Let’s open a discussion forum specifically for valves. This valve business is undoubtedly challenging for small investors, as few of us deal with industrial valve solutions and flow technology on a daily basis.

Even before the listing, Valmet announced that it had acquired a stake in Neles:

Neles is a good and high-quality global company, a large part of whose business is recurring, and which has a strong position in the pulp and paper industry. The company has shown its ability to achieve good growth and has the potential to continue growing. Today, we have agreed to acquire a minority stake in Neles, and our goal is to increase our ownership when the share price of Neles supports the purchase of additional shares. Valmet’s goal is to be actively involved in Neles’ development over the long term. The strategic rationale for the share acquisition is also supported by the fact that Valmet and Neles have a common history, the companies serve the same global industries, and they benefit from the same megatrends.

Pasi Laine, CEO of Valmet, June 17, 2020

Information about the upcoming Neles Corporation

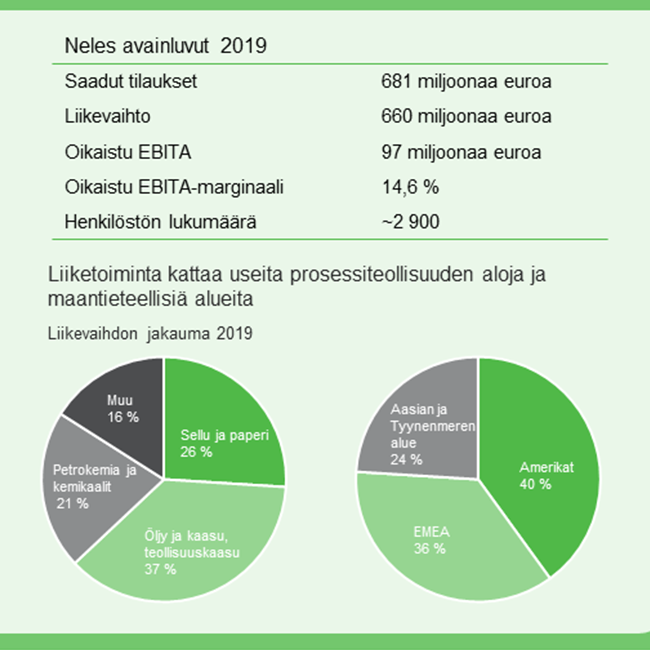

The upcoming Neles Corporation is a renowned provider of flow control solutions and services. It serves the oil and gas refining industry, pulp, paper and bioproducts industry, chemical industry, and other process industries. Neles has 2,900 employees and operates in over 40 countries. Neles’ audited 2019 carve-out revenue was 660 million euros and carve-out operating profit was 93 million euros.

Source:

https://www.metso.com/fi/uutiset/2020/5/tulevan-neles-oyn-virtuaalinen-paaomamarkkinapaiva-2020/

Neles is a globally leading valve, valve automation, and services company with a strong position in the pulp and paper industry. Approximately 70% of Neles’ revenue comes from recurring business. Neles’ business covers several process industries and geographical areas, with 26% of the company’s revenue coming from the pulp and paper industry. Since 2011, Neles’ received orders have grown by approximately 5% annually, and profitability has improved.

Figures source: Neles CMD 2020

Brief history of the upcoming Neles Corporation

The first in the industry

From the beginning, it was clear that only a metal-seated valve would work in these conditions. However, such a valve had never been designed before. After two years of intensive work, Neles’ product development team presented the product now known as the Neldisc valve. The U-shaped metal seal and elliptical disc formed a unique triple-eccentric valve structure that we are accustomed to seeing in many current butterfly valves. Neles’ version was the first in the industry.

The first deliveries at the end of 1975 exceeded all expectations, and the valves proved to be bubble-tight even at high temperatures. The product incorporated many innovations related to its structure and manufacturing technology. When the product development project ended, intellectual property rights for the revolutionary combination of the elliptical disc and metal sealing ring had been secured in 13 countries.

More information:

https://www.metso.com/fi/showroom/oljy-kaasu/yli-40-vuotta-luotettavia-lappaventtiileja/

Summary

Overall, the upcoming Neles Corporation has been described in many contexts as a strong player in its field and a global leader, with the majority of its revenue coming from recurring business. Due to its market leadership, defensive nature, and future growth prospects, I see Neles as an attractive investment case.

What do you think?

Let’s also add a link to the company’s brand new website: