This is a US fast-casual restaurant chain founded in 1963, originally from Chicago. The company currently has 85 restaurants in ten states in the US. Their goal is to increase the number of restaurants to approximately 500. The company has never closed a restaurant in its history, meaning all locations are profitable.

The company is so popular in the States that when they open a new restaurant, there are hours-long queues during the opening week.

40% of the restaurants’ sales come from drive-thru lanes, and the average spend per person is $10.75.

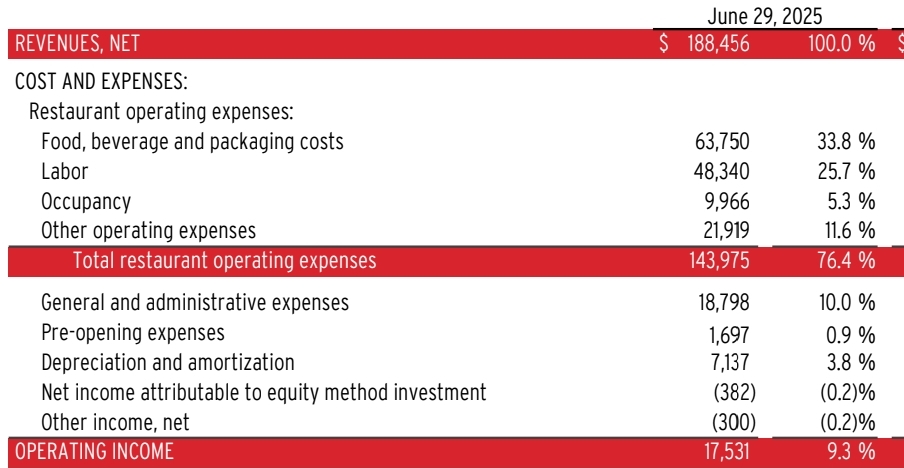

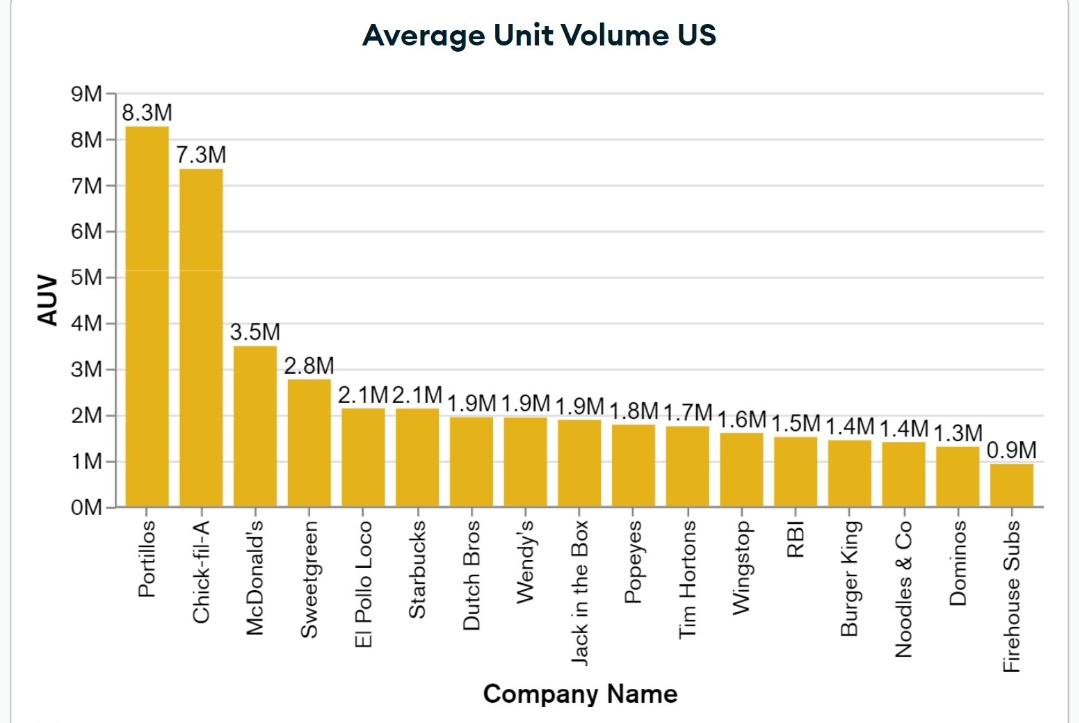

Annual sales per restaurant are approx. $8.3M, which is significantly higher than their competitors.

