Redeye Q1 previews

- Strong comparison period (Q1/23), so growth figures may be relatively weak.

- Cash flow is of more interest at this stage.

- Larger new contracts were predicted for H1/24. None have been announced yet, putting pressure on Q2.

Redeye Q1 previews

10% organic revenue growth year-on-year, EPS +/-0 and cash flow positive for the second consecutive quarter. ![]()

The focus has been on larger contracts providing recurring billing instead of individual projects. This is finally starting to show, as H2/23 was quite sluggish due to these actions. A better foundation for continued growth is ahead ![]()

Physitrack PLC – Interim report: January – March 2024

We are pleased to report significant growth in revenue and EBITDA, as well as two consecutive quarters of positive cash flow generation. This reflects our continued success in expanding our market presence, optimising operational efficiency, and delivering value to our stakeholders.

Quarter ended – Jan – Mar 2024

- Revenue increased by 10 per cent against a strong comparator to generate total sales of EUR 4.1m (EUR 3.7m). On an organic basis revenue grew by 10 per cent. This organic growth was achieved in both the Lifecare (10 per cent) and Wellness (11 per cent) divisions.

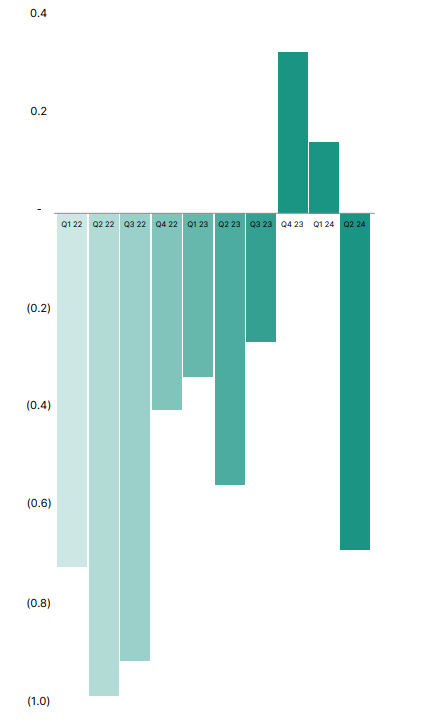

- Subscription revenue increased 23% (€618k) to €3.3m and now makes up 80 per cent of total group revenue, a significant increase from the prior year’s comparative, which was 72 per cent.

- Adjusted EBITDA of EUR 1.1m (EUR 0.9m) was generated resulting in an Adjusted EBITDA margin of 26 per cent (25 per cent).

- Adjusted operating profit of EUR 0.1m (EUR 0.1m) was generated resulting in a margin of 1 per cent (3 per cent).

- Adjusted ordinary and diluted profit per share totalled EUR 0.00 (EUR 0.00).

- Cashflow generated from operations before the payment of adjusting items equalled EUR 1.0m (EUR 0.7m).

- Free cash flow for the quarter was a net inflow of EUR 0.1m (outflow EUR 0.4m).

A couple of highlights from the comments

Champion Health secured significant contracts during the quarter, including the Cabinet Office, Network Rail and ACCA. Champion Health has a strong sales pipeline, and these agreements support the continued growth of the Wellness division.

The Growth target will now be that Physitrack aims to achieve a doubling of revenue within the medium term, replacing the previous target set in 2021 that targeted an annual organic sales growth exceeding 30 per cent in the medium term).

Edit: Redeye’s quick comments

Redeye comments on Physitrack’s soild Q1 figures, which were in line with our expectations. Highlights include quarter-on-quarter growth, an annual recurring revenue (ARR) increase of 15% y/y, positive FCF, and Software as a Service (SaaS) revenues now constituting 80% (71%) of total revenues. Consequently, we anticipate moderate adjustments to our near-term estimates and fair value range.

Redeye’s broader review - no surprises relative to expectations, a good start to the year

these points should be highlighted ![]()

ARR increased by 15% year-on-year, reaching EUR13.0m, surpassing our estimate by 6% and showing an 8% quarter-on-quarter growth. SaaS revenues now constitute 80% of total revenues, up from 72% last year, indicating a 23% year-on-year rise. We appreciate this shift towards SaaS revenue for its better margins and recurring nature

Accordingly, to management, 1/3 of the y/y growth is attributed to price increases and 2/3 to volume increases. Despite annual price hikes, churn levels trended inversely, implying pricing power

And Henrik’s interview

Affärsvärlden has apparently written some good things about Physitrack, at least judging by today’s share price reaction.

Behind a paywall:

Summarized here:

Strong comparative period, with 5% revenue growth.

EPS and also free cash flow in the negative. Apparently, the development work for AI services is taking its share ![]() .

.

