10%: This is the part formed by domestic companies, hopefully resistant to market volatility.

AOT 20%: This is where quick moves and profits are made (if they are). This is where world politics and trends are followed. The turnover rate of this portfolio is definitely the fastest part of my entire portfolio. It contains ETFs and stocks by theme. Commodities, small caps, etc. This is where the highest volatility and fastest turns happen.

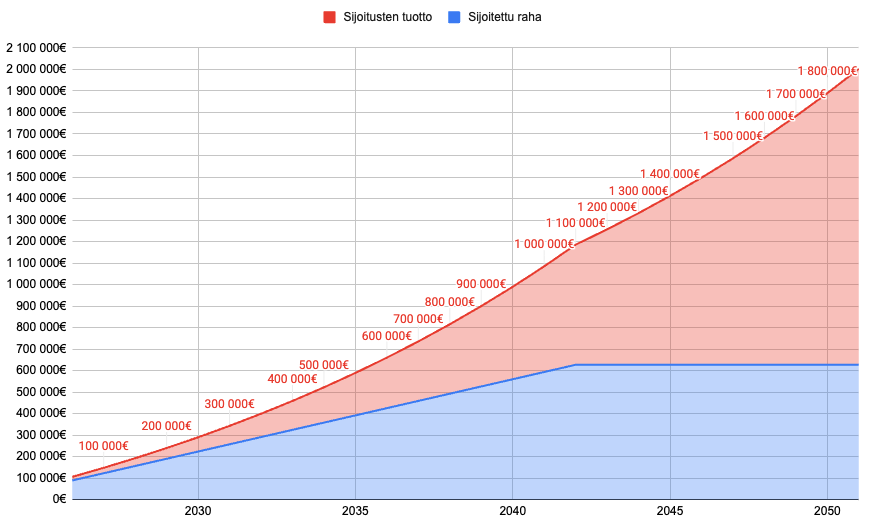

Nowadays, I aim to save about €800 a month for investments. My goal would be to grow the pot by about €10,000 a year. However, the last few years have been good for returns, so €62,000 grew to €77,700 in a year, and that again to €95,000 the following year.

Now the market has been favorable again, and I was finally able to write my own story in this thread.

Albeit in the singular. For now.