EPS was a negative surprise; I’ll have to calculate some kind of bridge from EBITDA to EPS when I have the time. 2026 EBITDA is still rising, and apparently the order backlog is good. Let’s wait for developments, but in any case, 2025 is significantly better than Reka Kumi has seen in its history. Specifically, the 2025 EBITDA was, as I understand it, the highest in history and will rise in 2026.

1 Like

And when you strip out the net cash from the figures, last year’s P/E is 5. And the forecasts show earnings growth.

2 Likes

It’s a bit annoying that Markku Rentto is sitting on that pile of cash and not putting it to work. I also fell for buying it back in the day because of the good dividend, but now I guess I’ll be holding it until the end of time at a 50% loss.

1 Like

It would have been nice to get more information on the use of capital again. I believe that acquisitions are being scouted constantly in addition to these investments made in production. Hopefully, something good can be found at a reasonable price… otherwise, I’d gladly see the excess cash on the balance sheet in the owners’ pockets, please. This uncertainty is likely the biggest driver of the share price, at least in the short term.

If EV is now approx. €6M (mcap approx. 26M and cash minus interest-bearing debt approx. 20M), EBITDA €2.5M and EBIT €1.157M, then

EV/EBITDA = approx. 2.4

EV/EBIT = approx. 5.19

Yes, but: P/E is indeed over 22. Capital isn’t really generating much of a return here right now.

Does Reka provide any guidance on how much the cash position yields? Or is it just in a zero-interest account?

Personally, I’m fine with them sitting on a pile of cash; essentially, it’s the cash position + a cheap business. Of course, I’m a bit skeptical about what they might find to buy.

At the end of 2025, the group’s cash and other financial assets were 30.0 million euros (31.12.2024: 26.4 million euros). The group’s other financial assets are mainly invested in low-risk investments.

Something like that right on the first page of the financial statements. Financial income of €1.468M is recorded for this year, but in theory, it could partly come from something else I haven’t noticed.

Yeah, I meant more along the lines of whether they’ve commented at all on the cash pile yielding X% per year. Of course, now that I think about it, in a company like this, basically all financial income should come from the cash reserves.

1 Like

Yes. I don’t believe the company can be made to grow with just rubber studs. Even the Aura factory dates back to the 70s. It has been slightly renovated now. There are old machines sitting idle. They need to come up with something more productive.

Granted, it’s a bit like cherry-picking if you remove the net cash from the enterprise value but don’t remove the financial income from that net cash from the earnings ![]()

8 Likes

I’ve kicked off my own coverage of Reka. The operational business seems to be running consistently poorly, but the balance sheet-based valuation looks quite interesting.

