Yep, and companies rarely advertise this voluntarily ![]() Usually, they vie to boast about how only that good organic development has driven ROIC or ROCE to even higher levels

Usually, they vie to boast about how only that good organic development has driven ROIC or ROCE to even higher levels ![]() Only one company comes to mind that openly talks about this. It’s the serial acquirer Judges Scientific, which reports a ROTIC figure, or return on total invested capital

Only one company comes to mind that openly talks about this. It’s the serial acquirer Judges Scientific, which reports a ROTIC figure, or return on total invested capital ![]() The company adds these amortizations back so that the invested capital better reflects what was actually paid for the companies. From the company’s annual report:

The company adds these amortizations back so that the invested capital better reflects what was actually paid for the companies. From the company’s annual report:

11 Likes

Thanks, that ROTIC is very excellent and interesting. I’ve been thinking about something similar, but of course, someone has already launched an official term for it. ![]()

In the case of Constellation, I’ve seen massive calculation exercises in blogs, where they’ve tried to figure out the “real” return on invested capital, for example by looking at the total cumulative cash flow spent on investments as a proxy for invested capital. You can ponder these endlessly, and it’s a useful way to spend time.

Going even deeper, the development of a company’s value is driven by RONIC: Return on new invested capital, i.e., the return on newly invested capital. ![]()

RONIC indicates how the new investments made by the company perform. A company’s growth in itself only creates value if the return on reinvested capital is higher than the required rate of return. If the company is unable to do this in the long run, in other words, if the company does not have attractive investment opportunities, it should return capital to shareholders or pay down potential debts.

RONIC is calculated as the ratio of the change in operating profit NOPATT+1 - NOPATT+0 to the change in invested capital ICT+1 - ICT+0. In practice, this gives the investor an answer to how much new capital the company has had to invest in its business to achieve operating profit growth.

If we again assume that, on average, a serial acquirer pays 8x EV/EBITA for companies (Röko has paid less than that on average, note), taxes are paid on the profit (~20%) which roughly converts that to EV/NOPAT 10x; organic growth is 2% but “free” (because the return on capital for the businesses is something like 150-200%), then RONIC is 12%.

12% safely exceeds the required rate of return on capital, which hovers in the 8-10% range. Let’s say ten; it’s a nice number to round to.

Again, key points include:

-Quality of growth: unsuccessful acquisitions penalize RONIC

-Operations of acquired companies: if they falter, there is less cash flow to invest and growth slows down

-Capital lightness of acquired companies. Again, growth slows down if a larger portion of the cash flow goes into maintenance investments

-Discipline of growth: prices higher than EV/EBITA 8x are not paid for targets except in exceptional cases (a very fast and reliably growing target).

10 Likes

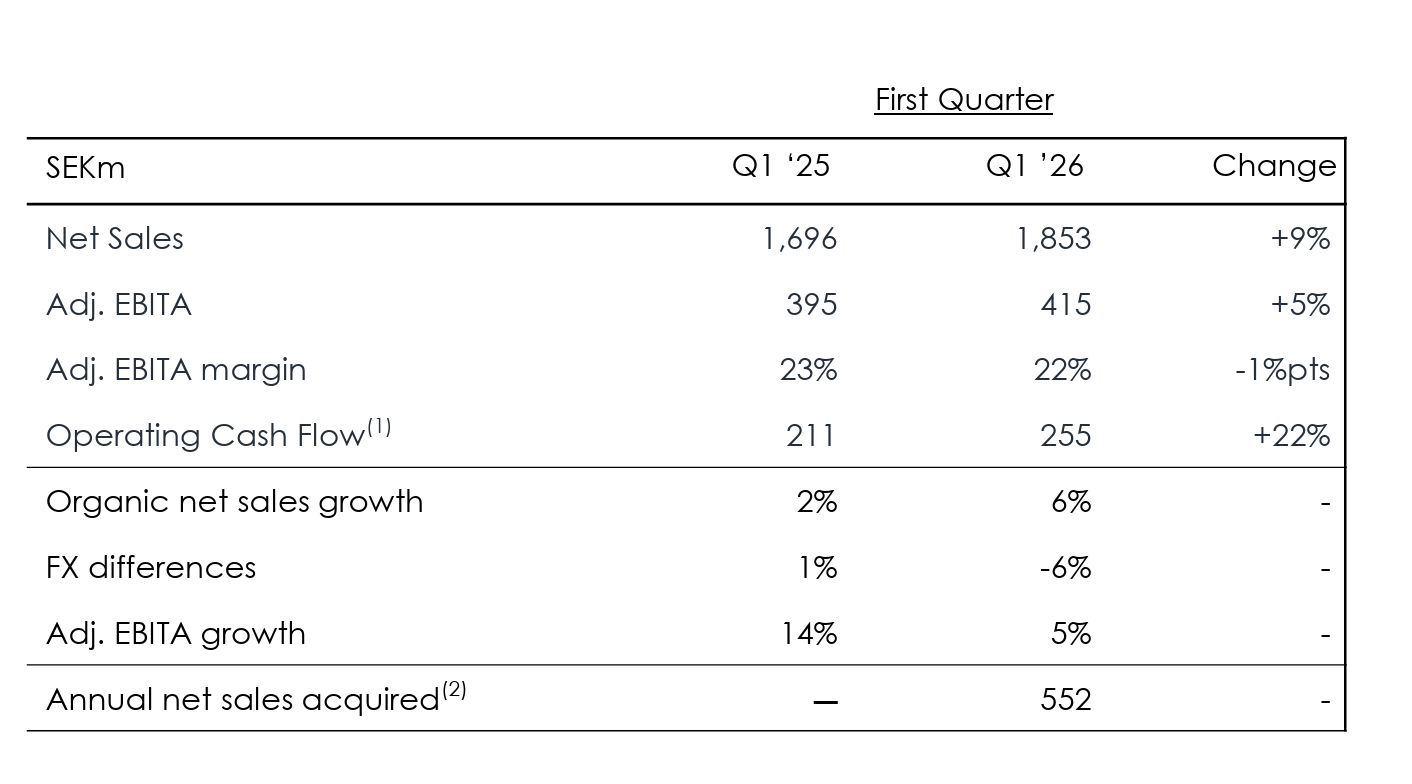

Röko’s Q1 numbers are out.

Stockholm, April 21, 2026

- Adj. EBITA increased 5% to MSEK 415 (395) in the quarter driven by acquisitions and organic growth, but with negative exchange rate differences

- Adj. EBITA margin declined to 22% (23%) with recent acquisitions having a negative margin impact in the first quarter

- Net debt / LTM Adj. EBITDA increased to 2.4x (1.9x) at the end of the quarter, driven by recent acquisitions consolidated towards the end of the quarter

- Three acquisitions with combined annual sales of MSEK 552 were completed in the quarter

Currency headwinds, these will fluctuate back and forth in the long run.

16 Likes

An extremely boring-looking earnings report. Rökö has been making waves among my investment circles, but it still hasn’t clicked what attracts people to own this extremely mediocre company? I mean, something other than the obvious Verneri phenomenon.

Whenever you ask about this, intensive ROIC-coping begins, where they try to prove the investment is secretly damn good with some complex variation of return on invested capital calculation, as long as you feed the numbers into Excel in just the right way ![]()

21 Likes

I took a look at the transcript of the audiocast, which now appears immediately on Inderes’ service since Röko is our audiocast client. This time, my colleague Sabina acted as the moderator. ![]()

Organic growth was indeed very strong, even though it’s hard for Johan to comment on exactly what all 33 companies have been doing. But apparently, Röko teaches the heads of the companies to implement continuous price increases.

I think in general, it’s a bit difficult to comment too much on volume versus price across the group because there’s the diversification among the subsidiaries. But we can mention that we believe that the work we have done through the last couple of years of continuing to educate our local management teams on the importance of continuous price increases means that some of them at least have benefited and captured the opportunity that exists in the current market by raising prices.

The impact of tariffs is still visible, and the US share of revenue (exports) dropped to 5% from last year’s 7% level. Apparently, the M&A market has picked up and there are plenty of good targets for sale. Röko has little debt and abundant cash flow. ROCE is dipping because the results of the acquired companies don’t show up in the accounting records yet, but the balance sheets roll in immediately.

The whole set is 12 minutes long. ![]()

17 Likes

Is that a little or a lot of debt if net debt/bullshit earnings is 2.4x? ![]()

On a more serious note: Did management explain in the webcast which industries/companies are driving the strongest organic growth?

6 Likes

EBITA is maybe batshit or something compared to EBITDA, because EBITA reflects cash flow before taxes well. ![]()

Most of the debt is that put/call arrangement, which is on paper. “Real” debt is less than a billion kronor.

(Note: that put debt still needs to be taken into account, because if you only look at market cap and earnings, you get a too generous picture of the company’s valuation since 100% of the subsidiaries’ results are included in the earnings! In reality, there are always minorities who are entitled to a portion of the results.)

No, as I quoted above. But Röko buys companies with pricing power (based on their high margins and capital-lightness) and clearly the company also instills a Swedish culture of bold pricing in them.

11 Likes

The best part of the Inderes forum is when Eka comes to challenge your investment thesis in the thread of a company you own, thanks! ![]() I can’t say why others own it, but I can tell you why I do. It’s impossible to summarize this in a single post, but let’s start with the basics:

I can’t say why others own it, but I can tell you why I do. It’s impossible to summarize this in a single post, but let’s start with the basics:

The starting point of the investment thesis is that there are just over 20 million small and medium-sized enterprises (SMEs) in Europe. A significant portion of these companies are privately owned by entrepreneurs and families, meaning they aren’t part of any mega-corporation yet. A large number of these companies were founded by older generations, so many will face retirement in the coming years and decades. For almost all of these companies, a successor cannot be found among heirs or family, for numerous different reasons. Because of this, approx. 15,000 SMEs are sold in Europe annually.

Röko is a “forever owner” of such SMEs. It buys them and, in principle, owns them forever and reinvests the money to buy more. This creates that compounding machine in Excel. The company basically has endless opportunities to reinvest cash flows in the coming decades. It’s obviously easy to grow through acquisitions, and anyone can buy whatever companies to grow if they have endless money.

