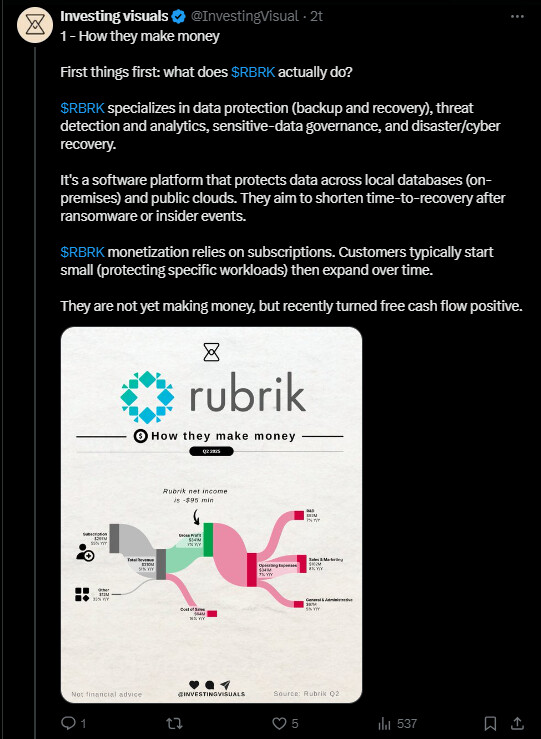

@Hessuli I’m replying to this because it might be useful to others as well.