ARR, for its part, grew well by 21%

Second quarter: 1st April – 30th June 2024

- Revenue increased by 5 per cent against a strong comparator to generate total sales of EUR 4.0m (EUR 3.8m). This growth was achieved in the Lifecare division (10 per cent) but was offset by a contraction within the Wellness division (2 per cent).

- Subscription revenue increased 21 per cent (€0.6m) to €3.2m and now makes up 82 per cent of total group revenue, a significant increase from the prior year’s comparative of 71 per cent.

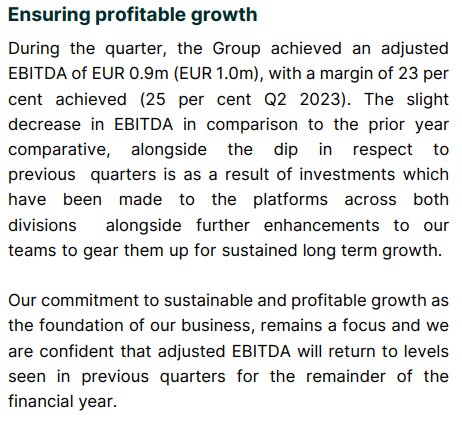

- Adjusted EBITDA of EUR 0.9m (EUR 1.0m) was generated resulting in an Adjusted EBITDA margin of 23 per cent (25 per cent).

- Adjusted operating loss of EUR 0.3m (profit EUR 0.1m) was generated resulting in a margin of -7 per cent (1 per cent).

- Adjusted ordinary and diluted profit per share totalled EUR (0.02) (EUR 0.00).

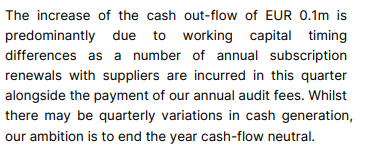

- Cashflow generated from operations before the payment of adjusting items equalled EUR 0.4m (EUR 0.5m).

- Free cash flow for the quarter was a net outflow of EUR 0.8m (outflow EUR 0.6m).

The previously advertised result of AI development as a new release:

AI-driven self-care - valuation multiples should at least triple now ![]()

Champion Health Plus, a division of Physitrack Plc, proudly announces the launch of its cutting-edge AI-driven musculoskeletal care platform, Nexa. This innovative platform offers self-triage, self-management, and seamless escalation to care professionals, providing comprehensive care through a national partner network of over 850 clinics across the United Kingdom.

Redeye’s comments, largely in line with expectations

Highlights from the CEO’s comments

Summary and upcoming revisions to estimates and valuation

- We note that the Q2 2024 report from Physitrack was overall in line with our expectations. However, we had hoped to see q/q growth from the Lifecare division and a slightly higher ARR. In the CEO letter, Henrik Molin states, “Despite the short-term challenges, I am confident that we will see a positive turnaround in the second half of 2024. We anticipate ending the year with positive cash flow and a return to margin expansion”.

And Henrik’s interview as well

https://www.redeye.se/research/1029824/physitrack-interview-with-ceo-henrik-molin-4

Summary of the current situation in the pitch thread

https://keskustelut.inderes.fi/t/pitchaa-paras-sijoitusideasi-kisa-kaynnissa/52900/10?u=kettunen

And views from Swedish retail investor OT Analytics

https://www.otanalytics.se/physitrack.html#portfolj

@kettunen Can you break it down simply—why do you have such clear confidence that the cash flow will break through now? Looking at this thread and the company’s performance from the IPO to the present, it’s been pretty much one disappointment after another regarding cash flow. Revenue is growing, but profitability is worse and cash flow is lagging (which has weakened the balance sheet).

So why will things turn around now? I am particularly interested in these two things:

Why are margins weakening all the time?