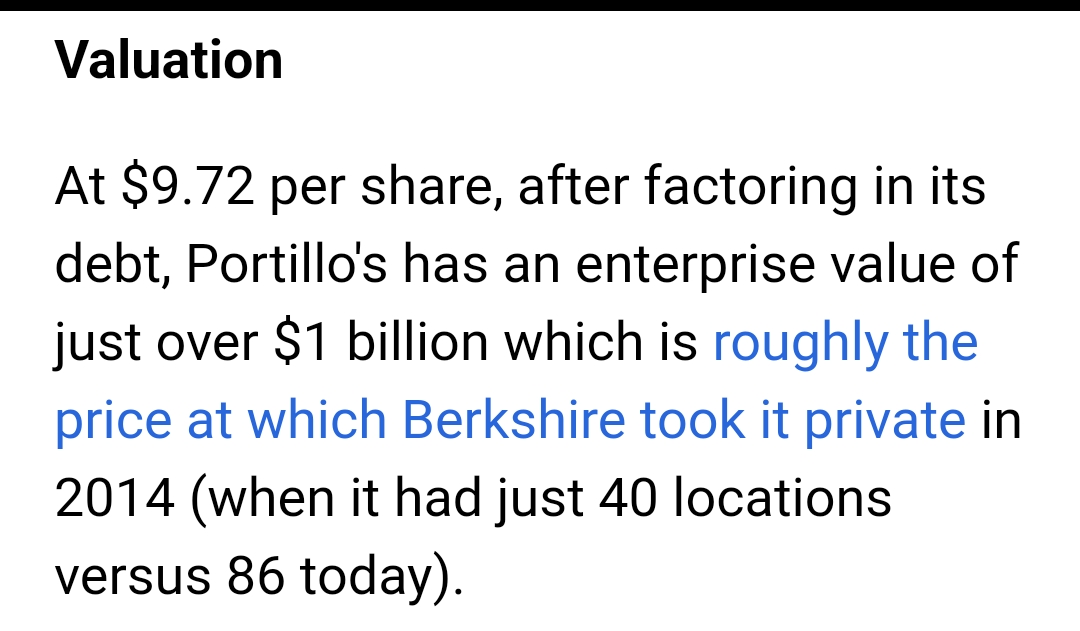

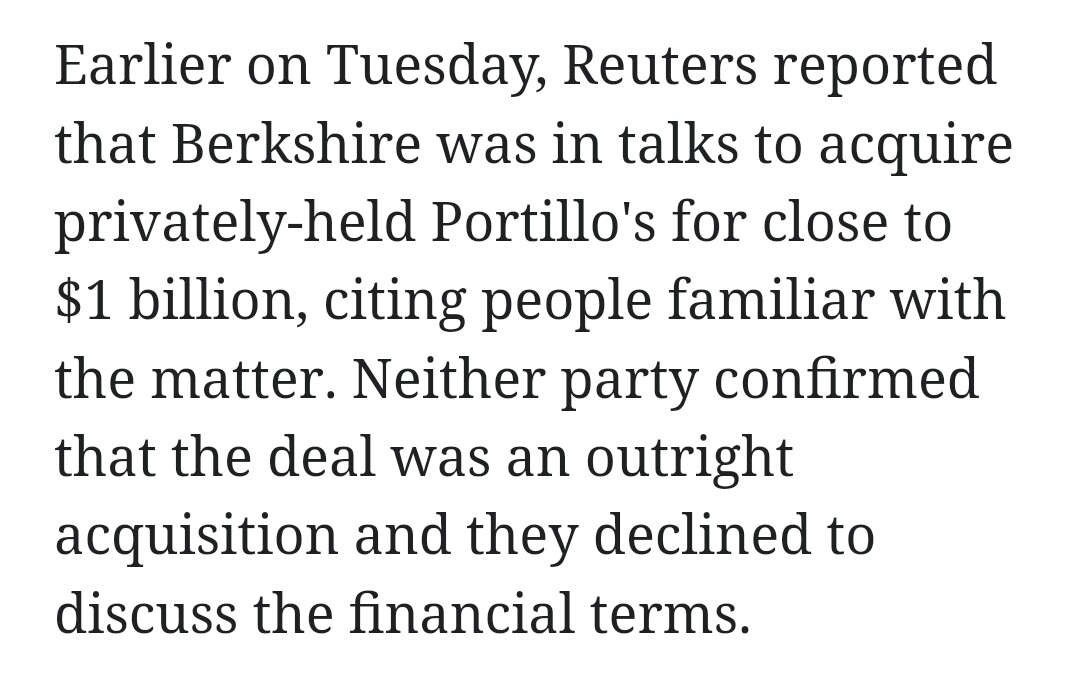

In 2014, the chain was sold to a private equity firm named Berkshire Partners, which took the company public in 2021. The IPO price at the time was $20 per share.

