I thought about opening a thread just for Philip Morris, but tobacco companies probably don’t need multiple threads, so we can centralize all discussion about the industry and its companies here.

I know that Swedish Match was to some extent popular among Finnish investors at one time. In 2022, Philip Morris made a takeover bid for it, and now the Swedish company is officially part of Big Tobacco. For Philip Morris, this acquisition seemed very “juicy.” The company integrated Zyn, the world’s most popular nicotine pouch, which complements Philip Morris’s Smoke-Free product portfolio.

Without further ado, let’s start reviewing Philip Morris as an investment.

Philip Morris International (PMI)

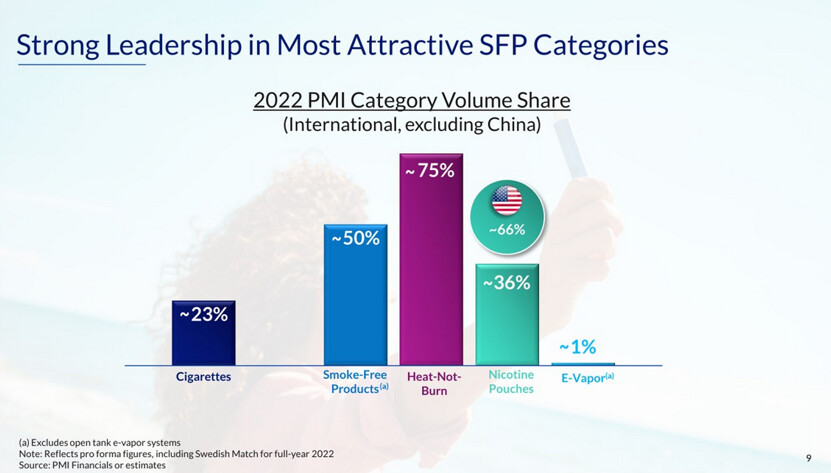

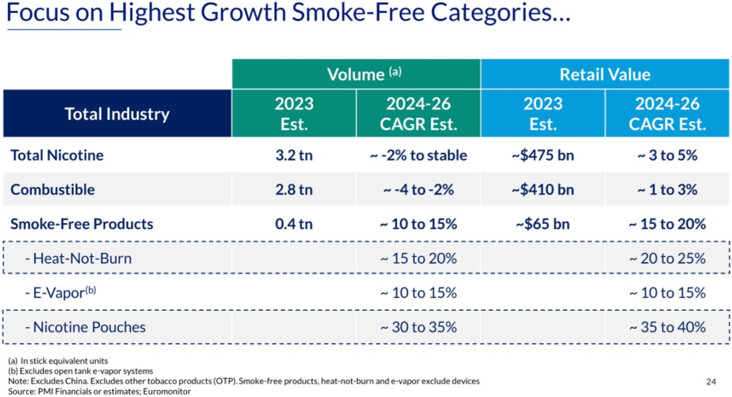

For an investor, the most important nicotine categories in PMI, in addition to traditional tobacco, are heated tobacco and nicotine pouches from the Smoke-Free products.

Let’s break down the company category by category:

1. Combustibles

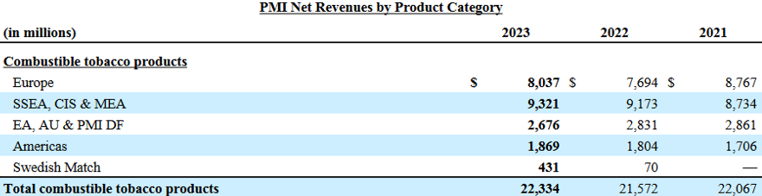

Share of revenue: 63.5% (2023)

Traditional cigarettes still account for the lion’s share of PMI’s revenue. PMI’s well-known brands include Marlboro, L&M, and Chesterfield. The company’s market is pretty much the entire world minus China and the USA. In 2008, PMI spun off from Altria, at which point the entire US business was left with the old company and the new PMI retained the international operations.

PMI has a massive moat in the tobacco business. No new competitors are entering the industry (who would start a cigarette company in 2024?) and smokers are surprisingly brand loyal. Price increases are applied to cigarette packs annually, and it hardly affects market shares. In this industry, market shares are now divided and will likely remain at the same levels indefinitely.

Tobacco is famously a dying (and death-causing) industry that investors avoid. Tobacco manufacturers’ P/E ratios usually hover around 7–9; the industry is highly disliked, and the trend of ESG investing certainly doesn’t provide any tailwinds. From a business perspective, however, the industry is perhaps not as bad as one might initially assume. Philip Morris’s Combustibles revenue was 22.3 billion in 2023, with 3.5% growth compared to the previous year. The company also guides for revenue in this category to remain stable. The decline of the tobacco market is largely offset by price increases; PMI raised the prices of its tobacco products by 8.9% in 2023, and market shares did not decline. So, there is pricing power.

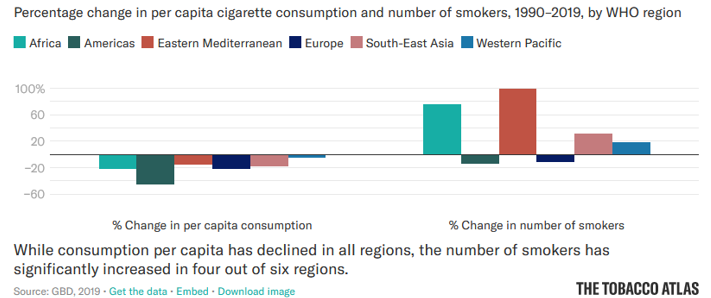

Furthermore, population growth has meant that even though smokers per capita are decreasing, the actual number of smokers in the 1990–2019 review period has actually risen. PMI also has no business in the States, which is a major market where smoking is declining sharply.

Surely other regions will eventually follow the development of Western countries, but these trends will likely turn quite slowly. Per capita figures in some developing countries are even growing due to increasing disposable income.

The industry is, of course, heavily regulated, and raising tobacco tax is politically very easy. However, smoking is so popular that it cannot be completely banned without creating a massive black market in its place.

2. Smoke-Free Products

Share of revenue: ~36.5% (2023)

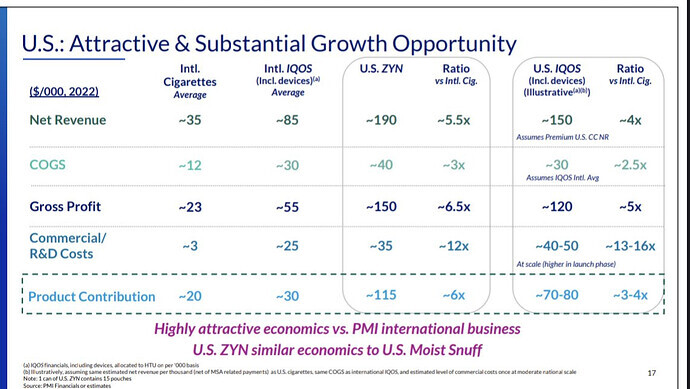

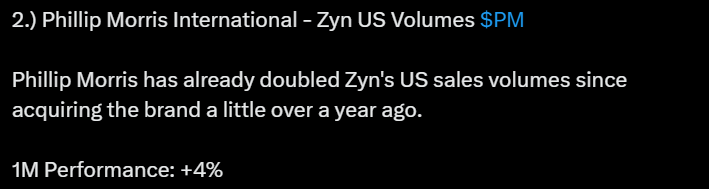

PMI’s growth engine is their Smoke-Free products. The company’s goal is to grow this segment to represent 2/3 of the company’s revenue by 2030. PMI has two extremely popular category-leading products: IQOS and Zyn. With these products, PMI aims to capture the largest Smoke-Free categories, which are heated tobacco and nicotine pouches. For now, the revenue from IQOS is about 10x compared to Zyn. However, Zyn is on a strong upward trajectory, and nicotine pouches are expected to grow by far the fastest among all nicotine products.

- Heated Tobacco Products

HTP is a category where, instead of burning tobacco, it is heated. The idea is that the harms of tobacco can be reduced when the smoke it produces is removed from the equation. PMI’s own research has convinced at least themselves of these harm reductions, but it is important to note that, to my understanding, no third-party studies providing decisive evidence on the benefits of HTP have been conducted. What is certain, however, is that HTP users also expose themselves to dangerous chemicals in tobacco. The question is whether it is still healthier than cigarettes.

Either way, this category resonates with consumers, as it was a 10-billion-dollar business for PMI last year. As a benefit of HTP, it should be mentioned that (supposedly) compared to cigarettes, it doesn’t stink as much, and the smell doesn’t cling to clothes as easily. Additionally, second-hand smoke is also milder.

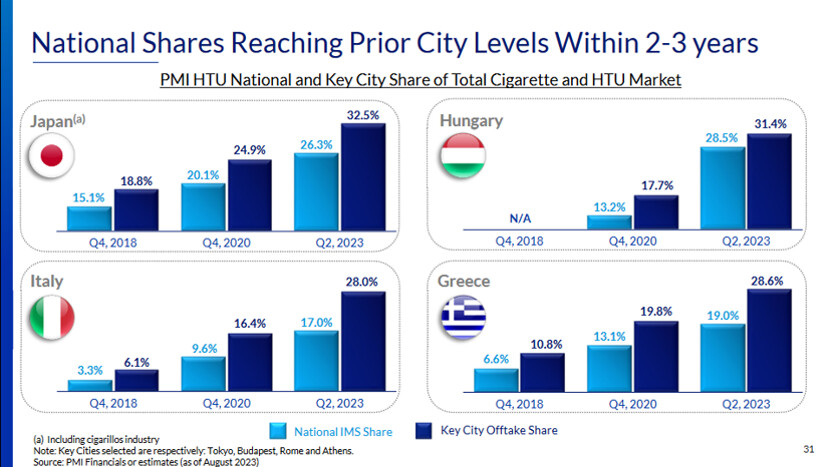

IQOS is the undisputed number one in the HTP category with 29 million users. Last year, it surpassed Marlboro in revenue and is now PMI’s highest-grossing brand. IQOS was originally launched in 2014 in the Japanese and Italian markets, from where it has now spread to 70 countries. Last year, PMI also bought the rights to the US market from Altria. The price tag for this was 2.7 billion, and on April 20th, PMI was allowed to start selling the product in the States as well. Success in the USA would be very profitable for PMI shareholders because, unlike in other markets, the success of IQOS in the USA would not cannibalize PMI’s Combustibles business at all.

The expansion strategy for IQOS is quite interesting. PMI targets its product only at certain key cities, from which it has successfully made the market shares of the rest of the country match the levels of the key cities with a 3-year lag.

In my opinion, IQOS feels like an odd “in-between” nicotine product. It still uses tobacco, whose popularity is at a breaking point in the West and whose health risks are known. For me, it’s hard to justify why someone would want to switch a cigarette addiction to an IQOS addiction when there are clearly healthier nicotine products available as alternatives. Of course, I am not a smoker myself, and the numbers here speak for themselves. IQOS has been an incredible success for PMI.