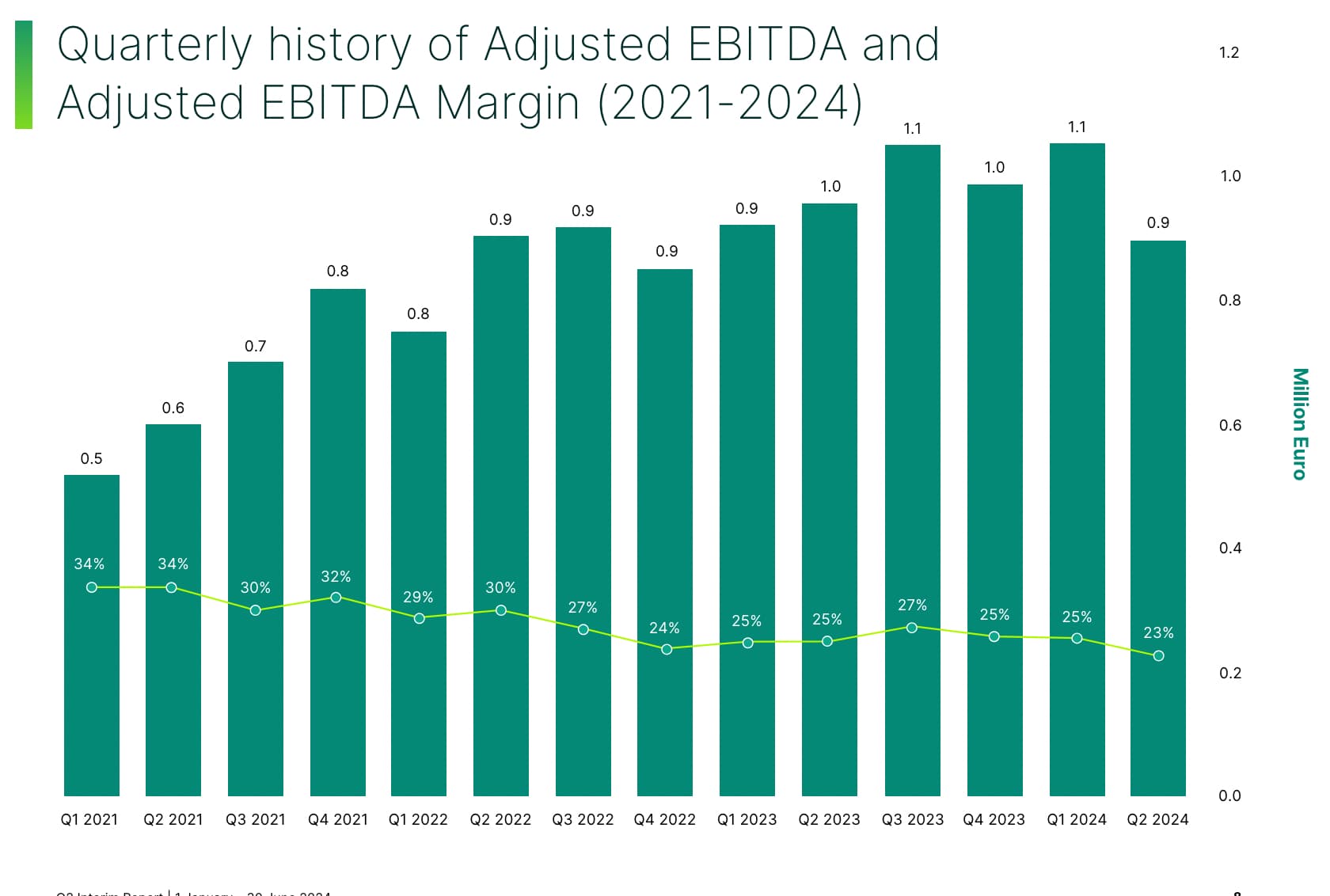

From the 34% level, it has dropped 11 percentage points to 23%, which is a very modest EBITDA% figure.

Can the balance sheet hold up without shitty loan terms or equity financing? In other words, will this turn around ASAP?

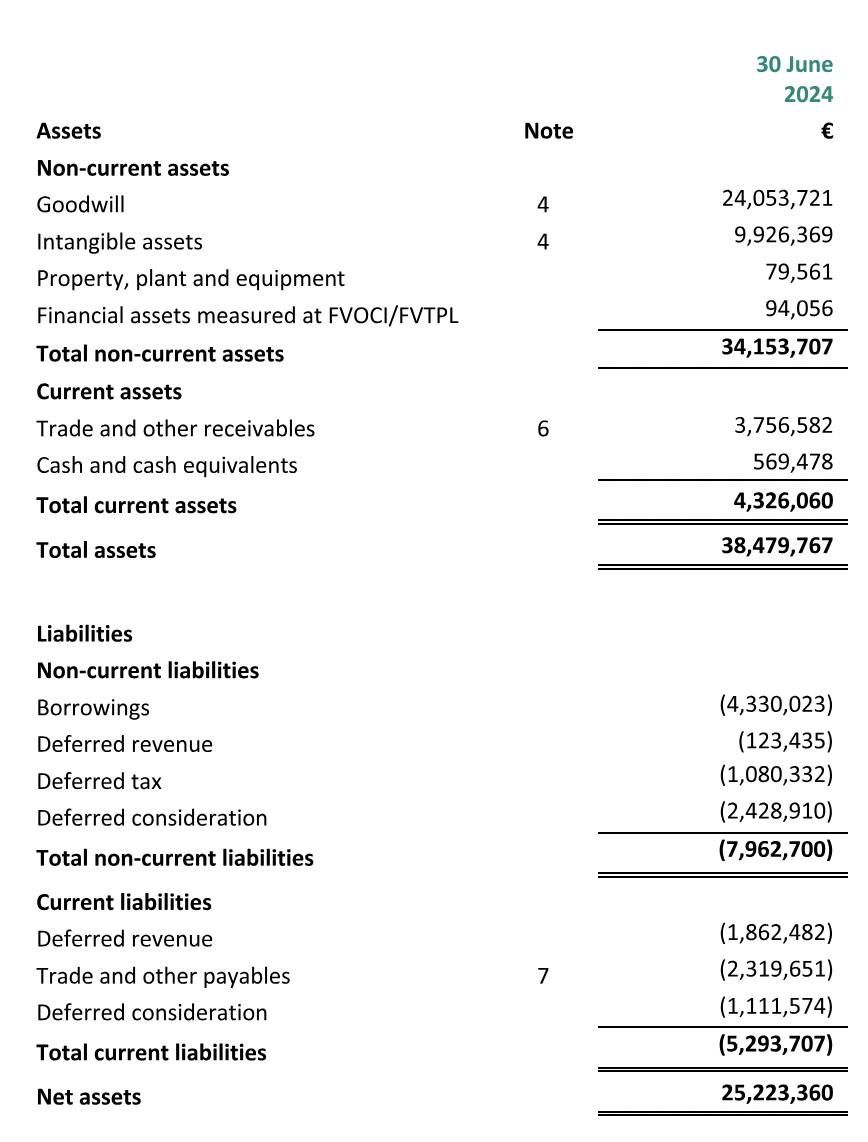

Just over half a million in cash and nearly 10 million in debt.

Regarding the balance sheet, it’s also a bit alarming that goodwill is such a large part of equity. It speaks to the recent pace of acquisitions and the industry itself, given it’s software business.

PS: By the way, adjusted EBITDA is a terrible metric for profitability ![]()

Profitability and cash flow have been weighed down by those multiple acquisitions, which were made with valuation multiples that were too high, partly during the COVID hype period when anything even remotely related to remote services was priced at a premium.

These also brought along earn-out payments (performance-based considerations). Most of these have been settled, but some have not been paid because targets were not met, and some have also been partially written down. These represent a relatively significant portion of the cash flow.

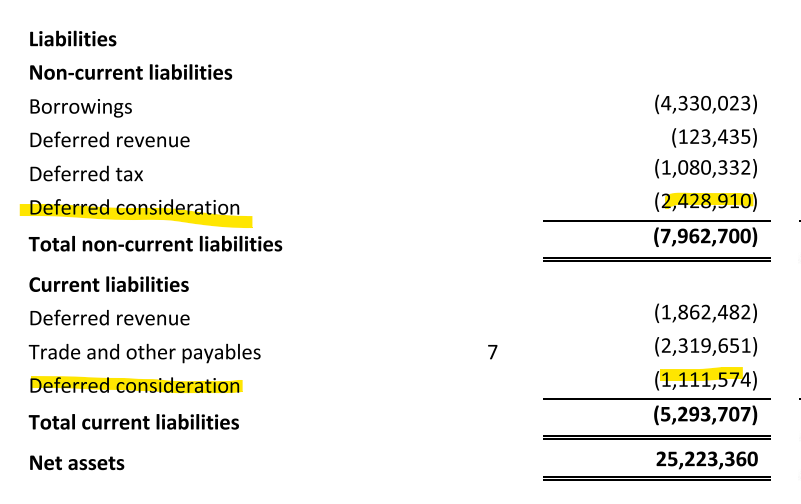

The remaining ones are visible on that balance sheet line “Deferred Consideration.” No more payments are due this year, and the final part of Champion Health is expected next year.

Another thing visible in the latest Q2 report is the licensing and maintenance costs for Physitrack’s platforms. During Q2, these are paid for the entire year, making the cost level heavier.

The recurringly heavier cost structure in Q2 is visible in the cash flow statement. Otherwise, the trend has been in the right direction. I personally didn’t expect any significant improvement yet, but growth was still lower than expected, and consequently, cash flow was weaker.

And thirdly, the development costs for the new platform. These are added to self-developed intangibles on the balance sheet and amounted to €1.7M in H1. The platform has just been released, and in this regard, costs should decrease, although software development obviously cannot be stopped entirely. The previous version of Champion Health has apparently hindered sales due to some missing features that are now included. According to the CEO, sales growth is about a year behind the target, partly due to this.

![]()

Growth has been lower than before for about a year because project-based new client accounts have been shifted to recurring billing. Previously, these contributed a good share of revenue, and especially margin, but as one-offs.

So, projects have not translated into recurring services, which they want to emphasize in the long term. In Q2, ARR grew by 21% (YoY) and already accounts for 82% of revenue. In other words, the previous one-off revenue and margin are now coming with a delay, but on a recurring basis.