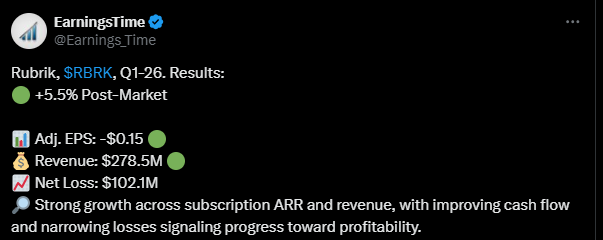

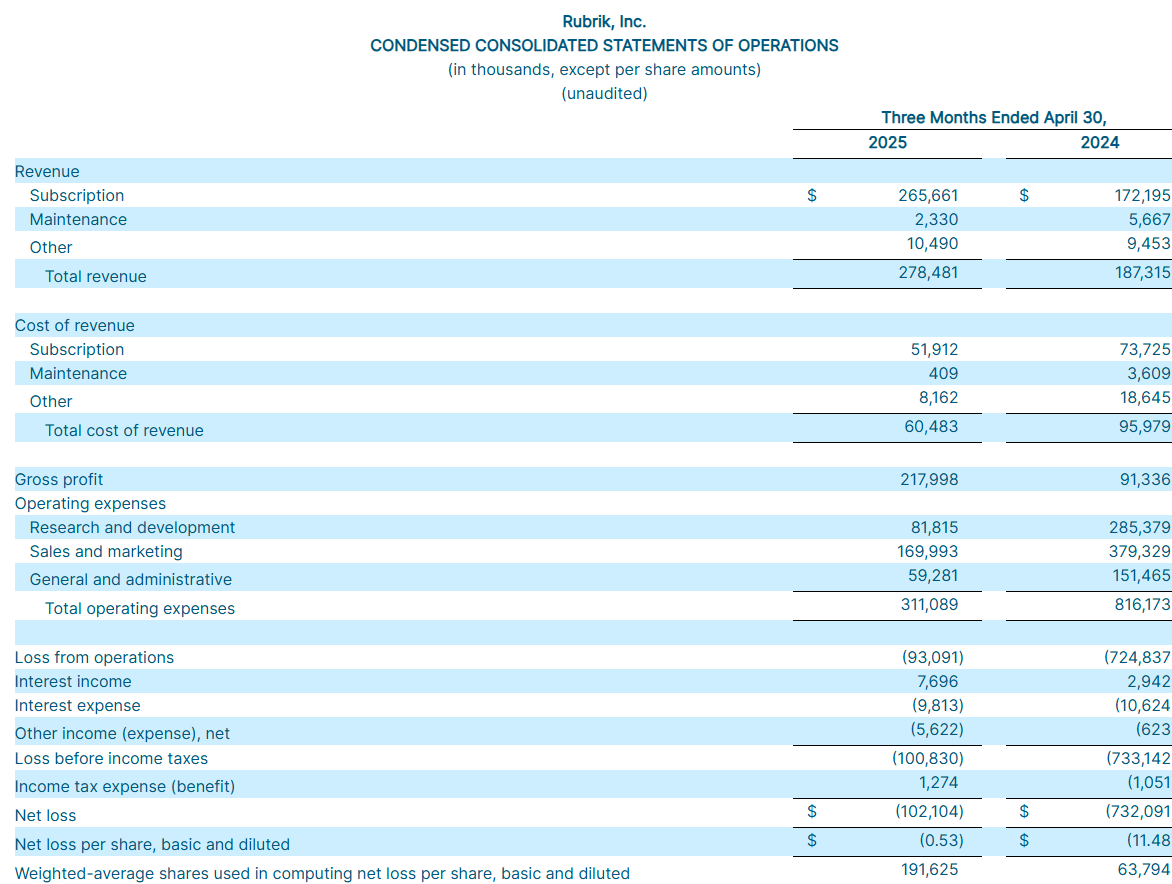

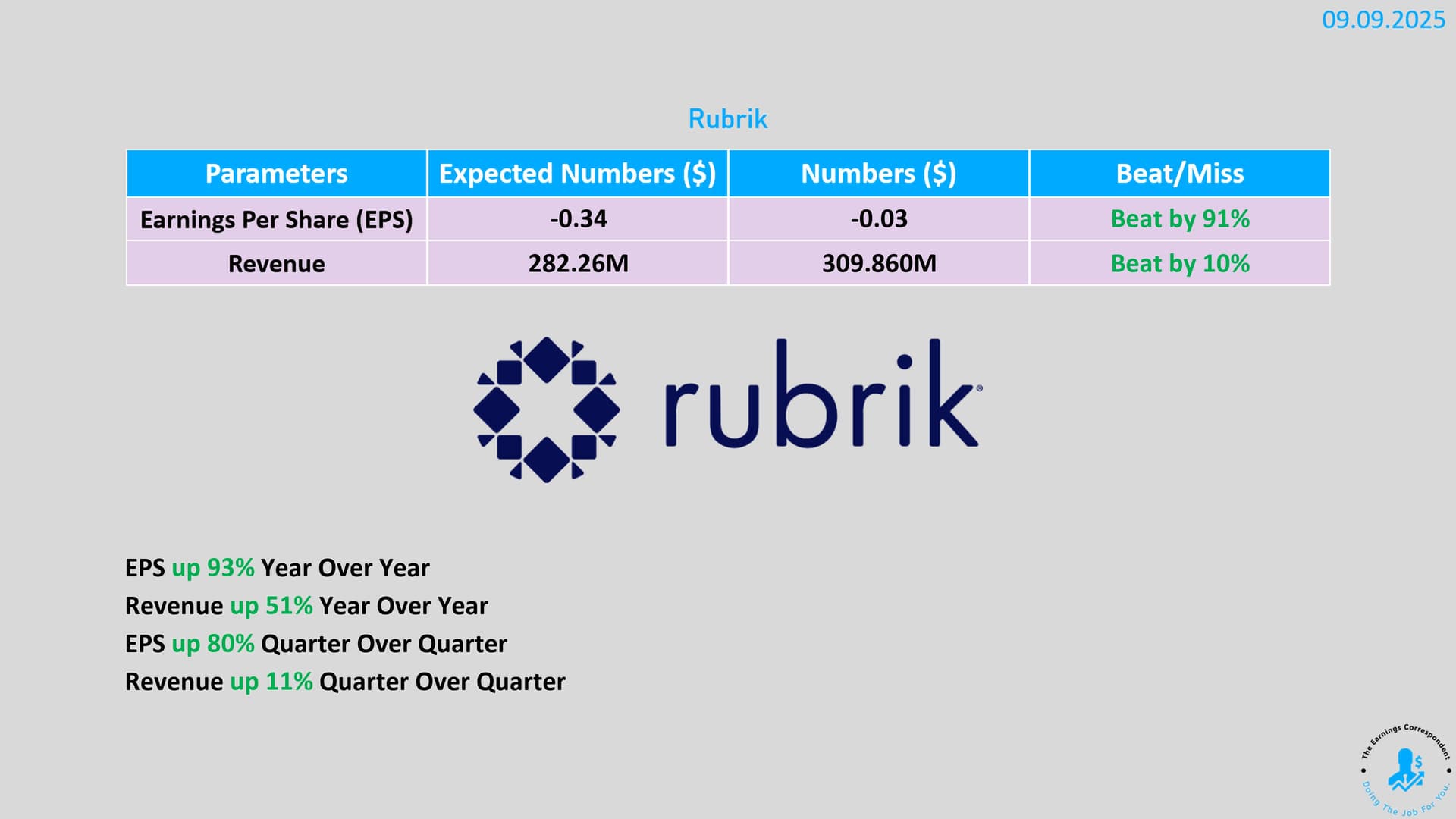

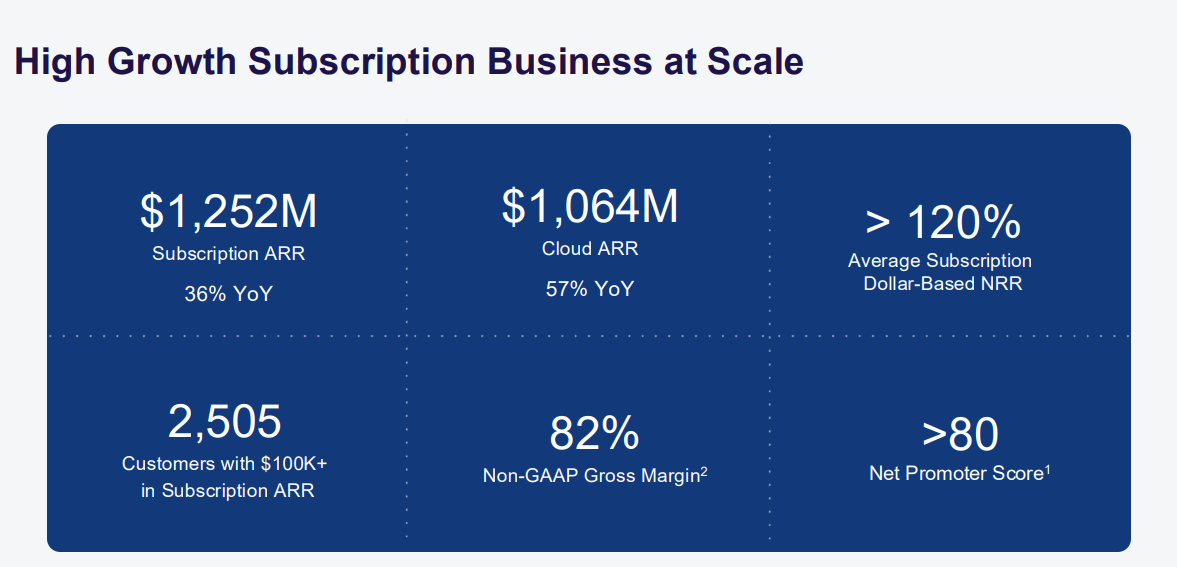

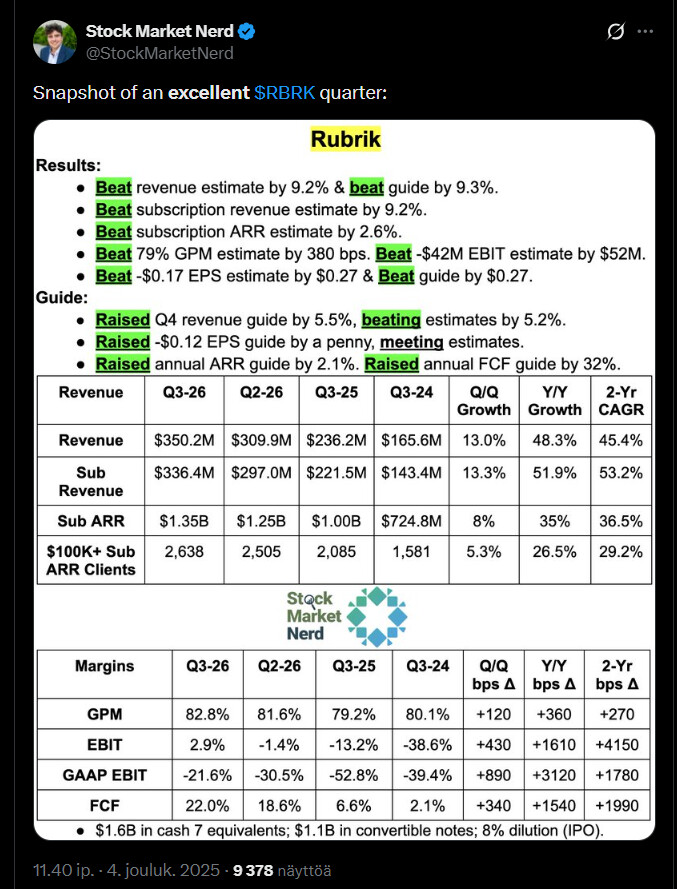

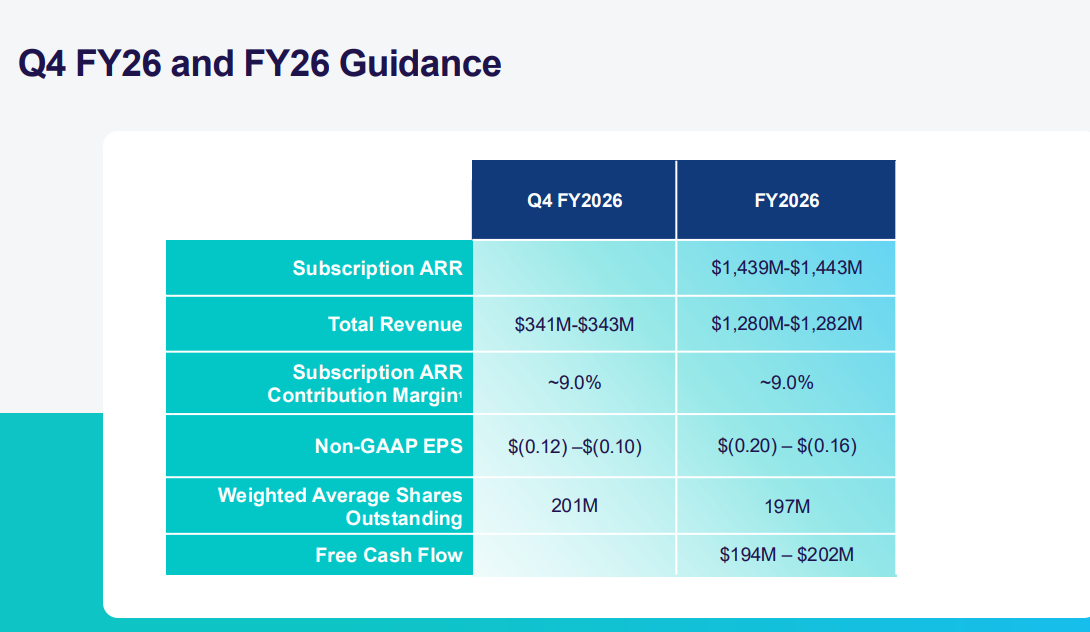

