I didn’t see a dedicated thread for Mettler-Toledo, and since I’ve been looking into the company more closely lately, I thought it would be a good exercise to start a thread about it.

Mettler-Toledo is a leading global manufacturer of precision instruments. The company describes itself as follows (AI-translated):

“METTLER TOLEDO (NYSE) is a leading global supplier of precision instruments and services. We have strong leadership positions in all of our business units and believe we are the global market leader in most of them. We are recognized as an innovation leader, and our solutions are critical in key R&D, quality control, and manufacturing processes for our customers, who operate in a variety of industries such as life sciences, food processing, and chemicals. Our sales and service network is one of the most comprehensive in the industry. Our products are sold in more than 140 countries, and we have a direct presence in approximately 40 countries. We have achieved strong long-term financial results thanks to proven growth strategies and our execution-focused operations.”

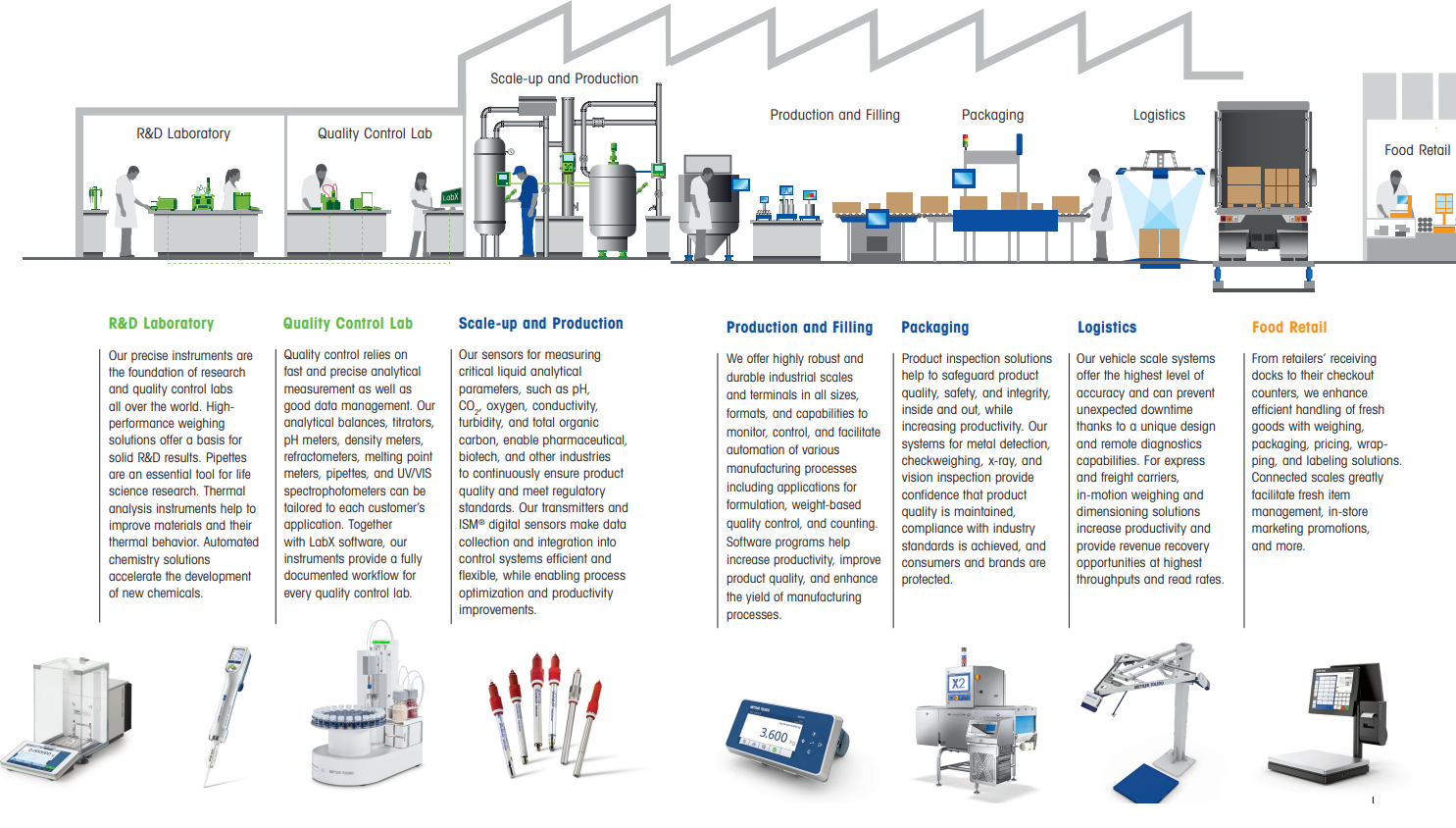

The company’s product offering is presented quite nicely in the 2023 annual report:

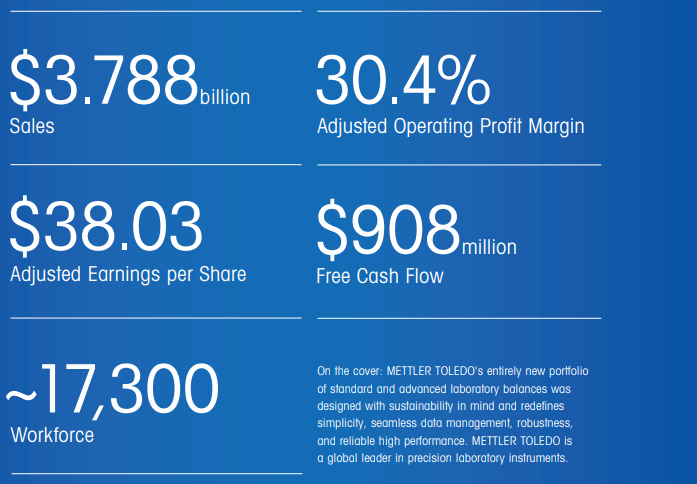

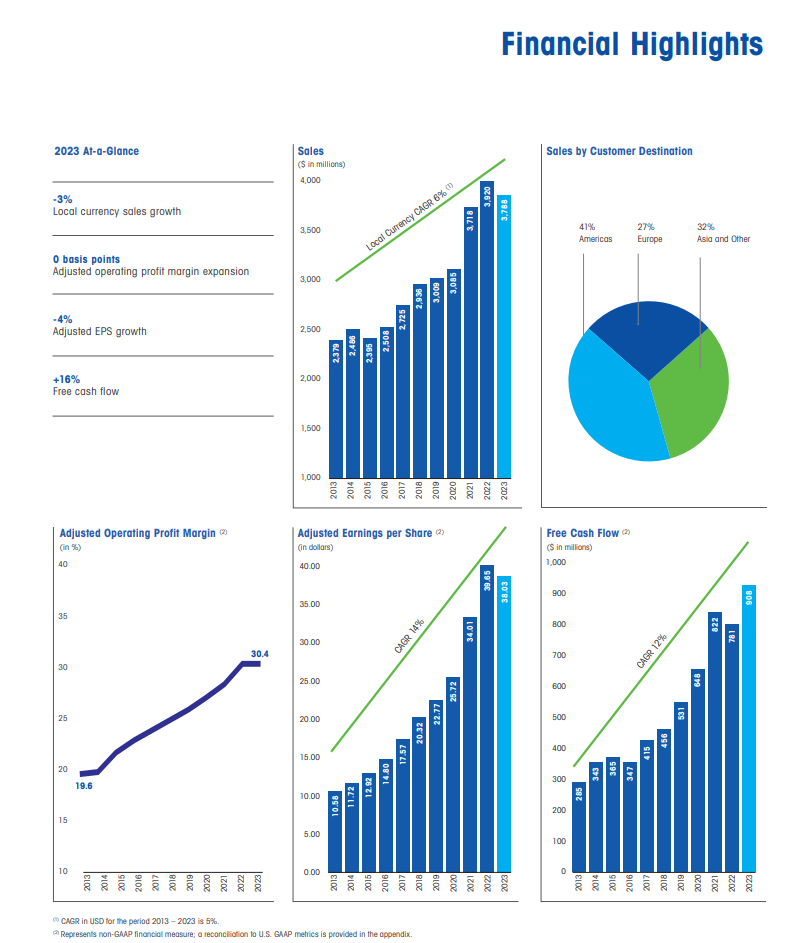

Here are some key figures for 2023:

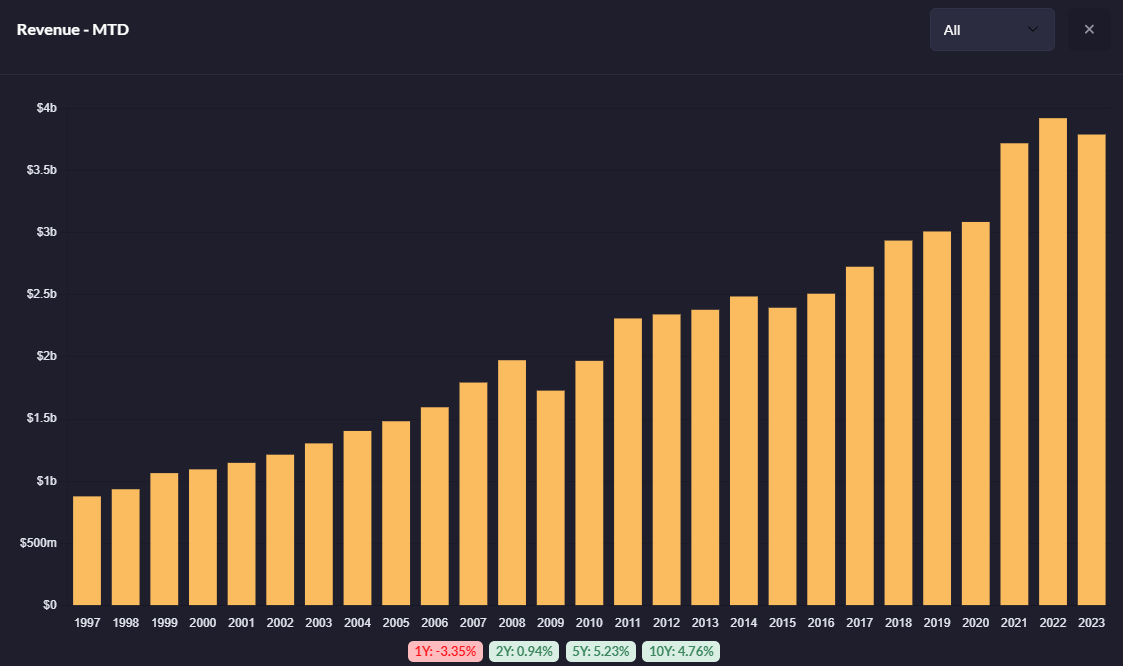

Historically, the company has been able to grow its revenue by approximately 5%.

As seen in the images above, the 2023 revenue decreased compared to the previous year. According to the company, this was due to weaker demand from life sciences customers and a significant decline in China during the second half of the year. Customers apparently reduced their investments as the year progressed due to global economic growth concerns, higher interest rates, and increased geopolitical tensions. For next year, the company guides for approximately 2% revenue growth. In my view, it looks like there was an exceptional step-up in revenue in 2021, and now things are starting to return to historical trend growth.

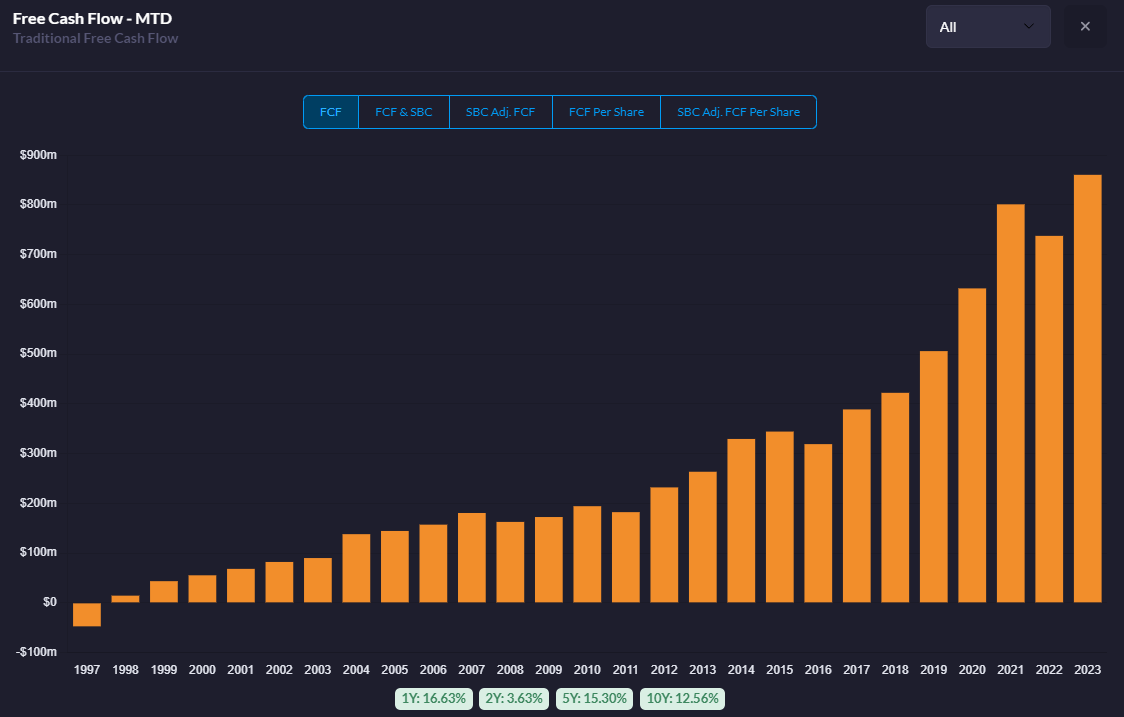

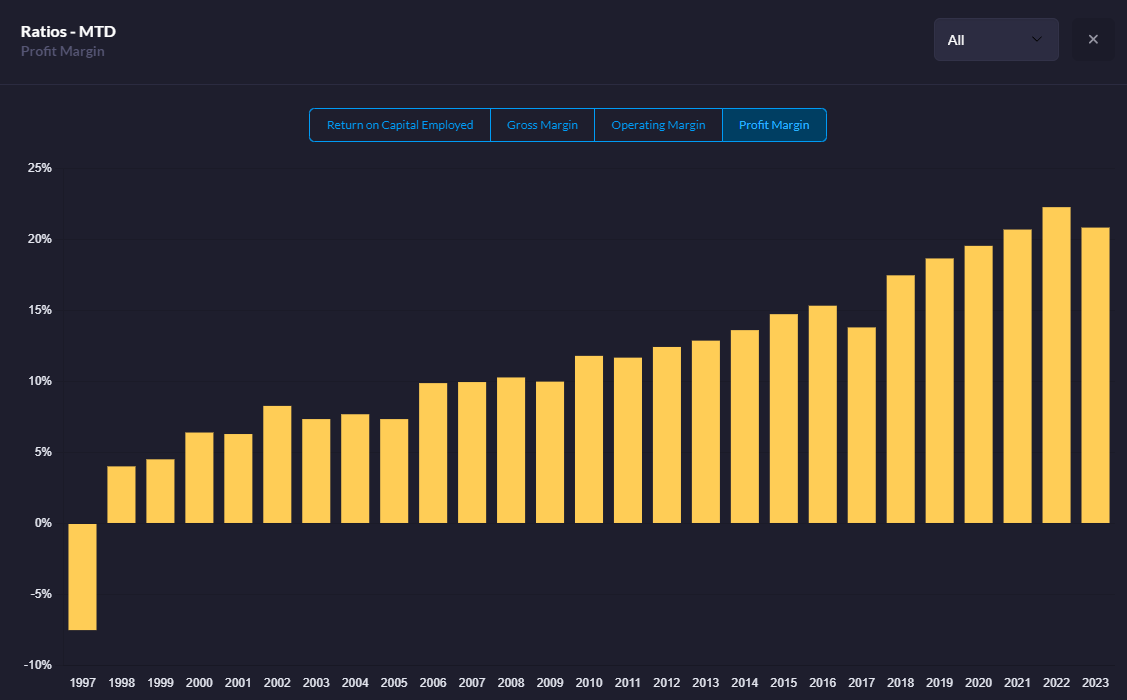

Historically, the company has been able to grow free cash flow and EPS faster than revenue due to improved margins:

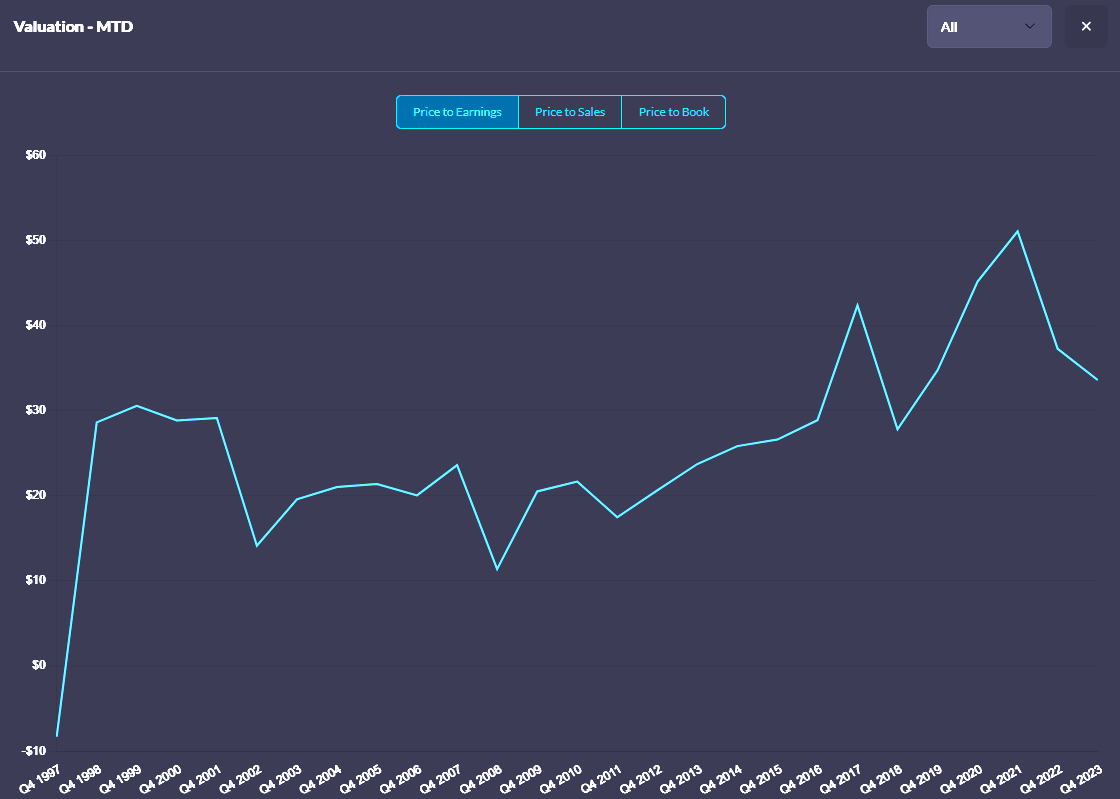

The current valuation is pretty much what you would expect from a high-quality US company:

The company is interesting to me in the sense that I am familiar with its products (e.g., scales) through my work history.