This brings us to ROIC. I think this part is extremely simple; you don’t even need Excel, mental math is enough ![]() Röko’s business is ultimately capital allocation, effectively stock picking in private firms. If you pay fair value (required return is high because it’s private and small) for a good SME that is:

Röko’s business is ultimately capital allocation, effectively stock picking in private firms. If you pay fair value (required return is high because it’s private and small) for a good SME that is:

- Historically very profitable

- Reasonably defensive

- Possesses pricing power

- Needs very little maintenance investment (capex)

…then such companies constantly produce good cash flow that can be reinvested. These companies wouldn’t be remarkable investments on their own, but with masterful reinvestment of cash flows, magic starts to happen if you can do it for decades. In many investment cases, the problem is exactly that reinvesting cash flows is impossible to predict, or the company simply has nothing to invest in with a good return. In serial acquirers and investment companies, this reinvestment problem is inherently solved.

Röko targets approx. 15% growth, the prerequisites of which have been calculated several times in the thread. My thesis is that Röko can maintain this pace for a truly long time—a decade or two.

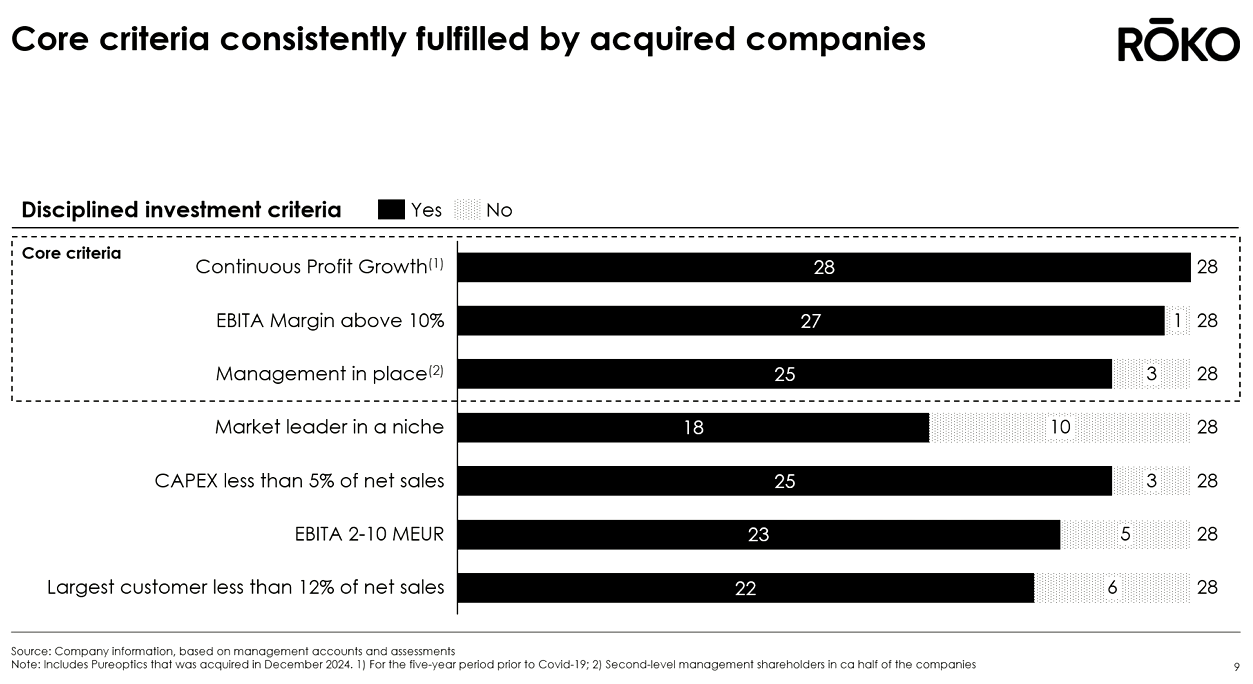

Röko’s acquisition criteria:

Maybe it can be summarized as: if successful, Röko will become a kind of mini-Berkshire, but with European SMEs and without the insurance float ![]() So, it’s pretty useless to expect +20% turbocharged annual returns, but purely by reinvesting cash flows, there are reasonable chances for, say, 15% annual returns on paper.

So, it’s pretty useless to expect +20% turbocharged annual returns, but purely by reinvesting cash flows, there are reasonable chances for, say, 15% annual returns on paper.

That’s still a multi-bagger over decades. So this is an investment that requires time and patience ![]()

A topic for a completely different post is what all this described above requires from both the capital-allocating headquarters and the cash-flow-generating subsidiaries. In practice, Röko is a lean 8-person headquarters and a group of dozens of entrepreneurs with their employees in very diverse industries. Running such an entity efficiently and with the right incentives is no easy feat.

Also fishing in the same waters are a whole bunch of other serial acquirers, PE clowns (private equity), and industrial/strategic buyers. Röko’s angle here is the forever ownership and decentralized operating model, where acquired companies are run entrepreneurially even after the transaction, with minority ownership keeping incentives in check ![]() Overall, very similar logic for value creation as Berkshire’s unlisted investments, just without the insurance companies. This, of course, requires masters at allocating capital, which I believe Röko has.