Based on Redeye’s comments, investments in Champion Health’s growth have also been front-loaded in terms of personnel. This is directly reflected in EBITDA. Now they just need those sales.

we know that the number of employees increased in 2024, and the organization has been staffed to prepare for Champion Health’s upcoming market expansion. In other words, the cost base in 2024 has been front-loaded in anticipation of future launches. We do not expect the cost base to expand from Q2 levels, as the majority of the vacancies now appear to be filled.

This can also be found in the CEO’s comments:

And regarding the sales side:

The shift to emphasizing recurring services also brought with it the goal of pursuing larger customers, which would offer better overall profitability. There were a couple of larger customers in the pipeline for H1, but these have not been announced. So, they either fell through or moved to H2, which would obviously be desirable.

In the interview, there seemed to be a slight hint that there are new customer accounts but no “significant logos.” This would mean the focus is back more on the SMB segment, which in my opinion is a more sensible approach for steady growth. I need to listen to the interview again.

An addition regarding these earn-outs. So, €1.1M is visible on the Current Liabilities side and corresponds to the portion for Champion Health, which is due for payment in H1/2025.

The remaining €2.4M is split among acquisitions made over the last four years. It is likely that a very large portion of this part will not be paid, so the actual share of liabilities is significantly smaller.

Acquisition history over four years:

Physiotools Oy (2020)

Rehabplus (2021)

Fysiotest (2021), the earn-outs for this have already been written down at the end of last year.

PT Courses (2022)

Wellnow (2022)

Champion Health (2022)

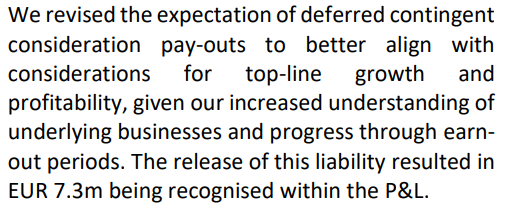

At the end of last year, as much as €7.3M (!) of these were already written off.

During 2023, €1.6M was paid out (portions of Wellnow and Champion Health).

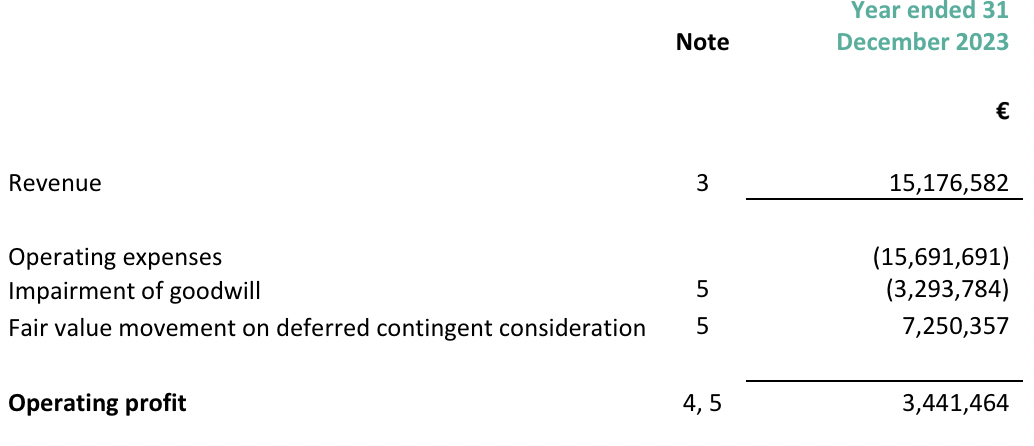

Correspondingly, €3.2M of goodwill was written down for Fysiotest, which reflects the high purchase prices ![]()

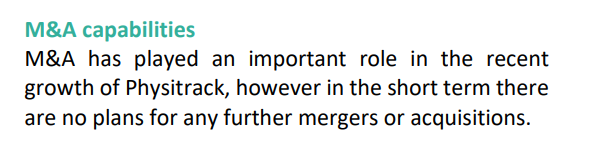

No new acquisitions are planned in the short-term strategy. From the 2023 annual report:

Thanks for the answers ![]() Especially that Q2 “seasonality” due to those license fees is a good point indeed.

Especially that Q2 “seasonality” due to those license fees is a good point indeed.

The company indeed capitalizes those software development costs on the balance sheet. Some companies do this, some don’t. Talenom from the domestic field does the same. This makes the reported result look better as expenses are amortized over different years, but the cash flow impact naturally occurs immediately. In Physitrack’s case, it highlights the need to look at the cash flow now and evaluate it for the upcoming quarters because the cash position is quite tight.

