Thanks @Petri_Gostowski, I also hope to get some discussion going regarding Neo. I was a bit surprised when I couldn’t find a thread, even though it’s covered by Inderes.

I personally got into Neo with a somewhat superficial understanding, based on the H1 report predicting a turnaround and a corporate arrangement supporting operations. I’ve gradually learned more about the business, and in the long run, I do trust this as a turnaround company in line with my investment strategy.

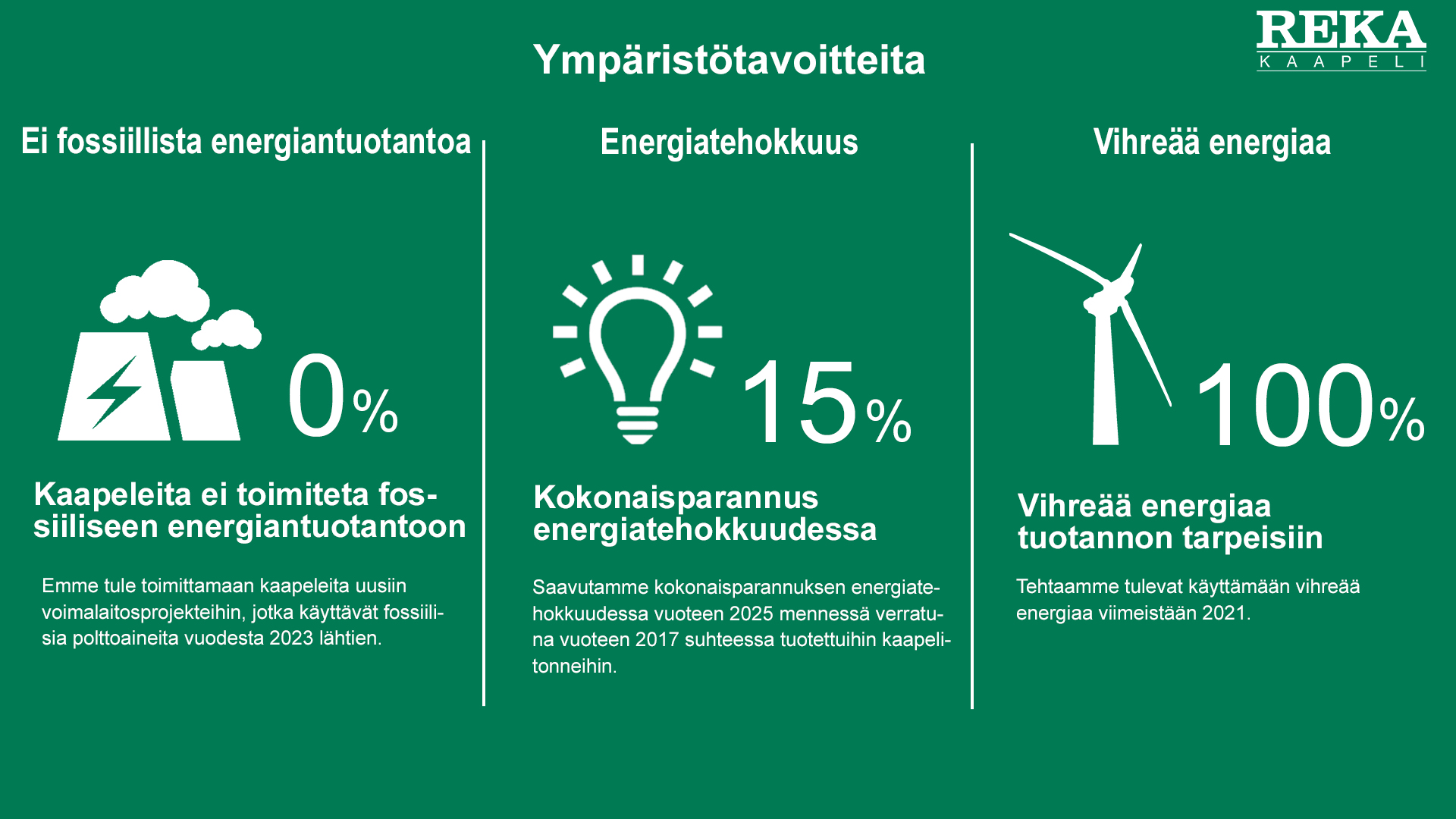

How do you see the addition of Reka Rubber affecting the portfolio in the future? The comprehensive report mentions “…the company is currently profiled as a turnaround company. In the long term, we estimate that the company aims to profile itself as a growth company, but the growth company profile is weakened by the fluctuating demand in the cable industry. A growth company profile would require expanding the investment portfolio…”

And from Neo’s H1 report: “If Reka Rubber had been acquired on 1.1.2020, the group’s revenue would have been 65.9 million euros, EBITDA 4.5 million euros, and operating profit 1.6 million euros.”

The rubber business is apparently much more profitable and even a larger industry than cables. With this arrangement, one could expect the operating profit to turn clearly positive for this year, if H2 continues at the same level? Are there potentially other arrangements still to come, which would expand the portfolio?

In addition, the balance sheet took a step in the right direction in the H1 report:

“The Group arranged the ownership of a property located in Keuruu, which was owned by an external party. Neo Industrial Oyj purchased the said property for a purchase price of 1.0 million euros using the purchase option in the previous lease agreement and sold it further to Reka Pension Fund at the fair value determined for the property, 2.2 million euros. A 10-year lease agreement was made with Reka Pension Fund. The fair value of the property was determined by external appraisers. With the financing generated by the arrangement, Neo Industrial Oyj paid off its short-term loan of 1.2 million euros. The arrangement had no significant impact on the result.”

Does this apparently ease potential future arrangements and lighten the capital needed for short-term financing?

The cross-ownerships of the Group with Reka Oy are a somewhat confusing combination. Neo Industrial is part of the Reka Group, but nevertheless owns Reka Kaapeli (Reka Cable) and Reka Kumi (Reka Rubber) companies. Is there any essential reason for this, or does it have any practical impact on daily operations?