Overall, very similar logic for value creation as Berkshire’s unlisted investments, just without the insurance companies. This, of course, requires masters at allocating capital, which I believe Röko has.

I’ll add that in an investment case like this, there are no rocket-ship drivers; instead, this is damn boring basic work, entrepreneurship, and capital allocation ![]() Things happen slowly, one acquisition at a time, and you have to look at the case with a very long-term view. This is like watching a tree grow in the yard. Nothing really happens in a year, but in a decade or two, a lot. There are no exciting pharmaceutical companies here waiting for a breakthrough to ten-bag in a moment

Things happen slowly, one acquisition at a time, and you have to look at the case with a very long-term view. This is like watching a tree grow in the yard. Nothing really happens in a year, but in a decade or two, a lot. There are no exciting pharmaceutical companies here waiting for a breakthrough to ten-bag in a moment ![]()

22 Likes

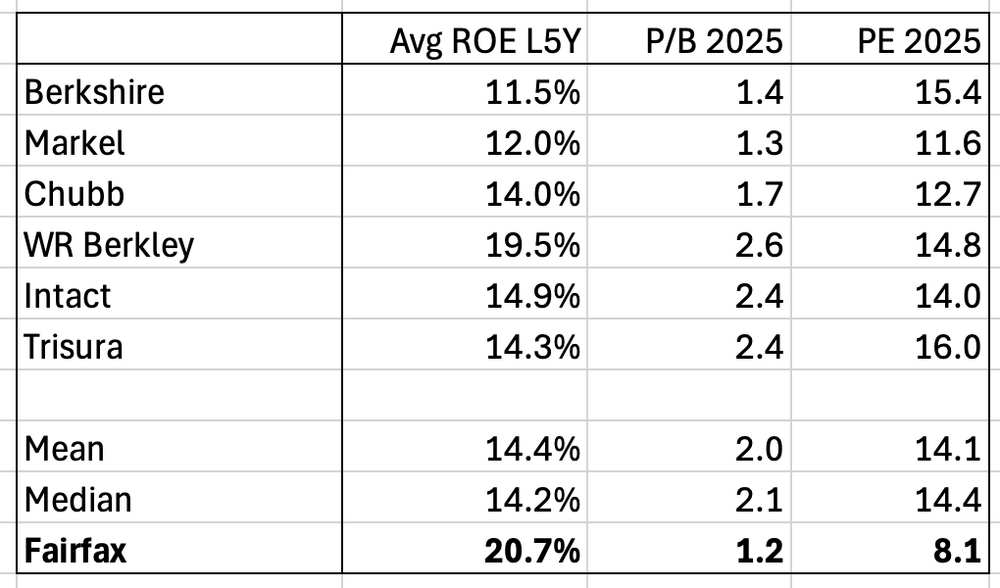

Speaking of mini-Berkshires. Fairfax is trading below P/E 10, its market cap is in the same ballpark as Berkshire was in the early 90s (adjusting for inflation), it is aggressively buying back its own shares, and has delivered over 20% ROE for the last 5 years. Röko is already priced close to its full potential, while Fairfax has plenty of room for multiple expansion. So, a bit of a “buff” at this point. ![]() Some Röko investors might be interested if Berkshire-like companies are close to your heart.

Some Röko investors might be interested if Berkshire-like companies are close to your heart.

16 Likes

The financial markets have long recognized the potential of unlisted companies, and investors focused on these assets are called private equity investors. There’s an unimaginable number of these debt-leveraging, value or quality investing PE funds just in the European markets. In Europe, private equity investors also have a genetic peculiarity of being quite security-oriented, so Röko’s market is a true (blood)red ocean where you have to work tirelessly to achieve even mediocre returns.

Normally, in private equity, a fund’s life cycle is a maximum of ten years, which is enough time to improve the management model and business quality of acquired companies and maximize the buyer’s impact and thus return, also aligning well with the investment horizon of an investor investing in these assets.

At Röko, the goal is to own forever, which admittedly can be beneficial if you identify as a pension fund and your investment horizon is also eternal. Is it? I argue that a typical Röko investor does not benefit from such an ownership philosophy in any way, and I’ll add that few investors even have personal experience of what, for example, a significantly shorter 10-year stock ownership means and what kind of drastic ups and downs can occur during such a period for a single holding.

Investors usually get into funds and stocks as ‘long-term owners’ until those two or three bad years in a row come along (when one should, of course, increase ownership), after which trust in management is lost, and money is pulled out. This is how investors have always acted and always will act. Unlike in PE funds, Röko’s continuous stock liquidity is a huge minus because it unfortunately enables poor timing and thus the destruction of one’s own investment returns.

Liquidity also brings other problems for the investor. While in a conventional PE fund, only the acquirers need to be scrutinized carefully, Röko has taken a leap in difficulty because that alone is not enough. Mr. Market also steps into the boxing ring, who relatively efficiently assesses the correct stock price based on the team’s past performance and the companies’ future prospects. Furthermore, the more attractive the business model and story Röko has, the more you have to pay for them in the stock price. Of course, with decades of ownership, the impact of the purchase price is effectively neutralized, but that does not save ‘fair-weather Buffets’ investing in the shorter term.

