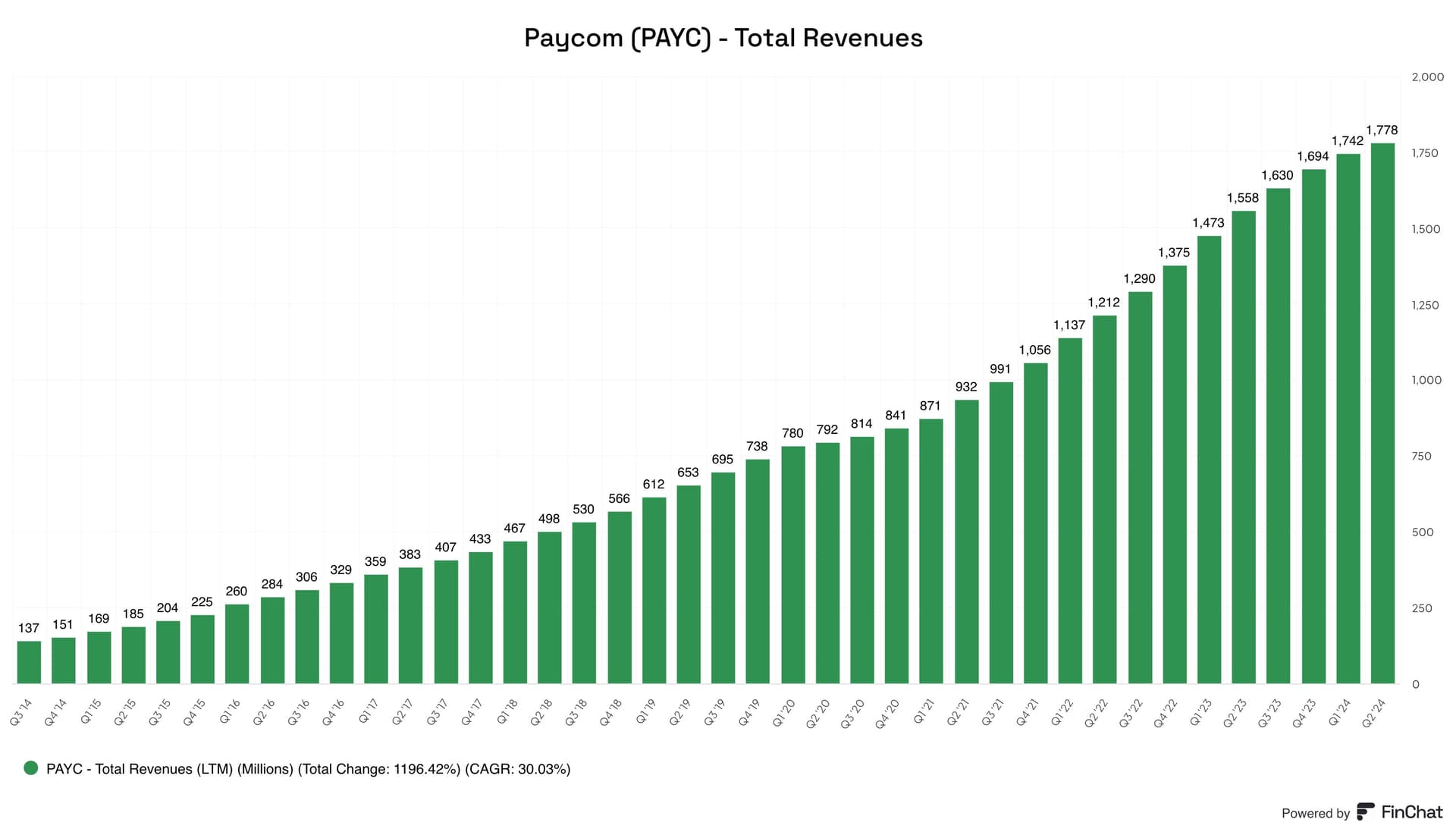

Paycom Software, Inc. is an American provider of web-based payroll and human resource management services. Founded in 1998, the company was one of the first fully online payroll service providers and has gained a reputation as one of the world’s fastest-growing publicly traded companies, in addition to receiving recognition for its innovation.

Paycom expanded its services in 2001 to include human resources. In 2014, the company went public on the New York Stock Exchange.

The company’s CEO, Chad Richison, was the highest-paid executive in the U.S. in 2020, but his compensation was largely based on company stock that only vests if the company hits certain share price targets. In 2021, Paycom released Beti, a new payroll system that allows employees to manage their own payroll. ![]()

![]()

Investor reflections

In the first paragraph, I raved about the company’s innovation and how it has grown, but:

The BETI system launched by Paycom in 2021 is cannibalizing the company’s existing business. BETI reduces payroll errors by up to 80%, which is naturally good for customers, but it means less revenue for Paycom from fixing errors and smaller customer service teams, which weakens the company’s revenue.

It also doesn’t help the company’s situation that the U.S. unemployment rate has risen for five consecutive months, slowing down recruitment. Since Paycom prices its services per paycheck, this has directly affected the company’s bottom line. Consequently, analysts have revised their forecasts downward.

Thirdly, the human resources software market is highly competitive. In a leaked staff meeting in January 2024, Richison admitted that competitors have been catching up to Paycom, even though the company has an edge with products like BETI.

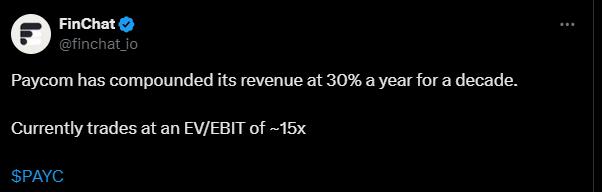

These three factors, among others, have slowed Paycom’s revenue growth, which has significantly dragged down the company’s valuation in recent years.

The company is seen as a good investment because free cash flow is in good shape, but it needs to stay competitive and succeed in managing its market share.

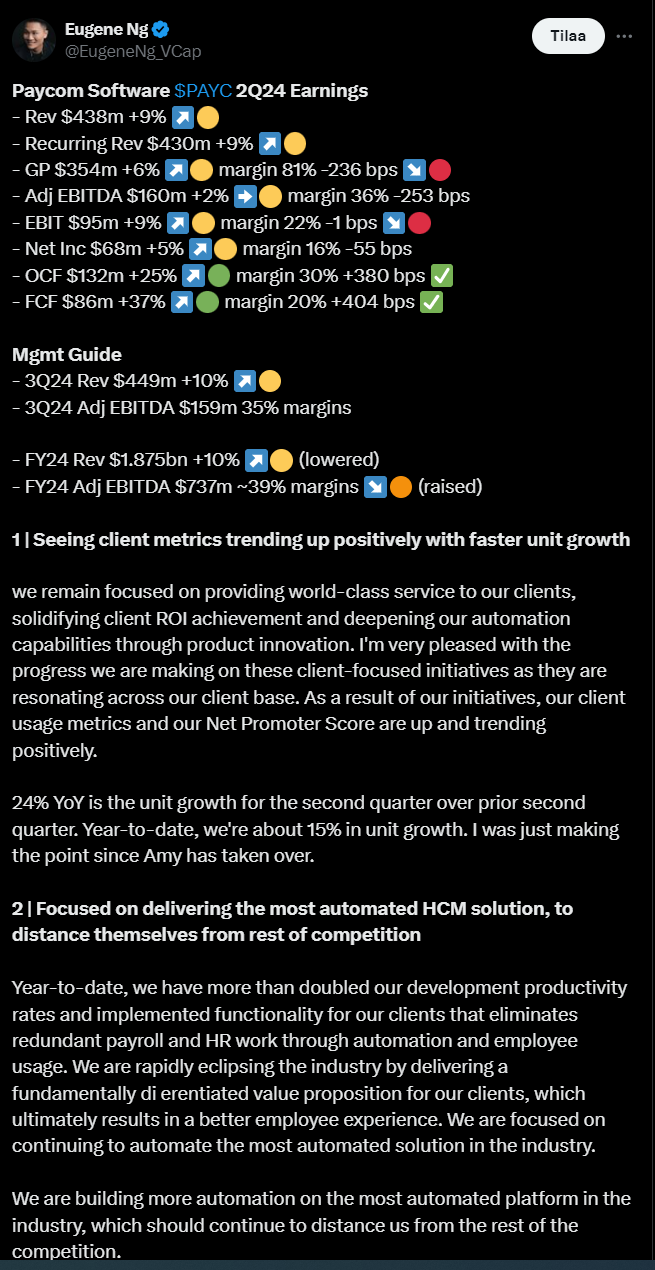

I see this tweet as sarcastic:

https://x.com/ypppy/status/1826296918307197242

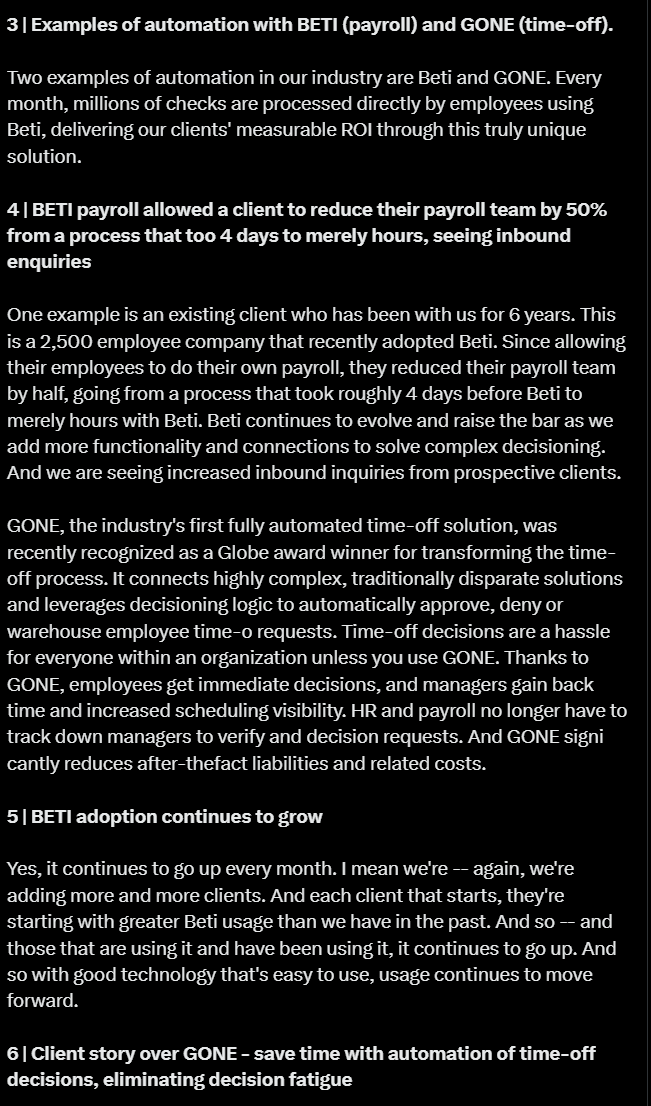

Regarding the last quarter:

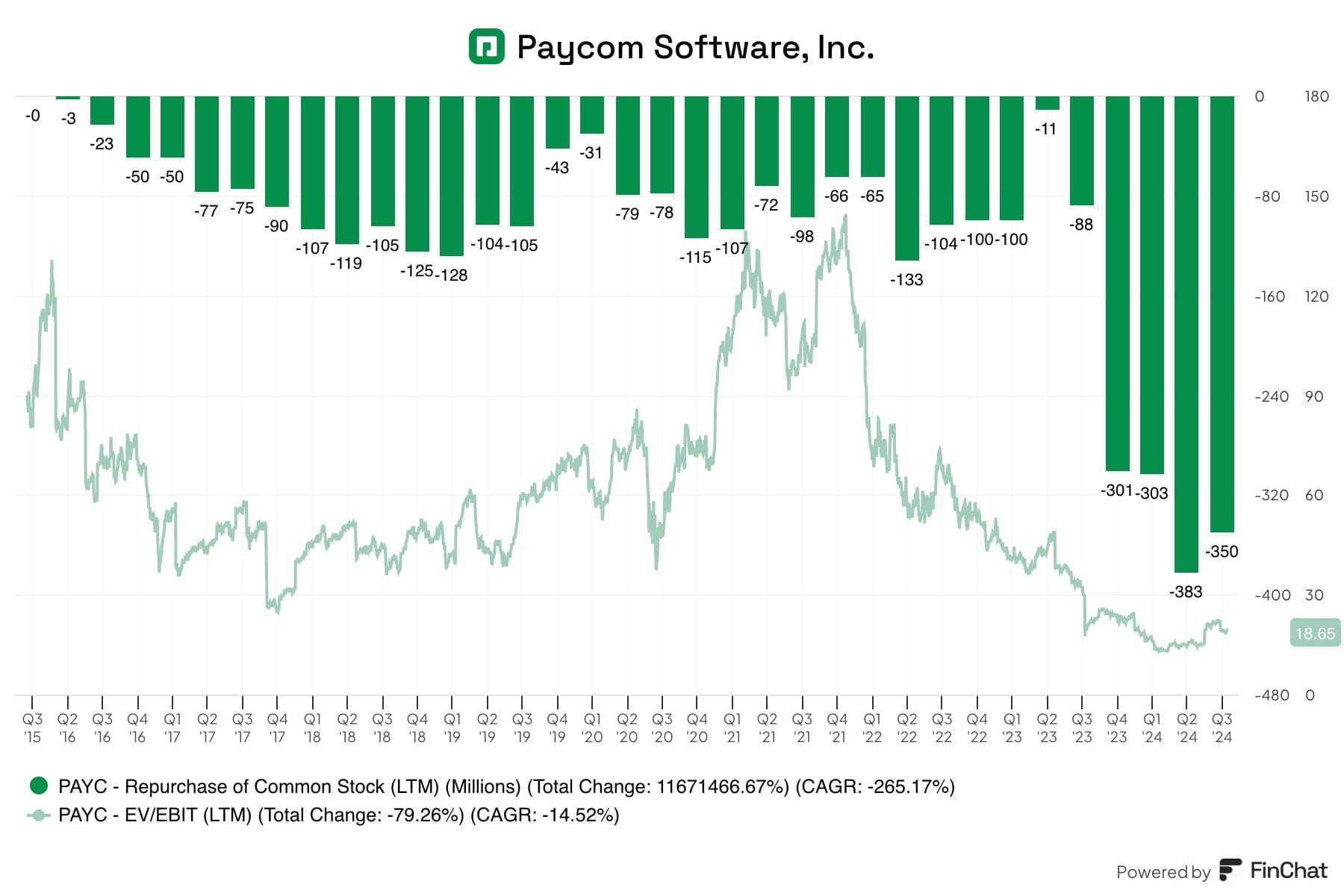

Paycom’s second-quarter results did show slowed growth, but the company says it is focusing on producing long-term value for its customers. New products, such as BETI and GONE, automate HR processes, improving the customer experience and reducing workload. However, BETI has reduced the company’s revenue, as I mentioned above. While short-term growth has slowed, Paycom believes that a long-term commitment to delivering customer value will pay off in the future. The company has also taken advantage of its low share price and bought back shares. ![]()

https://x.com/EugeneNg_VCap/status/1819264166018052148

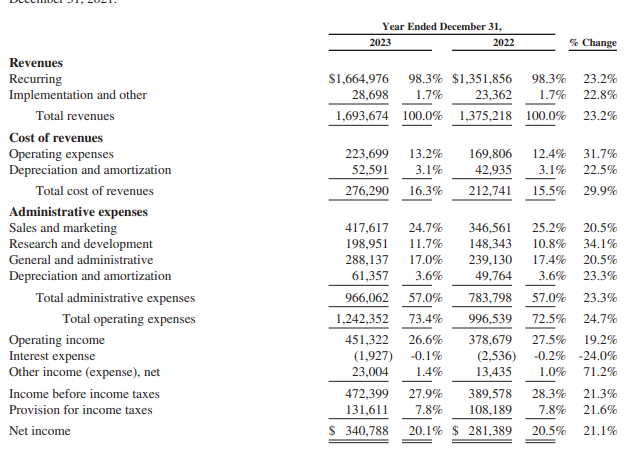

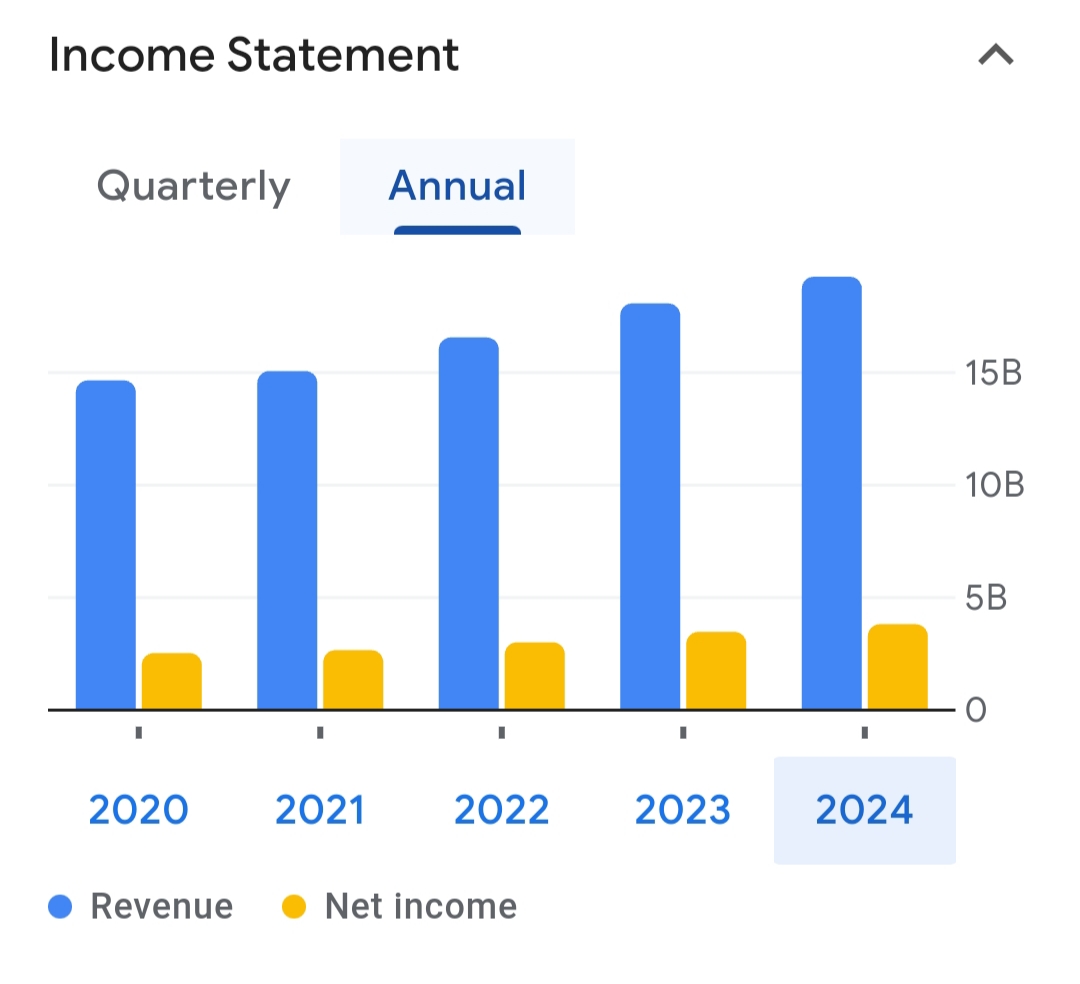

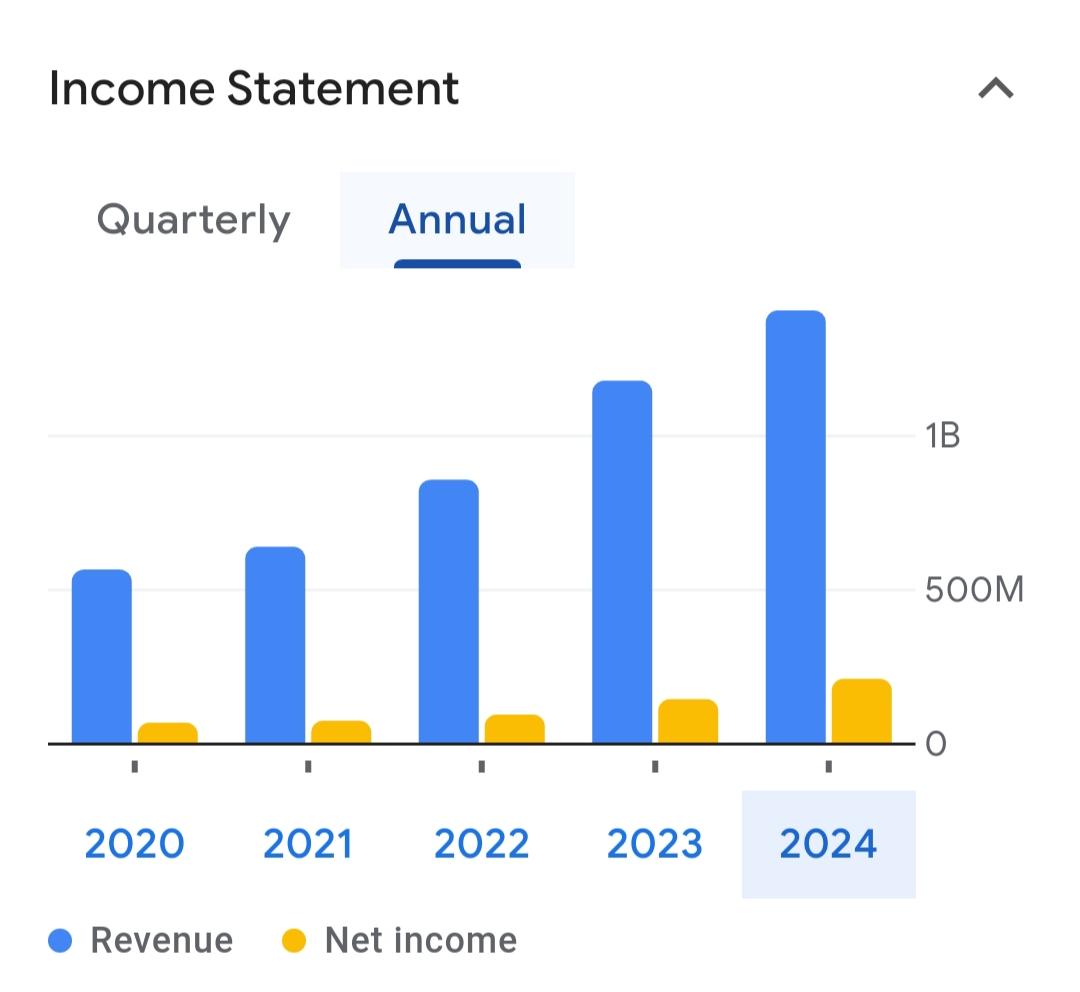

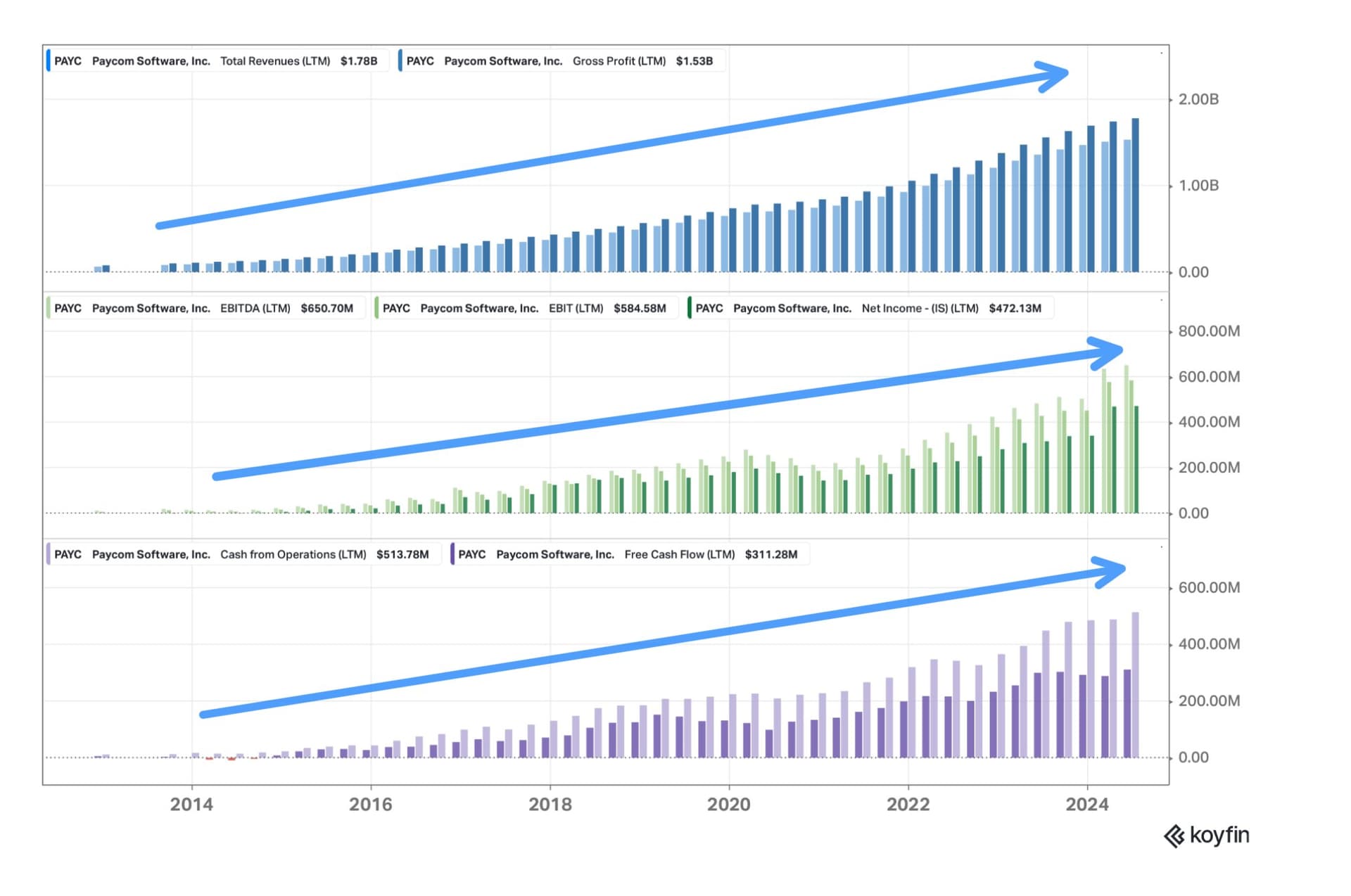

Last year’s figures from the company’s own site (https://investors.paycom.com/overview/)