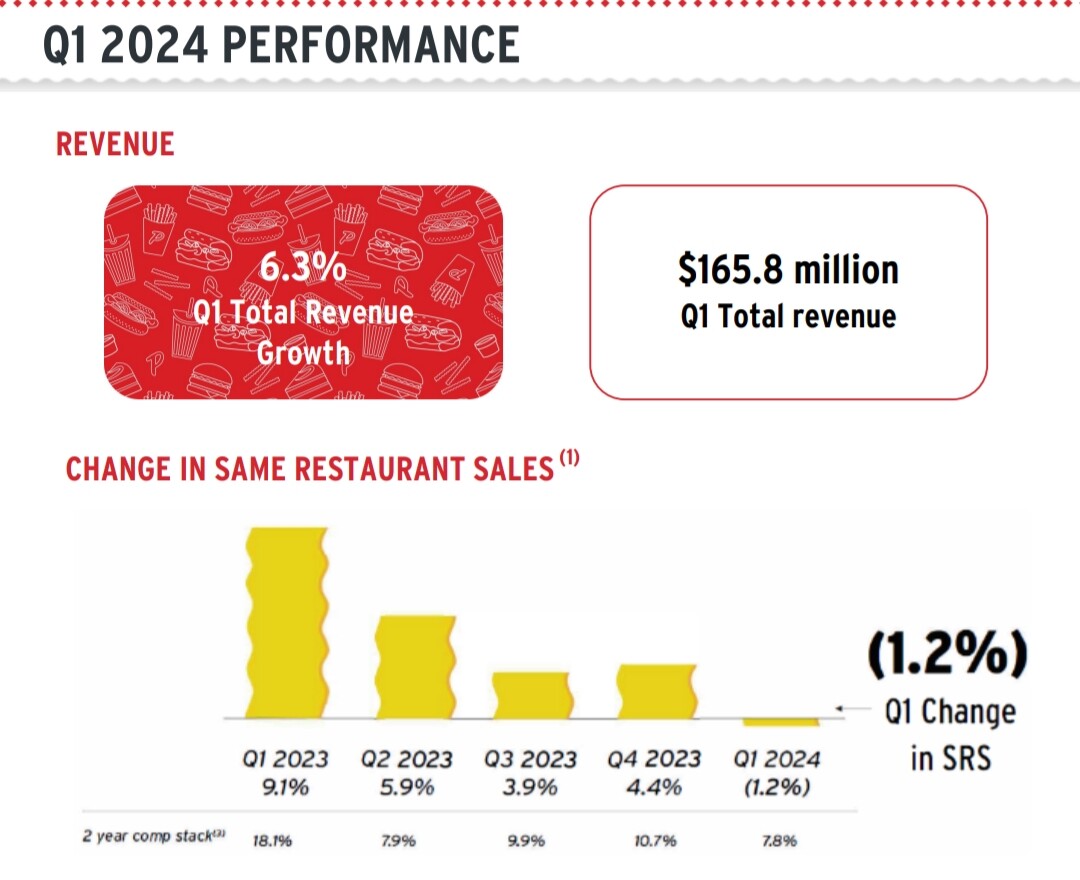

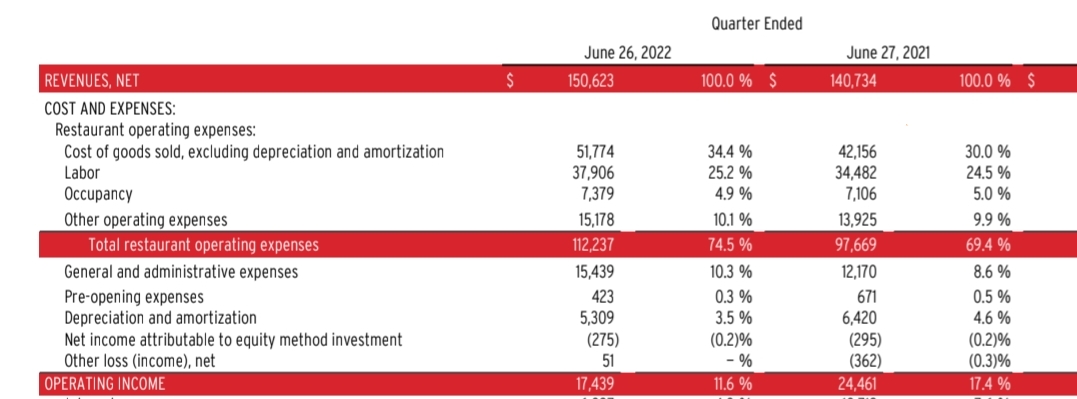

The company has grown its revenue at an annual rate of approx. 10-15% in recent years and aims to keep growth in the 12-15% range in the future. The company’s growth is partly slowed by the fact that the company owns all the real estate itself and funds growth directly from operating cash flow. Building a new restaurant costs approx. $7M, but according to the company, construction costs can be pushed down to around $5.5M with their new restaurant concept, where the kitchen will be smaller and more efficient. A newly opened restaurant also generates positive cash flow immediately.

The company has two classes of shares listed: Class A shares and Class B shares owned by the private equity firm. However, the company regularly buys those B shares and converts them into A shares, which increases the trading volume of the listed stock without diluting ownership. There are still 11.6M B shares left for the company to redeem, while there are 61.6M A shares.

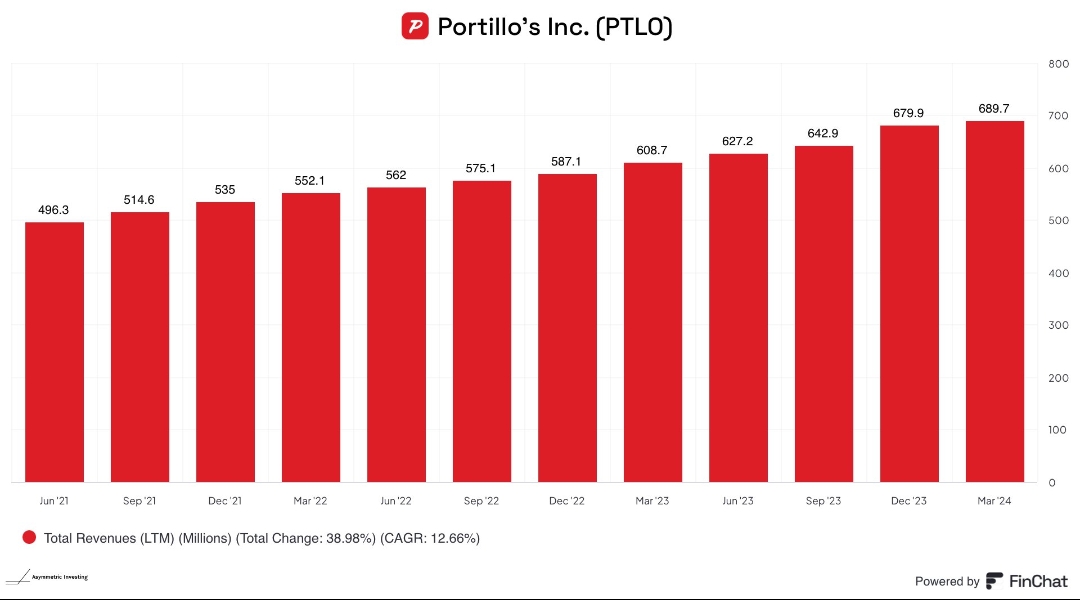

What makes this interesting is that the company’s EV/EBITDA multiple for this year is 11.3, while the average for listed US restaurants is 16.6—even though the company is growing at double-digit rates.

At the beginning of this year, activist investor Glen Welling bought a 3.5% stake in the company; he has also done good work at Shake Shack. I believe he will try to get the company to sell the real estate on its balance sheet, which would increase the company’s return on capital and free up more cash for growth. Additionally, he typically places his own people on the board. Glen mentioned in an interview that his only job in a company where he buys a stake is to figure out how to drive the stock price up.

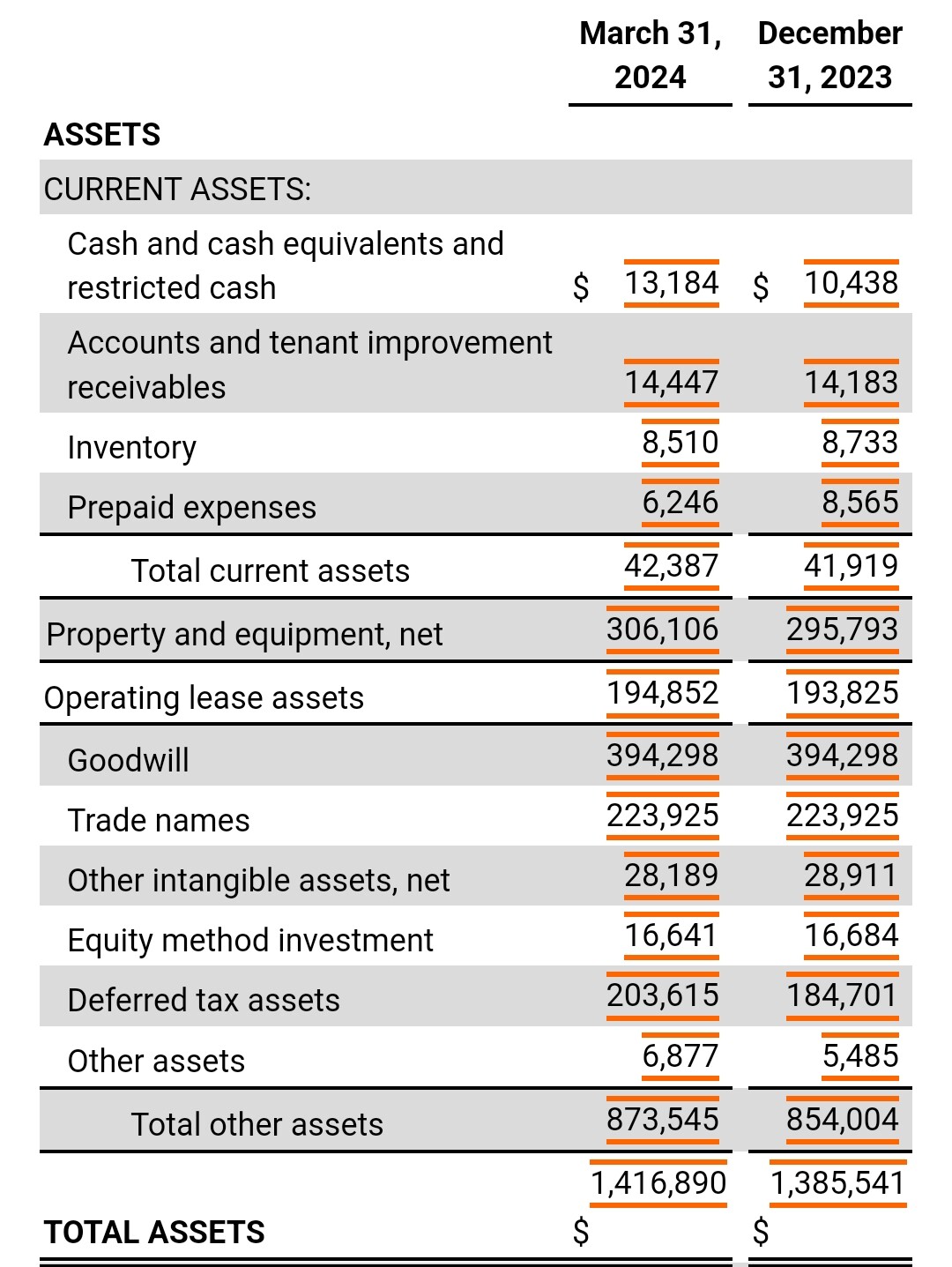

They have $306M worth of real estate on the balance sheet, and if building a new restaurant costs $7M, selling those 85 restaurants could bring in more money than the $306M currently on the balance sheet.

Figures:

Below is a customer experience from the restaurant and an interview with the CEO.