So, in my opinion, those investing in this should just switch directly to a private equity fund if they want similar exposure to that market and asset class, thus avoiding those pitfalls and freeing up time spent monitoring stocks for other projects. The fee structure in those is often perceived as salty, but Röko’s founder also has a history of compensation disputes, and therefore, they will certainly ensure in the same way that too much benefit from the created added value does not flow into the wrong pockets of small investors.

I see the greatest benefit of Röko and other similar companies in the sector for jaded stock pickers who no longer have the energy to spend hours sifting through stocks and making difficult choices and therefore want to outsource that company digging to another person and become passive to enjoy the appreciation of a long-term, thoughtful owner with a well-diversified portfolio. In their own mind, they can then convince themselves that the person staring back from the mirror in the morning is a ‘stock picker’ and not a ‘fund investor’.

Now that I have written about Röko in this tone, the reader has probably formed an incorrect impression that I consider this a bad investment. Indeed, Röko easily beats a typical Finnish investor’s dividend-muddler investment due to its serial aggregator logic and target market, but at the same time, as an investment idea, it is irritatingly aggressively mediocre.

21 Likes

I think Röko (or other “perpetual” owners) has certain advantages at the negotiating table with SMEs. While PE guys in their puffer vests or suits would be coming to the family business office after the transaction to straighten out EBITDAs and give advice, Röko instead gives entrepreneurs full autonomy to work.

With this approach, Röko specifically looks for SMEs where the entrepreneur-owner and/or other key personnel would stay on to run the business with an entrepreneurial spirit (as minority owners). This approach can be very attractive to a seller in certain deal situations, but not all.

For example, if a family business had a successor in the next generation or among key personnel, but they didn’t have the personal risk tolerance to buy 100% at once, Röko could be an attractive option. In this case, the next generation/key personnel can stay and run the company as minority owners with entrepreneurial freedom, while Röko carries the risks of the majority owner. The seller can trust that the company will preserve its brand, culture, and employees in the eternal home provided by Röko. Meanwhile, in PE, an aggressive five-year plan would be hammered out to cover those outrageous costs and generate returns on top.

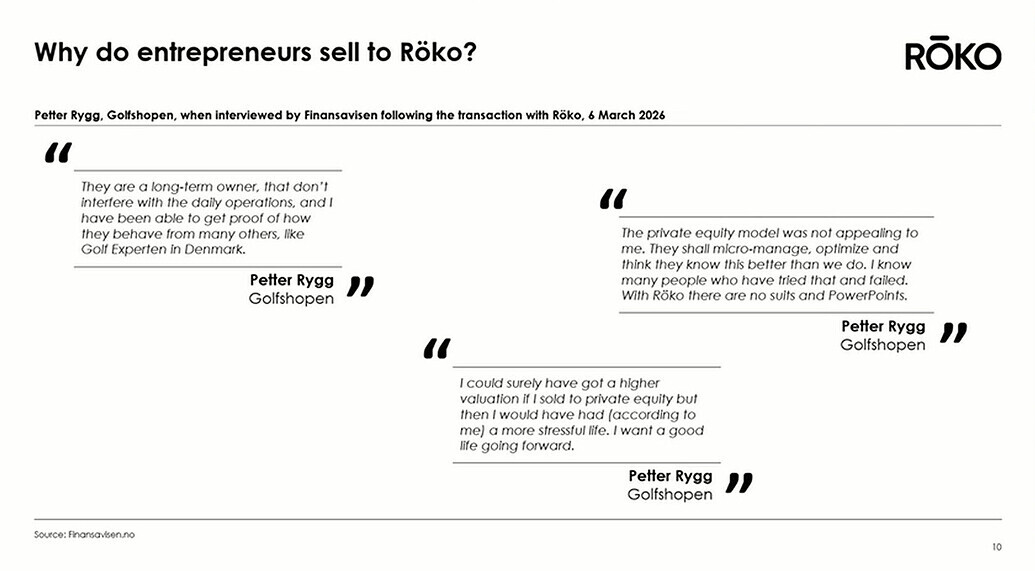

This is a bit of “soft” stuff, but for some SMEs and entrepreneurs, these can be very personal and important matters. An entrepreneur may know all their employees very well—they might even be family members or relatives—and would primarily want to preserve their jobs under a new owner. Röko can also be an option for an entrepreneur to diversify their ownership well before retirement age to provide security for their family. They sell the majority to Röko and then run the business as a minority owner, just like before. There were some fun highlights on this slide, where an entrepreneur who recently sold their company to Röko was interviewed in a magazine:

I agree regarding the position of a Röko investor. It requires guts and a truly long-term investment strategy, for which every investor is, of course, responsible to themselves. For a completely rational Röko investor, continuous liquidity is just an opportunity to buy more as the expected return improves, even if the sellers are those small-cap funds with their paper-handed owners. As you said, Mr. Market has factored in the value creation potential of such a business quite efficiently, so the opportunities brought by volatility and a long holding period must be utilized to achieve good returns.