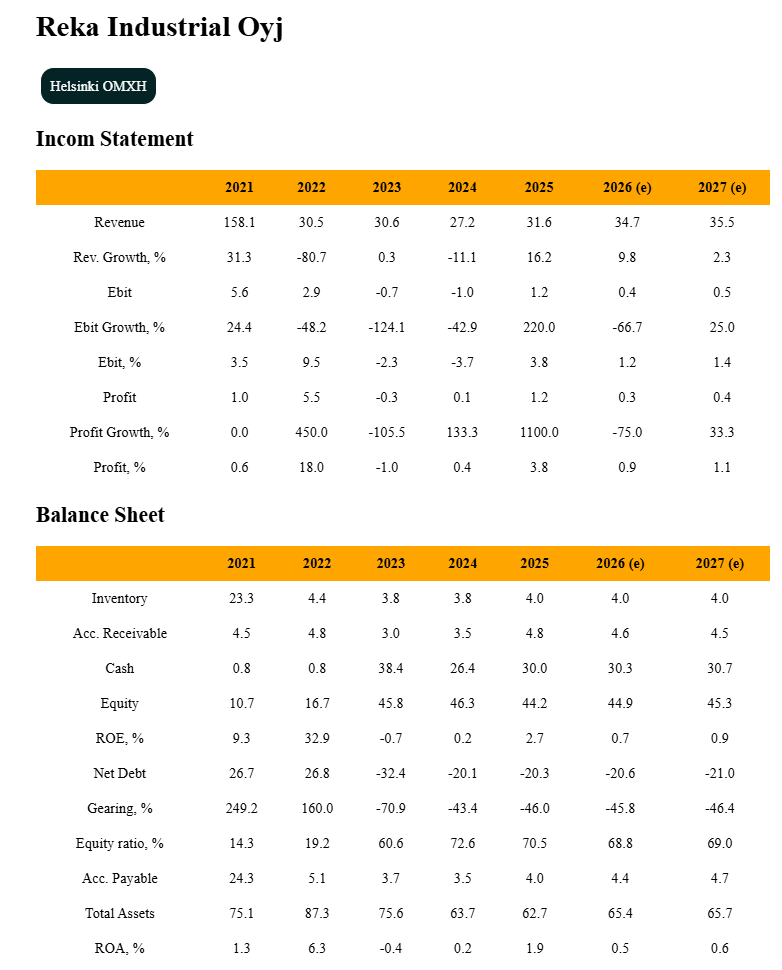

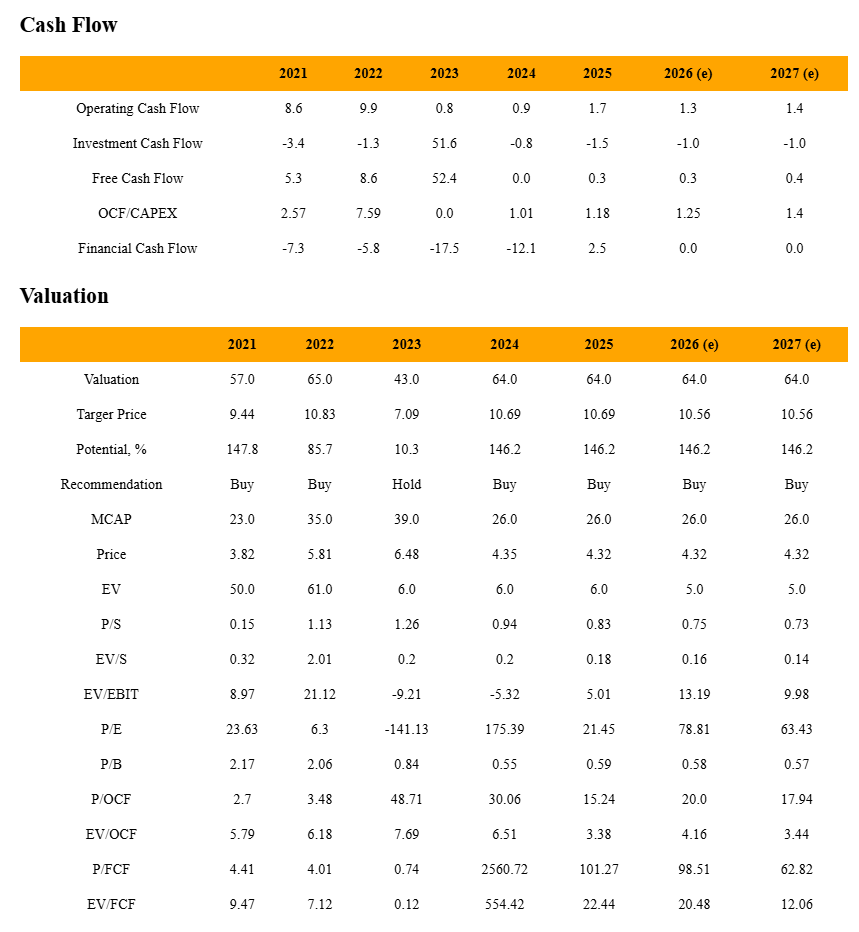

There is about 20 million in net cash and about 30 million in the bank account, which could significantly impact the current share price level. Share buybacks would be good for the share price development. The market cap is only 26 million and the valuation level based on the P/B ratio is approx. 0.6, which feels quite low. Of course, it’s possible that the operational business won’t really head in a better direction in terms of results at any point and the money will just sit idle in the account. However, EV/EBIT 10-13 looks quite attractive for the coming years. Reka receives a Buy recommendation with a target price of 10.56 euros. Reka Industrial Oyj - Financial Summary and Valuation

12 Likes

Where do two-thirds of the operating profit and three-quarters of the net profit disappear to with guidance of growing EBITDA?

1 Like

Forecasts are 100% based on mathematical models. Guidance or other narratives have no impact on the forecasts. However, the forecasts can be influenced to some extent by choosing a different model. Reka’s operating profit development doesn’t seem very predictable, which is likely reflected in the forecasts. Perhaps profitability is disappearing into the establishment of the Ukrainian subsidiary.

3 Likes

Great reflections here! I was on the parent company’s board for years. I haven’t been involved in any way for a couple of years now. The company’s situation seems to have stabilized, and the recent communication is very clear. Growth is being sought from rubber, and they are looking for ways to put their cash to use. The situation will resolve itself in due course. The stock is readily available, and I decided to jump in with a reasonable position. #V

9 Likes

You seem to know the company and the main owner reasonably well. Any guesses as to what that cash will be used for and on what timeline? I’m not looking for an exact target, but just some general direction?

3 Likes

I am not guessing or speculating, but in my opinion, the company’s announcement says it quite clearly: “Reka Industrial’s strategy aims to increase shareholder value through corporate transactions. This is backed by strong expertise in industrial manufacturing and international operations, complemented by our entrepreneurial way of operating. Based on these strengths, we identify and evaluate new opportunities and continue to develop our operations.”

5 Likes

Reasonable growth in Q1 revenue. According to the comments, volumes grew, so it wasn’t just price increases.

Uncertainty was emphasized, which was expected given the industry and raw materials.

January–March 2026

- Rubber segment revenue was 8.5 (7.9) million euros

- Rubber segment EBITDA was 0.9 (0.9) million euros

- Group revenue was 8.5 (7.9) million euros

- Group EBITDA was 0.6 (0.5) million euros

- Group operating result was 0.3 (0.1) million euros

- Group result for the period was -0.1 (0.2) million euros

- Group cash and other financial assets totaled 29.4 million euros on 31 March 2026.