- Nicotine Pouches

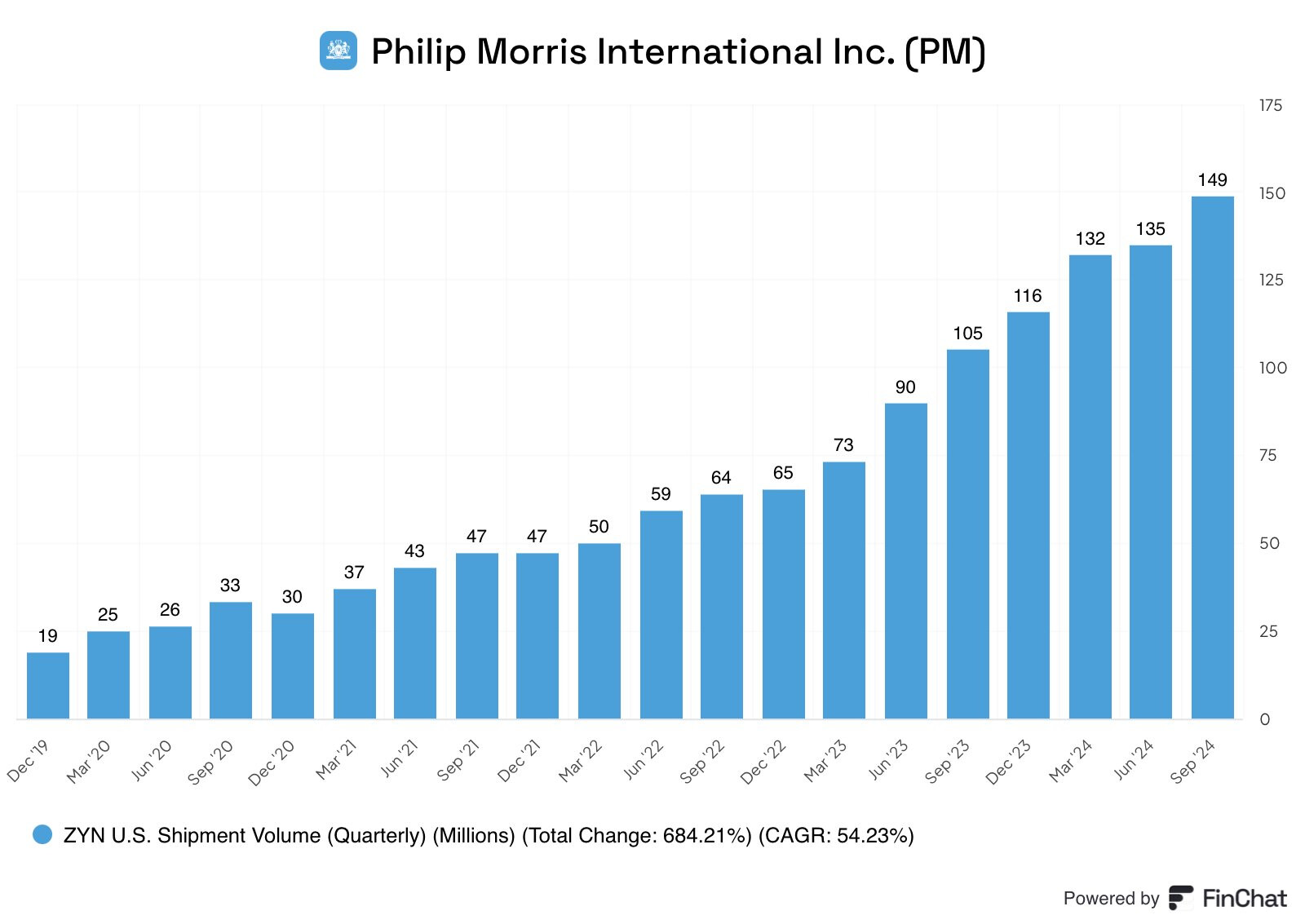

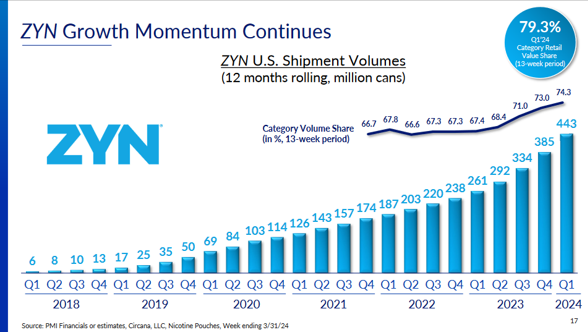

Although nicotine pouches are still relatively marginal compared to PMI’s other business, this category is the strongest grower in the coming years. The nicotine pouch category is expected to grow at an annual rate of up to ~35%, and if you have followed social media culture, this is not surprising.

Nicotine pouches are a new, cleaner, and more stylish way to get hooked on nicotine. Zyn has broken through especially in the USA, where these cans are being torn off store shelves.

Growth has been very strong and is not expected to slow down. In much the same way as key cities showed the direction for the rest of the market with IQOS, the Western US seems to be a few years ahead of the rest of America in “Zynification.” So, there are still many new growth areas even within America. If the Nordic nicotine culture were to land in the States, pouches would replace other nicotine products in massive quantities. This development would suit PMI quite well, as one must still remember that PMI does not sell cigarettes in the States. Thus, the growth of Smoke-Free products would not cannibalize PMI’s own products.

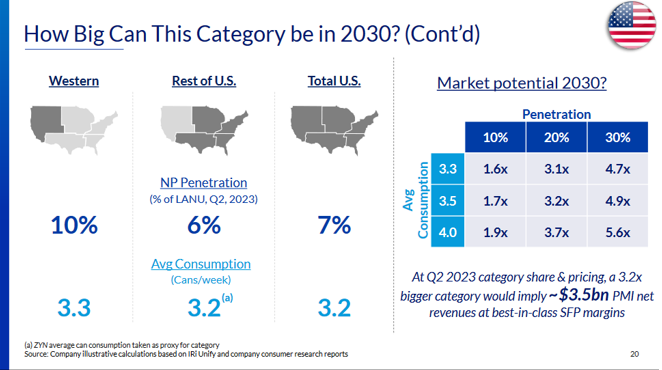

(LANU=Legal age nicotine user)

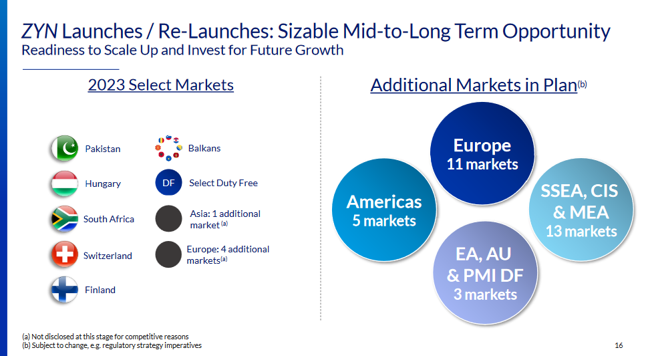

Zyn’s second growth lever is, of course, expanding into new countries. Currently, Zyn is only sold in a few countries, so there is certainly room for growth. In this expansion, PMI utilizes the infrastructure used for IQOS, meaning it aims to cross-sell Zyn cans to IQOS retailers as well.

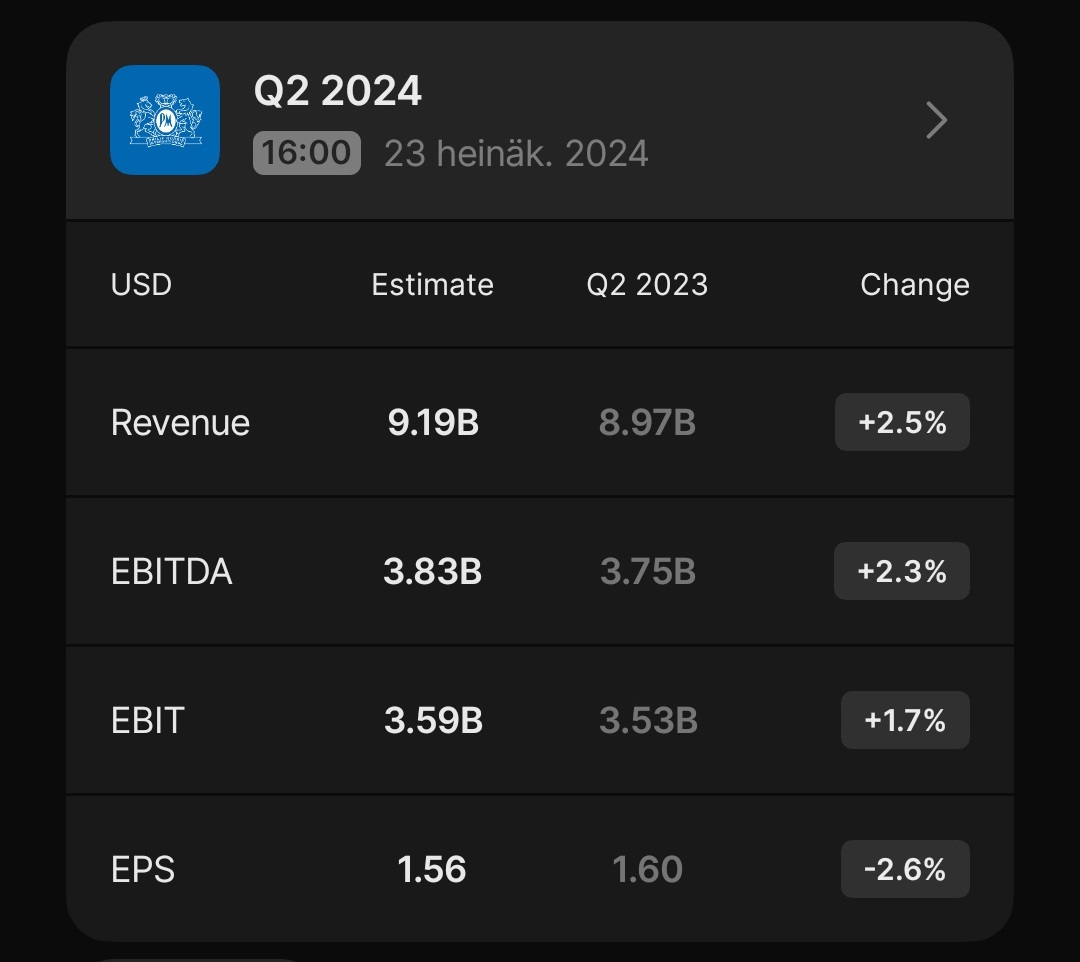

Philip Morris ValuationEV/EBITDA is ~13.5 based on this year’s forecasts. One can draw many conclusions from the valuation. If you compare it to the average S&P 500 company, it sounds cheap. On the other hand, if you compare it to the valuations of other tobacco companies, there is room for it to drop by almost half. Personally, I think that if PMI can churn out 10% earnings growth, there shouldn’t be much downside in these multiples, but you shouldn’t expect tech multiples for a tobacco company either.

My own back-of-the-envelope calculations expect the valuation to remain unchanged, with the investor’s expected return consisting of 10% earnings growth in the coming years and a >5% dividend. This probably won’t be a moonshot, but you can still achieve a good return with that.

The nicotine industry is very much dependent on trends, which can change quickly. Regulation can also come as a surprise and change the entire market overnight. A few years ago, vaping was massive, and Juul’s popularity in particular was halted by the CDC, which banned the most popular flavors entirely. So nicotine products change form, but the need is unlikely to ever disappear. Roughly one in five of us walking this earth uses nicotine, and humans seem to have some compelling need for this substance. From the perspective of the investment case, it’s critical that PMI continues to perform well in the most important nicotine categories, whatever they may be.