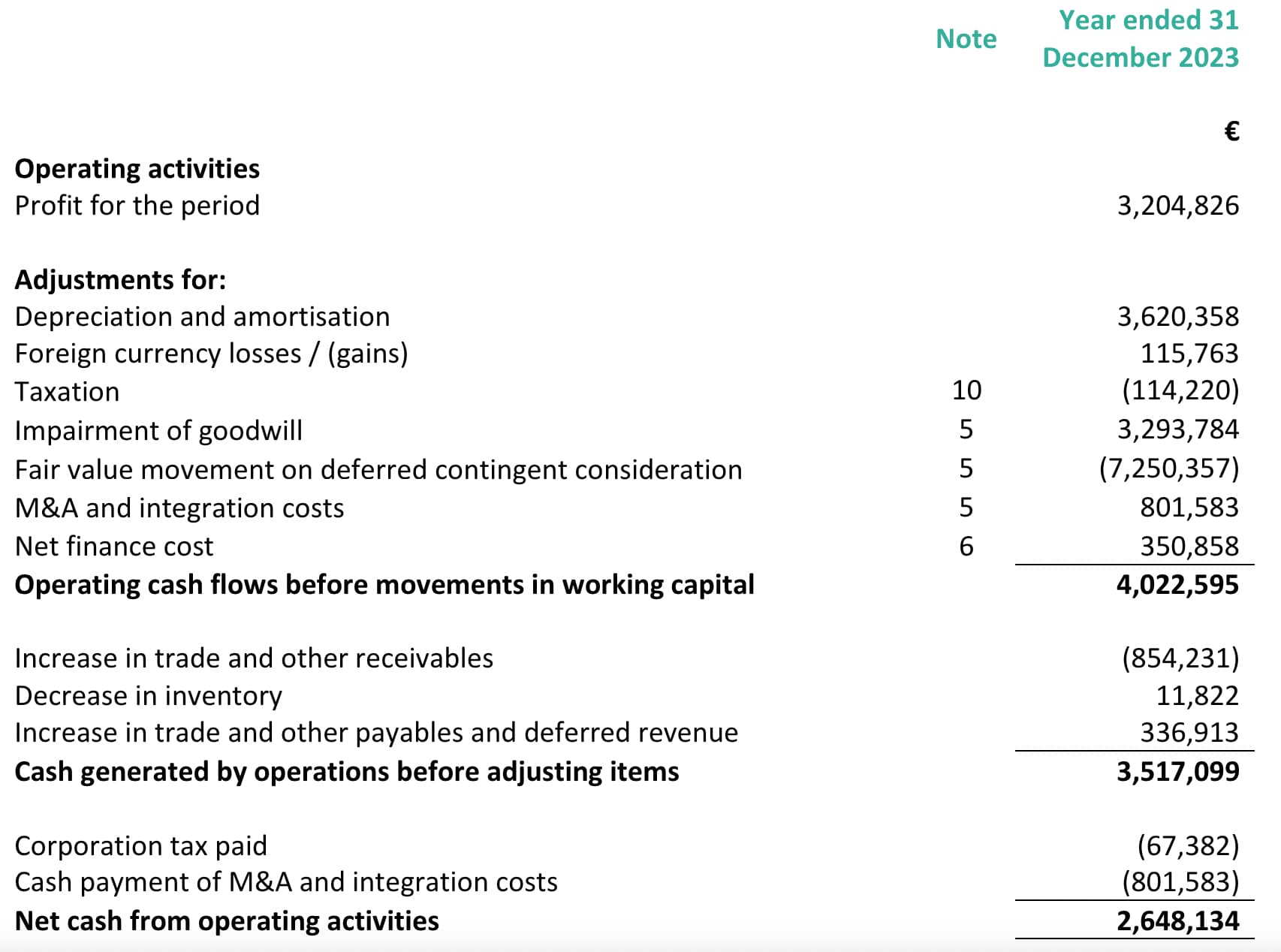

But indeed, those expensive acquisitions are past mistakes and now we must look to the future. Let’s try to estimate the cash flow adjusted for those; attached is the cash flow statement for the '23 financial year.

Could you break it down further @kettunen—so this “Fair value movement on deferred contingent consideration” is specifically those performance-linked earn-outs and nothing else? But what is that item in the investing cash flow section (“Payment of deferred contingent consideration”) then?

But do you think it’s likely that this line (above, a -7.25M€ burden on cash flow) will soon go to zero (for next year, there was only the remaining part of Champion Health)? Estimating software development costs is quite difficult; they tend to stay surprisingly high, and I don’t believe much relief is coming from there anytime soon.

Good point also that one-off revenue has now shifted to a recurring billing model!

Good questions, which always lead me to dig deeper myself ![]()

Movement refers to other changes, in this case, write-downs of the considerations from the balance sheet. In other words, a positive in the reported figures. So it also shows up in EBITDA for Q4/23.

Most of it relates to Fysiotest, but some also to Wellnow and Champion Health. I found it somewhere in the annual report when I was browsing through it earlier.