Projects in Ukraine are progressing; a subsidiary has been established and production facilities are being sought.

Attention has been paid to sales efforts and pricing dynamics, which is essential in the current market.

Nothing significant in the outlook as far as I can see.

Near-term outlook

The rubber segment continues to improve productivity and profitability while creating further conditions for future growth. Investments continue in long-term growth, supported by our investment in production technology that is lower-emission and consumes fewer natural resources.

EBITDA in 2026 is expected to be better than the previous year.

The company continues to explore corporate restructurings.

The decisions of the Annual General Meeting seem to be as expected. Dividend €0.09

In accordance with the Board’s proposal, the Annual General Meeting decided that a dividend of 0.09 euros per share will be paid for the 2025 financial year. The dividend will be paid to shareholders who, on the dividend record date of 28 April 2026, are registered in the company’s shareholder list maintained by Euroclear Finland Oy. In accordance with the Board’s proposal, the Annual General Meeting decided the dividend payment date to be 6 May 2026.

6 Likes

April–June 2026

- Rubber segment revenue was EUR 8.9 (8.4) million

- Rubber segment EBITDA was EUR 1.0 (1.1) million

- Group revenue was EUR 8.9 (8.4) million

- Group EBITDA was EUR 0.8 (0.9) million

- Group operating profit was EUR 0.5 (0.6) million

January–June 2026

- Rubber segment revenue was EUR 17.5 (16.3) million

- Rubber segment EBITDA was EUR 1.9 (2.0) million

- Group revenue was EUR 17.5 (16.3) million

- Group EBITDA was EUR 1.5 (1.4) million

- Group operating profit was EUR 0.8 (0.8) million

- Group profit for the period was EUR 0.6 (0.9) million

- Group cash and other financial assets totaled EUR 29.5 million on June 30, 2026.

Steady grinding along, there really isn’t even much more to say ![]()

There is cash in the bank, they should do something with it. The rubber business is chugging along steadily. If industry picks up a little, perhaps it will eventually rub off on Reka, too ![]()

6 Likes

“At the end of the reporting period, the group’s cash and other financial assets totaled 29.5 million euros (30.0 million euros on Dec 31, 2025). Financial assets have been invested primarily in low-risk investments and short-term deposits.”

In addition, operating cash flow for H1 has been 1.2M EUR.

Some investments have been made, even though the CAPEX is not disclosed. Hopefully, they will increase Gumi’s volumes and profitability sensibly. The cash position is inefficient, and there is still no information on how it will be used. They have missed out on quite a lot of alternative returns by hoarding cash for years. In my opinion, this is not entirely hindsight.

8 Likes

The Aura rubber factory was supposed to be renovated. I visited there a couple of years ago. Old machines and facilities. The entire board of directors resigned/was dismissed a while back. Rentto was the only one left. I wonder if there was a disagreement over the 30-million investment. I also fell for the big dividend and bought in, and now I’m down over 50%. It’s amazing how there’s just nothing worth buying out there. Even the return on cash is miserable.

3 Likes

I read through this again with a critical eye. There were quite a few negative surprises, although the Q2 performance cannot be considered particularly excellent either.

Regarding the future, however, there was a bundle of positive factors that will apparently materialize during the autumn, boosting both revenue and earnings:

- “Reka Kumi has passed on the rise in material prices to the sales prices of rubber products in accordance with customer agreements, but it has not yet been possible to update the prices for all customers; this will happen with a delay. A large part of the increases will be realized during the second half of the year.” → an effect that will improve revenue and, in particular, earnings

- “The sales organization, strengthened during last year, has invested in active customer acquisition, and the work has already produced results that will be reflected in revenue later.” → Organic growth has been sought, and results have started to show. Good news, especially as production efficiency has improved at the same time.

- “During the beginning of the year, several investments were decided upon to increase production capacity and develop production technology. The subsidiary established in Ukraine acquired production facilities in the city of Novoselytsia, and its goal is to start the production of silicone products there after the necessary modifications in early 2027. Moving the production of silicone products from Poland to Ukraine frees up much-needed space to increase the production of black hoses at the Dopiewo plant in Poland. In June, it was decided to purchase two new injection presses for the Aura plant and a new braiding machine for the Dopiewo plant.” → In the short term, the balance sheet shows a couple of million used for investments, but these have clear effects on improving capacity and efficiency. Larger investments supporting organic growth and longer-term returns make sense when there is an immense amount of cash, especially if that new customer acquisition and growing volume trend continues.

Overall, it is a positive report, with the slow pace of execution being its weak point. The EBITDA guidance was maintained (growing compared to the previous year), which means continuing profit improvement for the autumn.

Admittedly, that immense cash pile and its yield is a big question mark; if a good solution could be found for that, the share price could head towards the northeast. If there is nothing to acquire, they could always distribute an extra dividend or buy back their own shares from the stock exchange.

4 Likes