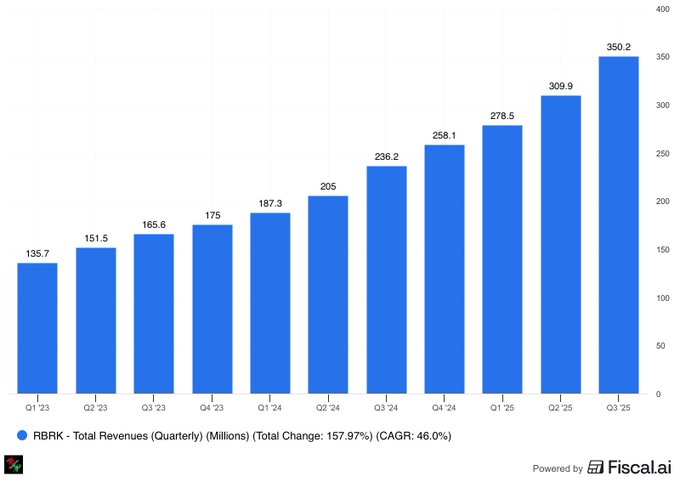

Rubrik made a strong earnings break, so this is a good time to use RBRK stock as an example of how I quickly analyze a chart/stock that has only been on the market for a short time (since 2024), made a break, and left a big gap behind. The valuation, including comparisons to peers, had already been discussed earlier, so here I’m outlining a point where I’m ready to add to a stock I consider potential (depending, of course, on the general market situation, overall trend, and market-accepted valuation multiples).