Payment, on the other hand, refers to what has been paid out, which was €1.6M during 2023.

FCF needs to turn positive during H2/24. According to Henrik, it should be breakeven or positive for the full year ![]()

So, is the logic here that because the fair value of these future earn-outs on the balance sheet was lowered, a one-time +€7.25 million entry was reported in the income statement, which then also had to be adjusted out of the cash flow statement? And the reason for this is that the acquired targets have performed worse than expected, so the magnitude of future payments has decreased by that much?

It really seems that the company’s fixed costs are too high and getting the cash flow into the black now simply requires growth. Of course, if software development costs decrease, that will help, but at least in 2023, depreciation and capex investments were already in the same ballpark.

Now that Q2, the worst quarter from a cash flow perspective, is out of the way, there are probably enough ingredients to get through at least H1/25 without additional external funding. Of course, bank loans and such are likely being reviewed constantly, but there probably isn’t any share issue risk (rights issue risk) in the coming months.

ADDITION:

By the way, the company’s reported 2023 result is REALLY misleading (relative to cash flow) because:

Now just more revenue, and this could actually turn into quite a good case.

Not from the cash flow, but from the income statement. Performance-based bonuses appear as provisions on the balance sheet according to the so-called worst-case scenario, i.e., that all bonuses would be paid.

So, €7.3M in liabilities were removed from the balance sheet, which then shows up in the reported result, and that is why the EPS for last year is indeed exceptionally high. Correspondingly, a one-off goodwill write-down of €3.2M was made for Fysiotest. But the overall impact is significant. Going forward, development costs will appear as amortization over time.

The CEO has consistently stated that share issues are not needed and that they will survive on internal financing and, if necessary, a credit limit. Belts were already tightened in the meantime when things were looking tight and a share issue seemed likely. A share issue wasn’t needed then, and if you trust management, it won’t be needed in the future either.

Growth has fallen about a year behind schedule, and costs have been front-loaded both in terms of personnel and software development. A typical SaaS situation, then.

Sales just need to get moving now that the tools are ready ![]()

New customer for CH from Sweden, though it’s a small company of about 10 people

An interesting addition to the shareholder list ![]()

Strategic investment ![]()

Leading Nordic hospital provider Aleris Invests in Physitrack’s Digital Health Technology to Enhance Home Exercise Prescription, Outcomes Analysis, and Patient Journey Personalisation

London, Oct 7, 2024 – Aleris, the largest private hospital provider in the Nordics with a proven track record of delivering positive patient outcomes, has announced a strategic investment in technology from Physitrack, a leader in digital health technology. This investment will support the integration of Physitrack’s innovative solutions for home exercise prescription, outcomes analysis, and the personalisation of the patient journey across Aleris’s extensive healthcare network.

The collaboration aims to leverage Physitrack’s advanced digital tools to enhance patient care at Aleris, particularly in the areas of rehabilitation and long-term health management. Physitrack’s technology will enable Aleris to offer personalsed exercise programs tailored to individual patient needs, analyse treatment outcomes more effectively, and optimise the overall patient experience from diagnosis to recovery.

”This partnership marks a significant step forward in our commitment to providing the highest quality care for our patients," said Thomas Kudsk Jensen, CIO at Aleris. "By investing in Physitrack’s digital health technology, we are ensuring that our patients receive personalized, data-driven care that supports their recovery and long-term health goals."\n> \n> "We are thrilled to partner with Aleris and bring the best of our technology to their patients,” said Henrik Molin, CEO & co-founder of Physitrack Plc. "Our tools are designed to empower healthcare providers with the insights and resources they need to deliver better outcomes, and we are confident that this partnership will lead to improved patient experiences and health results."

Aleris AB is part of Triton Partners, e.g. Ambea and Mehiläinen have been through those funds.

Aleris provides high quality healthcare services including emergency rooms and radiology

Aleris is one of the leading healthcare companies in the Nordic.

The company was acquired from Patricia Industries, a part of Investor AB, in October 2019.

Headquartered in Stockholm, Sweden and with more than 4,000 employees, Aleris is a provider of specialty care and healthcare with a strong footprint across Scandinavia. The company’s specialist care operations cover hospitals and outpatient clinics. Aleris performs approximately one million radiological examinations annually.

The company operates in Sweden, Norway and Denmark and its services are used by public healthcare, insurance companies and private patients.

Triton invested in Aleris on back of extensive experience in the field through portfolio companies such as Ambea and Mehiläinen.

Driven by an ageing population, new medical technologies and a mix of public and private funding the health-care sector in the Nordics is non-cyclical with a growing market for high-quality healthcare services.

Within the Aleris ambition to be a long-term partner to public healthcare, Triton supports the company´s opportunities to build on its solid foundations through selected acquisitions and digital transformation.