In my opinion, Röko’s remuneration and incentives are generally in a completely different ballpark considering the position of a retail investor compared to PE. In practice, the Röko team only has fixed salaries, and everyone has significant share ownership.

You still have to do a bit of stock picking among serial acquirers, as there are plenty of them listed nowadays, often with a very similar-looking narrative ![]() That mediocrity and seediness, at least in terms of returns, might be left behind over time

That mediocrity and seediness, at least in terms of returns, might be left behind over time ![]() But yeah, you won’t get the next fast multi-bagger out of this no matter how hard you try, unless Mr. Market goes crazy again—so this is boring!

But yeah, you won’t get the next fast multi-bagger out of this no matter how hard you try, unless Mr. Market goes crazy again—so this is boring!

13 Likes

The most important thing is that in the morning, a ‘money man’ stares back from the mirror, not a broke ‘stock picker’. The operating logic of private equity funds differs significantly from ‘decentralized serial acquirers’ where decision-making largely remains with the operating companies; also, the fee structure is typically much more favorable for serial acquirers. The incentives of the main owners, at least in Röko’s case, are largely aligned with those of the retail investor.

Serial acquirers have most often outperformed the returns of private equity funds. The main reasons are likely:

-

Lower costs

-

No need to sell; good targets churn out excellent cash flow for longer

-

Serial acquirers usually buy smaller, private companies at significantly lower multiples than those for which large PE funds compete.

15 Likes

This is certainly true. I have observed from my inner circle how a larger firm can destroy the corporate culture of a smaller acquired company in just a few years, along with the entrepreneur’s “life’s work.” Since it is difficult to view one’s own company with cold rationality, it definitely influences the decision of who to sell to.

Quite a few messages have now mentioned that Röko’s holdings generate cash flow for the company. This is exactly the same kind of money that all other profitable listed companies produce, which can then be used for business growth, acquisitions, strengthening the balance sheet, or profit distribution. No “Rheingold” (Reininkulta) has been found in the quality trash bin of small caps ![]() . If future cash flows have been priced even somewhat correctly at the time of sale, then one receives perfectly fair compensation for those holdings, so it doesn’t essentially matter whether the companies are owned or sold.

. If future cash flows have been priced even somewhat correctly at the time of sale, then one receives perfectly fair compensation for those holdings, so it doesn’t essentially matter whether the companies are owned or sold.

I can believe that there were massive inefficiencies in the market in the era before the modern internet, when serial acquirers entered the Nordic markets with a new way of operating. I know of cases where owners of small companies were completely at sea when selling their companies, having to ask their accountants and entrepreneur friends about pricing because the expertise and information weren’t available, only to be “cleaned out” by professionals. After all, it wasn’t that long ago when companies were bought and sold based on substance value and book value.

Today, the markets are significantly more efficient; when a small entrepreneur can learn about the correct pricing of unlisted companies by having a 15-minute sparring session with ChatGPT, those same low-hanging fruits are no longer available to buyers. Overall, the idea that these serial acquirers could generate higher returns in the future with less leverage, without an increasingly efficient market correctly pricing the stock, is a bit naive. Past performance is no guarantee of future returns, and every player rushes into the corner where attractive opportunities arise until those outsized returns have been competed away.

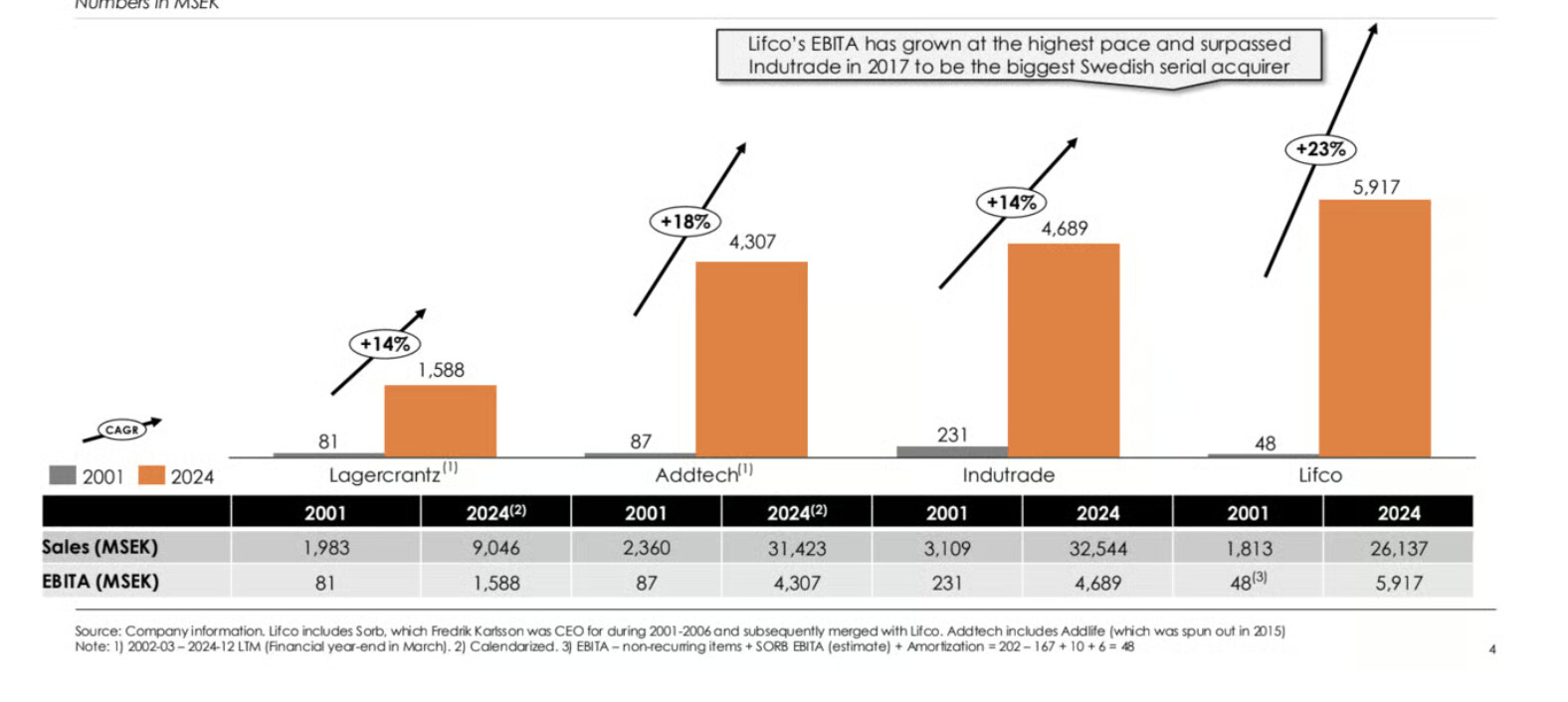

The image you posted shows impressive 23-year CAGR development curves, but no investor is actually capable of finding winning serial acquirers and then independently owning a listed stock for such a period. It’s simply not possible. My own record in my investment career is over ten years, and that period included all sorts of bull and bear markets, good and bad interim reports, the birth of new Finnish investment media and the death of old ones, new investment tools, the excess returns made by the neighbor in another sector, changing investment trends, the rise and fall of various investment influencers, drastic changes in life situations, as well as the irrational allure of every new stock and the typical boredom with current holdings. It only takes exactly one moment of weakness during this period where you feel more like hitting the sell button than not, and the holding disappears from your book-entry account.

Extremely long-term ownership strategies for liquid listed stocks are many orders of magnitude less credible than New Year’s resolutions to hit the gym and walk past the chip aisle without buying anything. You should definitely not plan your investment strategy around it, because it is doomed to fail; genuine “forever-holders” of winning stocks are that rare.

If you are truly a superhuman or some kind of elderly person with dementia and therefore capable of owning serial acquirers for extremely long periods without selling, then you can probably reach the level of historical index returns and maybe a few single-digit percentage points above that. But for us mortals, it is psychologically much easier to invest in practically the same market through some illiquid PE fund, where you aren’t offered a constant opportunity to sell your holdings too early or at the wrong time. No matter how much you repeat to yourself that time in the market beats timing the market, everyone’s hands eventually start to itch for some kind of action after years of holding.

4 Likes

An awfully long text where I’m finding it hard to grasp the main point. The word ‘cash flow’ wasn’t acceptable and long-term holding is impossible?

If we assume that when selling you always get fair value, no more and no less, doesn’t that exactly support the business model of serial acquirers? The money would have to be reinvested anyway, so it’s simpler and more efficient to just allocate new cash flow effectively. Sure, in theory, the bad apples should probably be sold, but according to that theory, they have the same problem: you would only get fair value for them and selling wouldn’t be of any benefit. So, the simplest thing is to allocate cash flow productively.

I’m not exactly an advocate for forever-holding myself, even though I do have a few 10-year+ multibaggers. That wasn’t what those charts were about; it was about the fact that significantly more genuine shareholder value has been created than in some of those slick-haired guys’ PE funds. I believe serial acquirers will continue to generate better average returns than PE funds, and I don’t see anything naive about that; in fact, I think it’s naive to think that PE funds with their fee structures could beat serial acquirers, especially when massive amounts of institutional money are being shoveled into them nowadays.

It is certainly true that the market is more competitive and efficient than ever before, which applies to pretty much all investment activities.

9 Likes

You are tilting at windmills here several times over. Even when holding an index fund, you have to hang onto it even through heavy volatility. PE funds don’t have 0.07% fees; you have already found a cheap fund if they are closer to 1%. You know how much that difference does to returns over the years. It is very difficult to define which tactic works best for which investor and in which stock.

2 Likes

Some of Eka’s arguments are better suited for an index investor than a stock picker, but then that argument related to holding is in conflict with index investing… Maybe the intention is just to troll.

1 Like

Personally, I find those long-term charts to be distractors in the discussion because an investor’s return differs significantly from the stock’s return unless the investment horizon and the holding period are identical. For example, Talvivaara’s lifetime stock return was -100%, but many who invested in Talvivaara saw returns that were even strongly positive, depending entirely on when they bought and sold. So, while that paper wealth looks sweet in these charts, practically no investor actually achieved that theoretical return because such holding periods are completely unrealistic.

In my opinion, one can argue for long-term ownership based on differences between the investor’s and the market’s cash flow estimates and preferences arising from the investment horizon. However, for a shorter ownership spanning only a few years, I don’t really see the point, as there are no tools here for an investor to differentiate themselves from the market. The management’s track record is public, corporate ownership is fragmented and neither it nor future acquisition targets can be rationally analyzed, and future cash flows are frustratingly stable. Thus, the stock is likely priced correctly to its full potential, and the shorter-term investor is doomed to mediocre returns.

Perhaps this does sound like trolling, but I think we are just on different wavelengths. To me, the premium paid for illiquid investment products is completely rational when looking at the real world instead of homo economicus. The typical investor loses return with every investment decision, whether it’s a buy or a sell. The optimal situation would be for someone else to assemble a suitable personal permanent portfolio allocation that the investor could not influence themselves—somewhat similar to how our pension fund system works.

However, this isn’t psychologically possible in personal investing, so an investor must either try to minimize the return losses caused by investment decisions through experience and study—which may eventually even turn their own decisions toward a positive expected value—or minimize the opportunities to make investment decisions by acquiring illiquid assets, such as an oversized owner-occupied home or those illiquid PE funds. Naturally, since illiquidity improves the average investor’s expected return, it is worth paying premiums for.

Now, if you look at the situation from your own perspective, the conclusion is the opposite. You are certainly an experienced and skilled investor and your investment decisions add value, so you must ensure that you are able to make them. Therefore, liquidity has value to you, as does finding yourself in situations where estimating a stock’s cash flows is uncertain or difficult, because in those situations, you are able to maximize the value generated by your investment decisions.

At the risk of @Verneri_Pulkkinen revoking my posting rights, I will state that I find this entire serial acquirer sector to be a bit of a silly target for a stock picker. Developing investors get enchanted by the ideology of long-term ownership and buzzwords like ‘asset-light business model’, but they learn almost nothing about investing by owning them for the few years the stock remains in their portfolio. For more advanced investors, on the other hand, there are no “fast and dangerous” situations where they could differentiate themselves from other investors and the market, producing added value with their hard-earned expertise.

Specializing in the sector as an investor doesn’t seem like a very attractive use of time either, because in the end, you are just buying teams and business models. Private equity seems, in every way, an easier and more sensible way to get nearly or completely similar exposure to unlisted companies in a portfolio than investing in serial acquirers.

5 Likes

I personally find those long-term charts to be distracting in a discussion because an investor’s return differs significantly from the stock’s return unless the investment horizon and the holding period are identical. For example, Talvivaara’s lifetime stock return was -100%, but for many who invested in Talvivaara, the return was even strongly positive, depending entirely on when they bought and sold. So yes, the value created on paper looks sweet in these cases, but in practice, virtually no investor has achieved that theoretical return because such holding periods are completely unrealistic.

You probably mean it’s difficult for the average investor to achieve these long-term returns? I do have a couple of stocks that I’ve held for a very long time, and the returns have been good/excellent. The world is full of examples of this. The correct way to say what you’re trying to say is: it’s generally difficult and few people do it. Index investors face the same difficulty, and I recall reading a study about why, ironically, index investors lose to the indices for this very reason—because they try to time the market.

Another thing is allocation; I have about 5% of my net worth in this stock—a small number in percentages, but a six-figure sum nonetheless, so it does mean something to me if it performs well. Then I have more exciting investments; as an example, a company few know called PolyPid (PYPD), which recently published strong phase 3 results, but the share price barely reacted. You get excitement from these, and short-term returns can be triple-digit, but the risk is also quite high. In my opinion, it’s not quite binary anymore here, though there’s still a risk of a poorly timed share issue. I think it’s quite logical to have stocks with different risk profiles in a portfolio, where the likely holding periods also differ. Allocation strategies, of course, vary between investors.

You are indeed talking in practice about the challenges the average investor faces, and you are not wrong when you refer to the average. However, I see it as illogical in the sense that the most sensible strategy for the average investor is, of course, index investing—and specifically a “buy and forget” approach, because timing usually goes wrong on average. Trying to fill a portfolio with picks like PYPD won’t end well for the average investor, nor will any other strategy seeking quick returns. For the average investor, that is. Therefore, that whole argument about impossibility is quite moot, as you could similarly dismiss almost any case or strategy seeking alpha as impossible for the average investor ![]()

3 Likes

I agree with this in the sense that I wouldn’t build the foundation of my portfolio with these, but I have come to the opposite conclusion regarding the comparison of serial acquirers vs. PE funds, as I explained earlier. In my opinion, tracking a company like Röko doesn’t take much time, or at least it doesn’t for me. This is certainly not a sure thing, I don’t mean that, what investment is?

6 Likes

Well, well, well!

This time the target is a market leader in the rotisserie grill game (how do you even translate that into Finnish ![]() ).

).

- 93% ownership stake in Fri-Jado Holding BV

- Revenue approx. €64m

- 220 employees

- No significant impact on Röko’s earnings for this financial year.

20 Likes