As a result of Friday’s rise, a clear gap remained between $71.97-$84.33, and that immediately tells a couple of things:

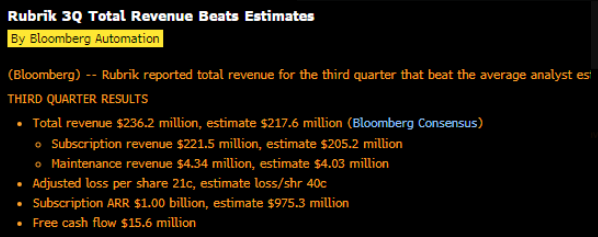

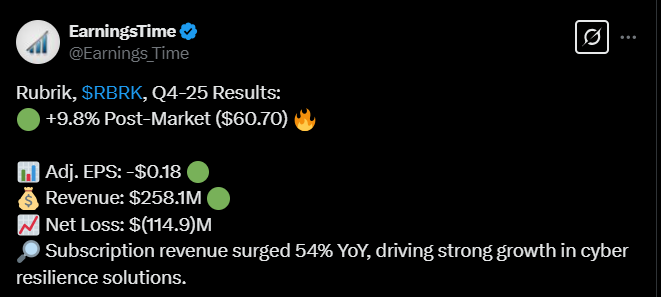

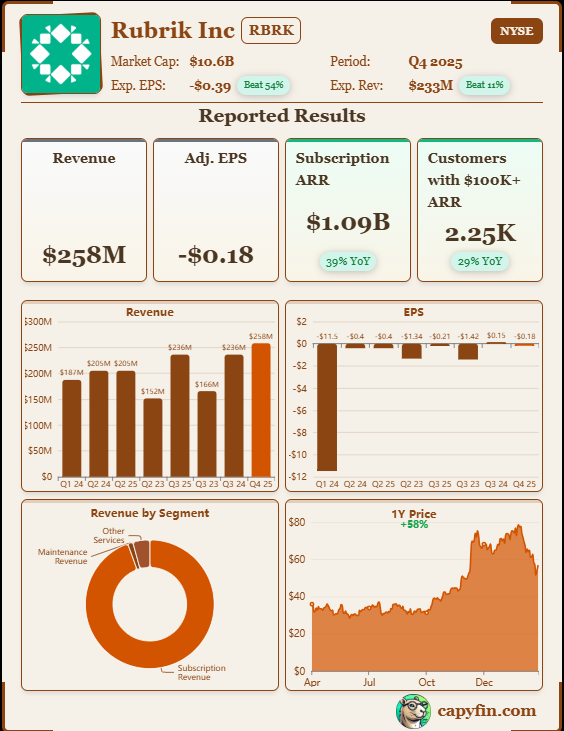

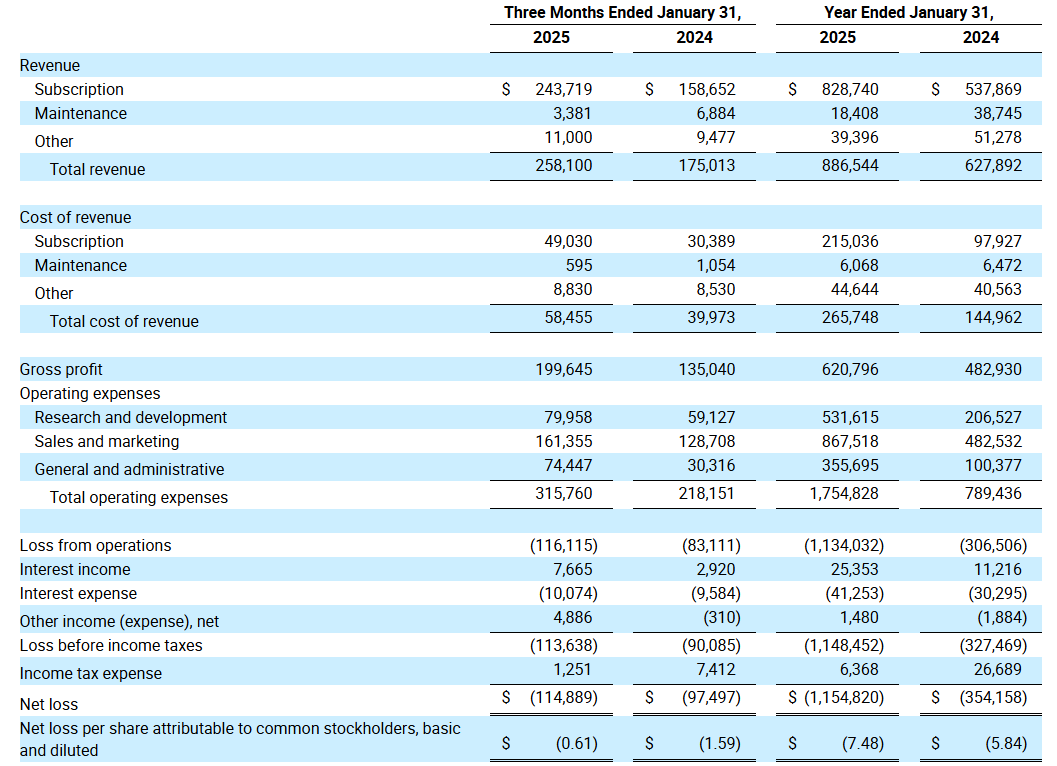

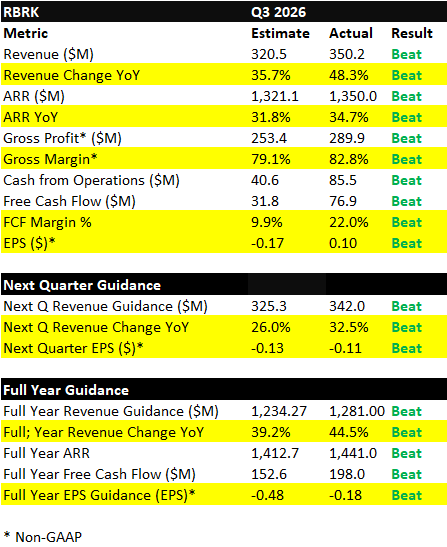

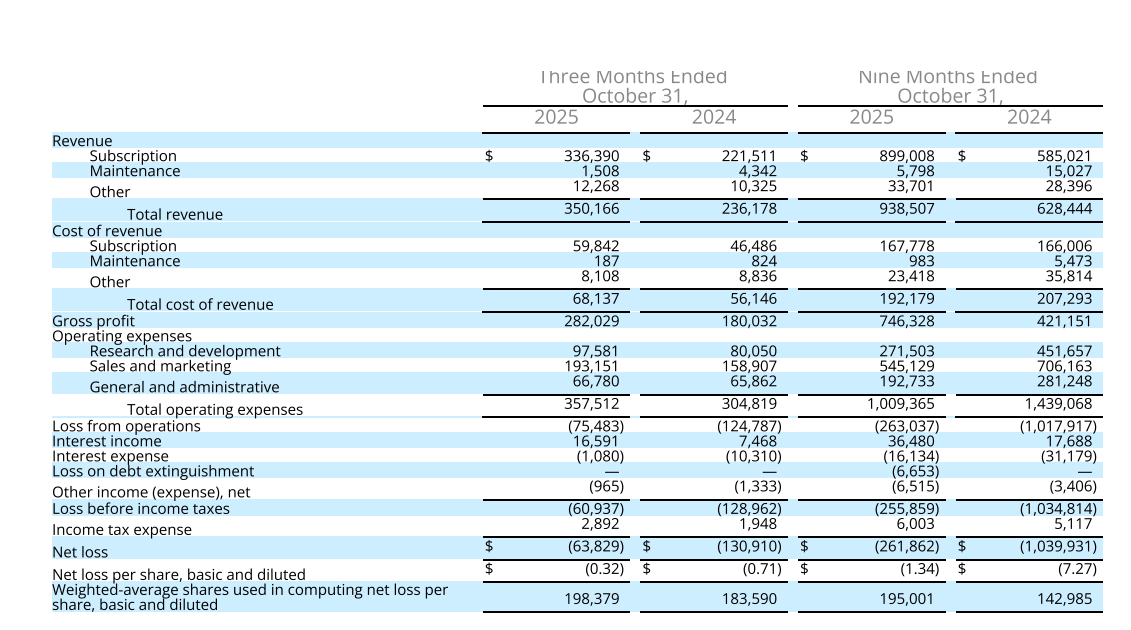

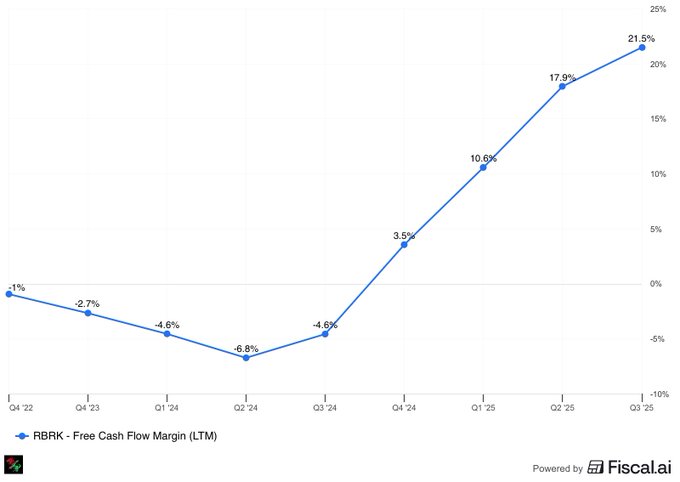

The results were acceptable to buyers, and shorts, which accounted for approximately 9% of the outstanding shares last week, got stuck below the gap. These shorts and their closing cause some of the rise and buying pressure, although the results were also acceptable to investors, like myself, because non-GAAP EPS has now turned positive, and that looks good to many eyes for the future.

If buying enthusiasm wanes and we approach an open gap or trade within it, I always monitor, especially in strong stocks, how the price behaves at the midpoint of the open gap. In RBKR’s case, at the midpoint of the gap (i.e., approximately $78.13), there is also the MA200 moving average, which, being rising, is strong support. Together, these often reinforce each other. The MA50 is also now turning upwards and will likely cross above the MA200 in the coming weeks (meaning they will soon be “the right way up” and both rising). MAs and EMAs with their various variations are followed by even larger players, in stocks and indices from Charlie Munger to Stanley Druckenmiller, so the benefits derived from them should not be underestimated, and they often indicate the strength of a trend at a quick glance.

Generally, gaps are filled with a very high probability over time (estimated 95-97%), so staying above the midpoint almost invariably indicates clear strength (at least temporarily), especially if there’s a strong bounce and a long wick or “tail” on that candle.

Another point I follow on the chart is the Low Volume Nodes (LVN) of the volume profile on the right side, which are often very good reversal points. These points therefore have the least trading volume, and in my experience, they work very well or at least provide information about price action. In RBKR’s case, the LVN is quite precisely $81, so the result for me is that the $78-$81 area forms a very clear support zone and a place for additions if it is not breached. Above that area, I consider the stock very strong, and only if that level area is broken below do I expect the gap to be filled and the next support area around $72. High Volume Nodes (the highest points of the volume profile on the right) are points where consolidation might occur for long periods, and a suitable trading price is fought over. Right now, we are in the June-September range, whose HVN is approximately $87.70. As a rule of thumb, the more commonly used clear support/resistance/indicators coincide at the same point, the better they work.

Technical analysis, combined with fundamental analysis, offers a great deal of information about one of the most important aspects of stock markets, namely buying and selling behavior, i.e., price (Price!), and with very simple TA, one can significantly improve entry and exit points and gain quick insights into pricing.

As a side note, a similar tail hitting the midpoint of a gap was seen, for example, in Nebius (approx. $78.25) during the worst of the decline on Fri 21.11., from which it bounced back relatively quickly to around $100. I was closely monitoring that point, so it was easy to buy the stock when that point was not breached, or the candle did not close below the midpoint. Not filling the gap (at that moment) immediately indicated that the buyers were institutions and the stock was stronger than it appeared during the decline. I wrote about this in more detail in the Nebius thread already at the beginning of October (2.10.). With just these simple tools, one can gain a lot of additional information to support stock purchases, and often the simplest things work best and provide just the right amount of extra confirmation. Hope this was helpful.