Well, that quarter didn’t exactly go to plan. ![]()

This quarter has seen us navigate a challenging environment with steady progress, while addressing temporary setbacks in Wellness and implementing several initiatives to position the Group for future growth.

Third quarter: 1st July – 30th September 2024

- Revenue increased by 1 per cent to generate total sales of EUR 3.9 (EUR 3.9m). This growth was achieved in the Lifecare division (7 per cent) but was offset by a contraction within the Wellness division (9 per cent).

- Subscription revenue increased 12 per cent (EUR 0.3m) to EUR 3.3m and now makes up 84 per cent of total group revenue, a significant increase from the prior year’s comparative of 75 per cent.

- Adjusted EBITDA of EUR 0.9m (EUR 1.1m) was generated resulting in an Adjusted EBITDA margin of 23 per cent (27 per cent).

- Adjusted operating loss of EUR 0.2m (profit EUR 0.1m) was generated resulting in a margin of -6 per cent (3 per cent).

- Adjusted ordinary and diluted profit per share totaled EUR (0.02) (EUR 0.00).

- Cashflow generated from operations before the payment of adjusting items equaled EUR 0.8m (EUR 0.9m).

- Free cash flow for the quarter was a net outflow of EUR 0.4m (outflow EUR 0.3m).

Key highlights during and subsequent to the third quarter

The Lifecare division has demonstrated remarkable and consistent profitability, particularly in Physitrack platform subscription sales to the MSK rehabilitation segment, expanding its influence across both public and private healthcare

sectors. The division has firmly positioned itself as a leading provider of software for injury prevention and recovery solutions, ensuring its ongoing relevance in the evolving healthcare landscape.In the Wellness division, innovation, talent acquisition, and successful integration of acquired businesses have been key drivers of its early growth, with acquired companies scaling 3-4times post-acquisition. However, challenges have arisen due to delays in the international rollout of Champion Health’s software, slowing the Wellness division’s growth. Despite this, significant progress has been made with Swedish and German market entries in October, and

long-term prospects for Champion Health remain strong.Looking ahead, the Lifecare division continues to enhance its market share by providing market-leading solutions that address emerging healthcare needs. Meanwhile, with international Champion Health versions launched at the end of October, the Wellness division is set to be well-positioned for rapid expansion with new products and markets that empower health and wellbeing, allowing the company to capitalise on the rising demand for digital health solutions.

Selected from the CEO’s comments:

The internationalisation of Champion Health, a uniquely holistic data-focused and ultra-personalised employee wellness solution, was especially key to continuing the strong Wellness growth journey that we set out on in 2021. Unfortunately, due to the Champion Health launch delays, we have been unable to put this software into the hands of the Wellness entrepreneurs that generated our amazing growth in 2021-2023 as quickly as planned, which has led to our expansion strategy slowing down. This is, of course, disappointing for all of us who were keen to bring Champion Health to a broader audience and accelerate its impact

Nevertheless, I want to assure you that this delay is only temporary, and our commitment to ensuring a successful launch is unwavering, with the Swedish and German releases having been executed at the end of October. Following this, we are taking deliberate steps to refine our approach and strengthen our position in these new markets.

In my view, the investment case remains intact despite the delay. The delay causes costs and pushes revenues into the future. However, the platform is now up and running, and the first order has already been announced.

Wellness needs to start delivering new orders and growth, however, for this to really become something sensible over time.

Lifecare continues to deliver steadily, nothing new there.

Edit, more about the balance sheet:

Redeye’s expectations were more moderate than my own. Q3 was very close to RE’s forecasts, though costs were higher, as could be seen from the figures.

Growth forecasts have been trimmed slightly downward due to Wellness’s long sales cycles with larger customers.

In my view, that first Nexa deal shows that it is possible to get upsells to existing customers more quickly through it. There are also likely new customers expected in the pipeline for Sweden and Germany following the delay. Let’s just hope they haven’t grown tired of waiting…

Physitrack CEO’s Q3 presentation:

There were quite a few questions about the financial situation, and Henrik seemed a bit annoyed by the third one ![]()

And an interview conducted by Redeye; I haven’t had time to watch it yet.

Restructuring at Champion Health.

Management is being reshuffled, and the focus is more on the Nexa AI service.

Additionally, physical clinics are being reduced.

A total of €800k in cost savings and €600k reduction in annual revenue, resulting in an additional €200k in profitability.

Redeye’s comments on this:

Henrik speaking and answering questions at Redeye’s Technology & Science Day event

Physitrack: CEO Henrik Molin presents at Redeye Technology & Life Science Day 2024 – December 3

I listened to it while driving, and it was quite familiar if you’ve been following the company. Otherwise, a good general overview, but at least these points stuck out: